long

350 posts

$EOS.AX is the most promising counter-drone company on the market.

I believe this has even more upside potential than $ONDS right here.

And the best part:

It's basically undiscovered by retail and institutions.

The rerating will be massive, once the market catches up with reality.

The Analyst@MMatters22596

English

Why do I keep seeing the lazy excuse that “competition will be tough” from people who do not believe in $ONDS? You realize the people investing in Ondas believe their technology is among the best in the field, right? It is such a weak argument. It often comes from people who still think this is just a drone company. Can you not read or are you simply too lazy to actually research the company?

English

@fundmyfund Nah mate, that analogy doesn’t work. At this point you just sound bitter. By that logic, anything on the internet would be a partner of Microsoft or Google. I thought you were funny, turns out you’re just bitter. $ONDS

English

@StocksSucks We are all $NVDA partners, Anduril suppliers, $PLTR partners and I already forgot the other one that every company on earth trots out as a reason to BUY THAT STONK

English

Is this the PR that finally breaks the shorts? $ONDS

Sleuth 🔎@YoYInvestor

$ONDS x $PLTR 🔥🔥🔥 Palantir just partnered with Ondas and World View to build a next-generation AI multi-domain intelligence platform. This is the stack: 🌎 Stratospheric surveillance balloons (World View) 🚁 Autonomous drones & robotics (Ondas) 🧠 Palantir AI turning sensor data into real-time decisions But the real story is the 3 programs launching: 1️⃣ Warp Speed – scales production & operations of balloon fleets for persistent surveillance. 2️⃣ AI Flight Director – AI mission control that plans routes, coordinates assets, and optimizes coverage in real time. 3️⃣ SkyWeaver – edge AI running on the balloons, analyzing sensor data before it even reaches the ground. Translation: A persistent AI ISR network spanning stratosphere → air → ground. This is what the future of defense infrastructure looks like. Accelerate. businesswire.com/news/home/2026…

English

Valverde must be Simeone’s dream player. Works like an animal, always lets his game do the talking instead of his mouth, a true captain, and on top of that incredibly gifted with the ball. I honestly think Simeone would pick Valverde over any footballer in the world if he had a free choice #UCL

English

@retail_mourinho Been long since november 24’. Eric is starting to really piss me off right now

English

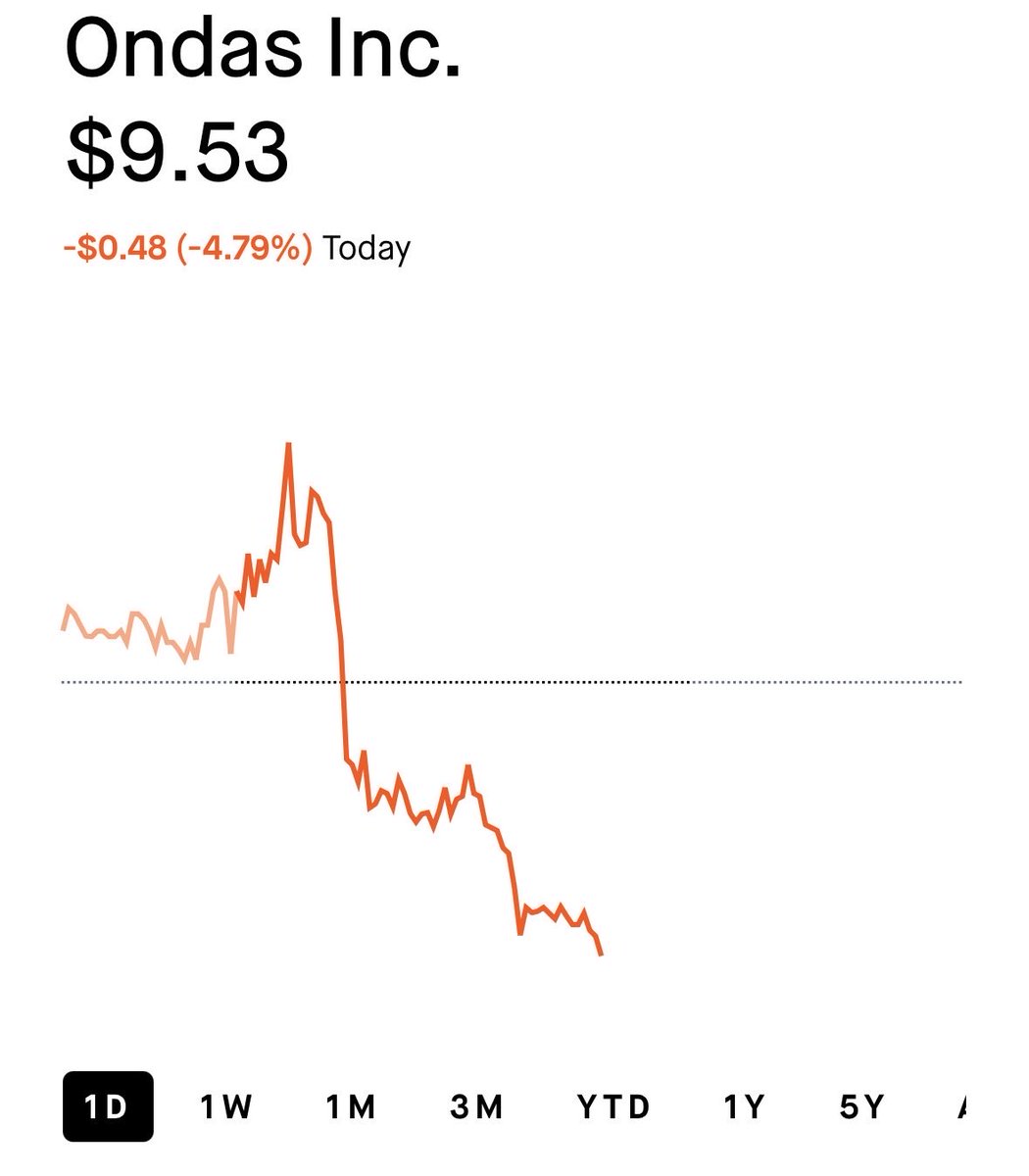

$ONDS down on the 2nd dilution this week. Just short term noise. Dips are buying opportunities 🤝🏻

