SnagsLewis

2.7K posts

$fnma this is such bull shit ... they can provide 200b to lower interest rates, they can now accept crypto which is crazy ... but they can't trade on NYSE? Has this administration done anything or took any actual step that helps shareholders besides trumps 2 tweets months ago?

English

@McNamara_Brief my God, how much longer are they going to make us wait after all of these truth social posts , news interviews, now silence for months ? Very frustrating indeed

English

SnagsLewis retweetledi

“When you arise in the morning think of what a privilege it is to be alive, to think, to enjoy, to love.”

— Marcus Aurelius

English

@Alec_Mazo With the Ackman scenario, what might the dividends?

English

@SnagsLewis1978 That will depend on the share count, whether the Gov't converts the warrants to own 80% of the companies or will push for an SPS cram down as well. I agree with Ackman that getting to a $500bn+ market cap is more likely with a 80% warrant conversion & SPS writedown.

English

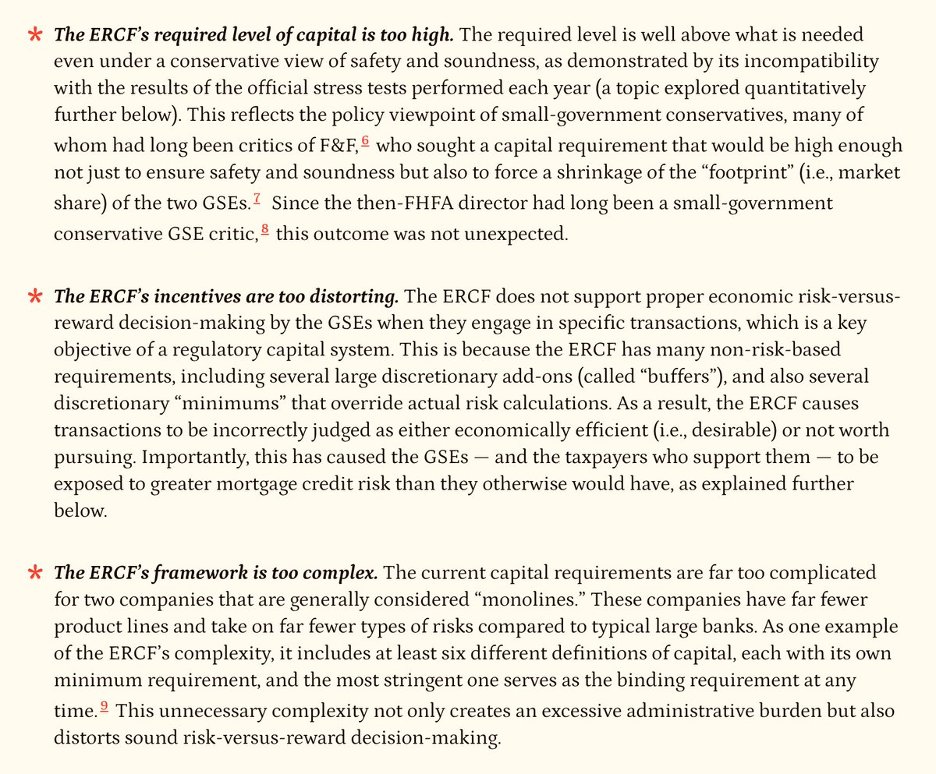

Layton hits the nail on the head - the GSEs' capital framework should be reduced to the 2018 framework suggested by Calabria's predecessor Mel Watt.

While the financial establishment lobby groups will insist it's a heavy lift, it's not. Remove the buffers and simplify the way capital is counted without a long comment period.

Then list Fannie and Freddie on the NYSE after converting the warrants and writing off the senior preferred stock (SPS). The commons will rerate significantly higher. The junior preferred could be converted into commons or left alone paying the coupon.

