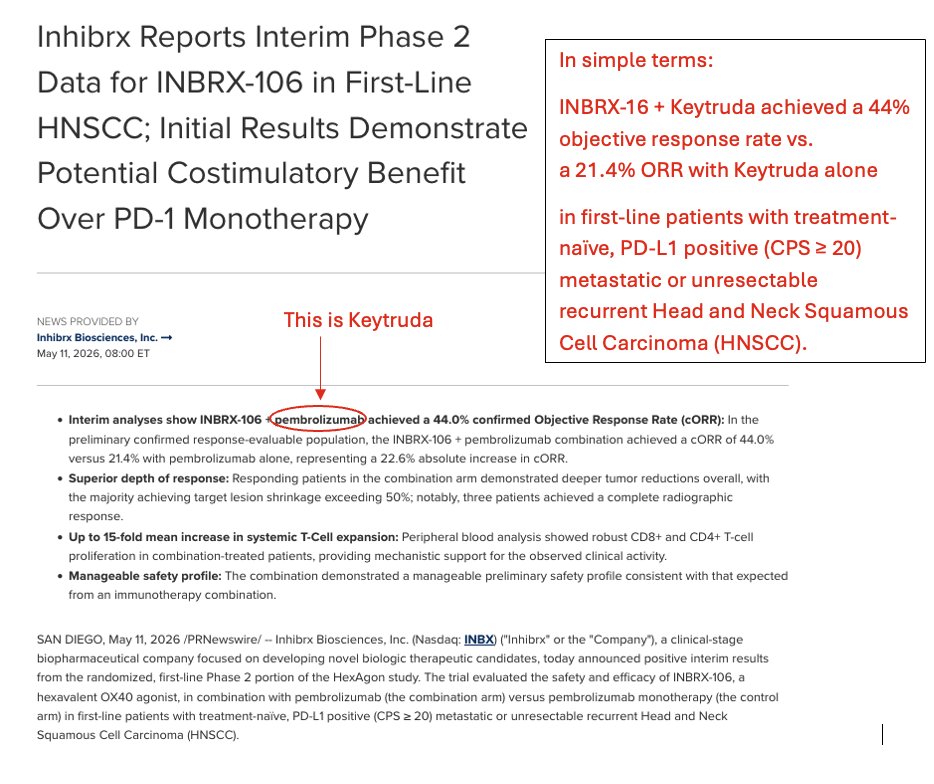

Stifel Raises $INBX target from $300 to $325 on recent positive trial data.

English

Single Best Ideas

816 posts

@SingleBestIdeas

Sharing the latest investment ideas sourced from the smartest analysts/investors (not traders) we know. Of course we are invested in most names covered here!

$SPCB 2-year chart suggests there's more to go on the upside as we await year-end results due April 30th. A quick look at the 5-year chart helps explain why impressive electronic monitoring contract wins and rev ramp have been largely ignored ... so far.