Further, initiate a small dividend policy in line with stable utility businesses. At 2.5% capital the GSEs would be allowed to distribute some of their earnings, a 2% dividend at a $500bn valuation will take about $10bn a year on $30bn of profits.

The Administration could partially monetize their 80% warrants stake at $500bn+ and let it grow over time to a higher valuation as the dividends are increased to 4%+ ($20bn of 30bn profits). Let's not forget that 80% of the dividends will go back to the Government!

The President is a master negotiator. There is no reason for Fannie and Freddie to be stuck in conservatorship with so much capital built up already and with the Government generating a huge book asset valuation on top of collecting dividends again that could be used for housing incentives! HUGE!!!

@pulte

@SecScottBessent

@realDonaldTrump

Tim Pagliara@timpagliara

You don’t need to do this unless you are engaged in a deliberate process to end the C-Ship. furmancenter.org/publication/pr…

English

@mey9585 @Alec_Mazo What is your estimate on annual dividends when turned on? $FNMA

English

@DoNotLose Commons about to fly. I’m hearing things again. Countdown post soon. Buckle up

English

QME

$FNMA $FMCC

It sure does seem like big, unstoppable wheels keep on turnin' to wind down the Fannie Mae and Freddie Mac conservatorship.

Will reductions in capital requirements represent a light at the end of the shareholder tunnel to our EXIT?

furmancenter.org/publication/pr…

English

SnagsLewis retweetledi

Dear President @realDonaldTrump, back in August 2025 you pushed a November 2025 #NYSE uplist narrative for $FNMA and $FMCC. We believed in you and have waited patiently long enough.

It really only takes one call to do right by the people, what exactly is the hold-up? Why push that narrative and still not act? What is the justifiable reason for this delay? Who can explain it?

Mr. President?

Secretary @SecScottBessent?

Director @pulte?

Secretary @SecretaryTurner?

Secretary @howardlutnick?

Mr. @BillAckman?

Mr. @michaeljburry?

Anyone?

As promised, please:

🇺🇸⚠️ End the Obama/Biden scam. Enough crushing hardworking Americans.

🔓 End #Fanniegate

🏦 Privatize #FannieMae and #FreddieMac - do right by shareholders.

⚖️ Justice delayed for 18 years is not justice.

#UplistNow #EndTheConservatorship

English

English

$FNMA $FMCC

Guess what's even easier!

Uplisting Fannie Mae & Freddie Mac to a legitimate exchange. And it won't take an act of congress.

@BillAckman has already preheated the oven with the NYSE.

Come on, @realDonaldTrump! It's a tap in. Let's get this party started!

The White House@WhiteHouse

It's not that hard. JUST DO IT. Save America's elections—pass the Save America Act.

English

SnagsLewis retweetledi

Death will come for you on an ordinary day, in the middle of your unfinished plans, and the world will continue on without you.

So live a little.

English

SnagsLewis retweetledi

SnagsLewis retweetledi

@BillAckman I had a dream last night that I was walking with Donald Trump and when I asked him about Fannie Mae and Freddie Mac , he told me it was happening soon $FNMA 🇺🇸🤞

English

A number of press reports have characterized our and other shareholders’ efforts on behalf of Fannie and Freddie (F2) as seeking a ‘gift’ or ‘handout’ from the government. We, the shareholders of F2, seek no such thing.

Hundreds of financial institutions were bailed out during the GFC by the U.S. Treasury. Nearly all of the financial institution bailouts during the GFC involved an injection of capital in the form of senior preferred stock by Treasury at an interest rate of 5%, plus warrants to acquire common stock in an amount equal to 15% of the face amount of the preferred with an exercise price at the then-current stock price of the rescued institution.

For example, Treasury’s preferred stock investment in Goldman Sachs was in an amount of $10 billion and, in addition, Treasury received warrants on $1.5 billion of GS' common stock at its then market price.

The bailout terms for F2 were materially more burdensome and expensive, with a higher interest rate and substantially more warrant coverage, than that of every other financial institution (other than those of AIG whose terms were similar). Despite the F2 bailouts’ massively more burdensome terms, shareholders are not complaining about the original terms.

Treasury invested $193 billion in F2 in the form of senior preferred stock (SPS), including funding for $2 billion of commitment fees, with a 10% coupon (twice that of the banks). Treasury also received warrants on 79.9% of both companies’ outstanding shares.

Fannie and Freddie have since repaid Treasury $301 billion, which includes interest on the SPS at a blended rate of 11.6%, an interest rate which is 160 basis points more per annum, and have returned the entire $193 billion of outstanding principal, $25 billion in excess of what was contractually owed. In summary, the F2 SPS has been fully repaid according to its original contractual terms plus an extra $25 billion.

Despite the fact that the SPS has been more than repaid in full, Fannie and Freddie have not accounted for these payments on their respective balance sheets, and the $193 billion of SPS remains an outstanding liability as if no principal payments had ever been made.

How can it be, you might ask, if indeed F2 have repaid $301 billion to Treasury when only $276 billion was due could there be any remaining balance of the SPS on the F2 balance sheets?

The answer relates to something called the ‘Net Worth Sweep (NWS).’

During the second term of the Obama administration, on August 12, 2012, two quarters after F2 returned to profitability, Treasury announced that it was unilaterally amending the terms of the SPS stock to provide that Treasury would take 100% of the profits of F2 each quarter in lieu of the 10% annual dividend rate. This was not a negotiated resolution with F2. It was a unilateral amendment of the original terms of the SPS that was done in bad faith.

The supposed rationale for the amended terms of the SPS was akin to the IRS garnishing the wages of someone who will never be able to pay the taxes that they owe. That is, the Treasury said F2 will never be able to pay the 10% coupon, let alone the SPS’ $193 billion principal balance, so it decided instead to ‘settle’ for 100% of F2’s profits forever.

In discovery, shareholders learned that the stated justification for the amendment was false. In mid 2012, the Obama administration had come to learn that both companies would soon be reversing tens of billions of reserves on their balance sheets as housing values had increased and the reserves taken during the GFC had been excessive. The NWS was instituted by Obama to forestall F2 from forever being able to recapitalize and be released from conservatorship. The NWS was not a ‘settlement’ for a lesser amount of future payments. It was the outright theft of the forever profits of both companies.

Never before or since has the government ‘swept’ 100% of the profits of any company, let alone a financial institution in conservatorship, a form of government intervention where the goal is rehabilitation of the institution, and where the hierarchy of corporate claims has always been respected.

The accounting for the NWS payments while it was in effect (until Secretary Mnuchin terminated the NWS in Trump’s first term) was also unusual. The NWS was treated by F2 as a quarterly adjustment to the dividend rate on the SPS such that the dividend amount owed was made equal to the after-tax profits of F2 for that quarter with no limitation.

In other words, regardless of the amount of profit F2 generated for the quarter – whether or not it was in excess of the original 10% annual dividend – the dividend payable under the NWS was made equal to the quarterly profit. The absurd terms of the NWS sweep therefore made it impossible for any partial or full repayment of the SPS to take place as every dollar paid to the Treasury on the amended terms of the SPS was considered a dividend payment, even if the amount was massively in excess of the original contractual SPS terms.

The absurdity of the NWS was made clear just two quarters after the NWS went into effect. Fannie Mae generated a profit of $59 billion in the first quarter of 2013, and the SPS dividend rate for that quarter was set at $59 billion so the entire amount was swept to the government, more than 10 times the contractual dividend rate.

I had the opportunity to discuss F2 and the NWS with Warren Buffett about a decade ago and he said that he “couldn’t believe what the government had done.”

In short, the shareholders of F2 are simply asking the government to respect the original and highly burdensome terms of the SPS. There is no dispute that Treasury has received more than the original 10% coupon and full repayment of principal of the SPS, that is, an extra $25 billion.

We and the millions of other shareholders of F2 are simply asking the administration to honor the original SPS terms and properly account for the $301 billion of payments, thereby eliminating the SPS liability from both companies’ balance sheets.

Shareholders have not asked for the extra $25 billion to be returned to the two companies. Treasury can decide whether to keep those funds or return them to the companies.

Accounting for the repayment of the SPS has other important implications. Namely, it is critically important that conservatorships respect the rule of law, in particular, the contractual terms of corporate instruments and the hierarchy of claims. Otherwise, no financial institution that gets into trouble will be able to raise rescue capital in the private markets.

Notably, the treatment of F2 in conservatorship explains why Silicon Valley Bank and other recent large bank failures since the GFC were unable to raise private capital and avoid government intervention or a forced sale to J.P. Morgan. If the government with the stroke of a pen during conservatorship can at a whim wipe out common and preferred shareholders, no one is going to step in to try to save a financial institution that gets into trouble, and only the top few banks will be possible rescuers of big banks that fail.

Furthermore, because of F2’s history, their reputation in the capital markets has been greatly damaged. F2 raised $22 billion of preferred stock in the year or so prior to conservatorship as the government pressed both companies to raise capital. Institutions were willing to invest billions of dollars of capital into both institutions before they failed because, based on all precedent conservatorships, the contractual terms of all financial instruments and the hierarchy of claims had been preserved. Unfortunately, in light of the precedent of the net worth sweep, no investor can be confident that they won’t be wiped out in a future conservatorship so none has been willing to take the risk.

Some have proposed that Treasury simply convert the SPS into junior preferred and common stock and massively dilute shareholders. Putting aside the potential legal challenges to this approach, the result will be that Treasury will at best own something approaching 95% of both companies rather than 79.9%.

While the government’s percentage ownership stake would be larger in the SPS conversion approach, the value of the government’s larger stake would be considerably lower as the companies would become un-investable. Who would invest in F2 alongside the government when they just wiped out the previous owners?

In the SPS conversion scenario, the government’s stake, at best, if it could be sold, would trade at a massively discounted valuation, well below the value of the government's stake if Treasury retained only its contracted for 79.9% stake and respected the original terms of the SPS. In other words, a slightly smaller ownership stake of much more highly valued companies would equate to considerably more value for Treasury and taxpayers.

In a public letter to Rand Paul after his first term in November of 2021, President Trump recognized that the net worth sweep was theft from the shareholders of Fannie and Freddie. He wrote:

“Another Obama/Biden scam in legal trouble was when they allowed the Federal Housing Finance Agency (FHFA) to steal the retirement savings of hardworking Americans who had invested in Fannie Mae and Freddie Mac…The idea that the government can steal money from its citizens is socialism and is a travesty brought to you by the Obama/Biden administration. My Administration was denied the time it needed to fix this problem because of the unconstitutional restriction on firing Mel Watt. It has to come to an end and courts must protect our citizens.”

I couldn’t have said it better than President Trump.

Now that you have the time, Mr. President, let’s Stop the Steal!

English

SnagsLewis retweetledi

Concentration builds wealth. Overdiversification kills returns.

Stanley Druckenmiller:

“You make 70–80% of your returns on two or three ideas, even if you have 30 or 40 stocks.”

The best investors focus on their highest conviction bets.

Conviction > diversification.

English

Let’s hope shareholder justice is coming.

$FNMA $FMCC

Horseman Country@HorsemanCountry

$FNMA $FMCC @BillAckman sets the record straight on the Fannie Mae & Freddie Mac conservatorship that's outlived its purpose but still torments shareholders despite F2 paying back more than they owed. Well worth the informative & factual read. Shareholder justice is coming.

English

@TomBrevL lol just kidding copied that of someone else’s post on here I’m not that brave 😂

English