-RM

English

Integration risk is a real concern for $ONDS so I wanted to take some time to address it

First, let’s understand what integration risk means for $ONDS specifically

Ondas isn’t doing traditional M&As, where you merge teams, consolidate ERPs, and cut redundant headcount

Their model is closer to a holding company or a private equity roll-up; subsidiaries keep their own management, their own brand, and their own customer relations

So the risk isn’t about culture clash, it’s more specific than that:

1. Can Ondas allocate capital intelligently across all subsidiaries

2. Are the subsidiaries getting starved of resources

3. Is there meaningful cross-selling and sharing of tech, or do they operate independently?

4. Are subsidiaries key people staying?

————————————

What we’ll need to assess over the next year is:

1. Are the founders and key operators of each company still in their roles 6-12 months from now

- if anyone quietly disappears within the first year = red flag

2. Is Ondas creating equity structure that keeps leadership motivated?

- important when you consider that most of Ondas M&As have been structured with equity

3. Is each subsidiary continuing to win on its own?

- sentrycs $6m Middle East orders, 4m defense tender win, etc… these are positive signals

- if contracts start drying up, ask why

4. Are deliveries happening on schedule?

- delays in completion will show up in revenue, so if a quarter comes in significantly below implied delivery schedule, ask why

- repeat customers and contract extensions is a positive signal

5. How do they address it on earnings calls?

- this will be important to note, any ambiguity or defensive language is a warning sign

6. How is their gross margin trajectory?

- are they absorbing redundant costs, dealing w delays, or mismanaging capital?

- compressed margins will be a telling sign

7. How is their operating expense growth compared to their revenue growth?

- if open grows faster than revenue for multiple quarters

8. Is backlog converting to revenue at a normal pace?

- if backlog grows faster than revenue, it could imply delivery bottlenecks

9. Is there evidence of cross-subsidiary commercial activity?

- for example, an iron raider customer who upgrades to includes BIRD AMPS protection

- if you see multi product contract announcements, it means integration is working

————————————

When does integration risk stop being a concern?

It’s important to note that integration risk isn’t permanent and it comes in phases

- 0-6 months after M&A is highest risk

- 6-18 months after M&A the risk begins to decline

- 18-36 months after M&A the risk normalizes

- 36+ month, the risk is essentially gone

For Ondas, the tricky part is that the integrations have been staggered, so you have subsidiaries at different stages simultaneously

The risk will be concentrated on the most recent M&As, not the whole portfolio equally

————————————

My conclusion

The thing that mitigates risk the most is Ondas holding company model

When you don’t force operational integration, you dramatically reduce failure

There’s a clear operating vision driving the portfolio, so every company compliments each other and builds on top of the vision

The next earnings call will provide a lot of color on what to expect over the next year, but we’re still in the early stages of some of these more recent M&As

Expect a multi year timeline before we understand the full impact of these M&As

RocketMan@RKLBMan

$ONDS shareholder here. But when do we start to get concerned about constant M&A before they can actually integrate all of this stuff? It's not easy seamlessly absorbing companies into your business. Different cultures, tech platforms, geographies, overhead, etc to account for. For me, this barrage of acquisitions can also be a bad sign....

English

Why do people keep posting about the $ONDS short situation as if it’s something positive?

“The shorts are starting to understand” I see that every other day, yet short interest has actually increased.

Stop ignoring this and question @CeoOndas for once. Not everything is golden. All you’re seeing is the amount of PR.

He’s doing that for his own benefit, what have shareholders actually gained from it so far?

Are you really that blind, or do you not want to see returns as well?

English

@Bobebbop @ConvictionPoint I’m not expecting that, but surely I’m allowed to bring receipts for your previous statements? There are many more of them $ONDS

English

@StocksSucks @ConvictionPoint you can play that game all you want pal...won't stop me from posting

English

$ONDS last 10 days:

- Stronger prelim revenue

- $20 million border PO

- $6 million of new Sentrycs orders

- $15.8 million 4M demining order

- $10 million World View investment

- Mistral merger agreement

- BIRD Aerosystems acquisition.

Final Q4/FY25 results on March 25!

English

@ConvictionPoint and the stock has essentially gone nowhere. tells you its all priced in already... $ONDS is not worth 4.5 billion.

English

This Heidelberg partnership is bigger than many realize.

Europe is entering a massive defense capex cycle, Ondas gains local production capability, and Heidelberg brings 175 years of industrial manufacturing expertise.

Exactly the type of partner a small defense tech company needs to scale into billion-dollar contracts $ONDS

English

This Heidelberg partnership is bigger than many realize.

Europe is entering a massive defense capex cycle, Ondas gains local production capability, and Heidelberg brings 175 years of industrial manufacturing expertise.

Exactly the type of partner a small defense tech company needs to scale into billion-dollar contracts $ONDS

English

$ONDS $100M IN REVENUE ADDED TO 2026 GUIDANCE OVERNIGHT 🤯

Here’s exactly what happened 👇

Yesterday:

“Ondas also reiterates our full year 2026 revenue guidance of $170-$180 million. This guidance does not reflect any new acquisitions announced in 2026.”

Minutes later:

“Ondas Reaches Merger Agreement with U.S. Defense Prime Contractor Mistral Inc., Expanding Direct Prime Participation Across U.S. Department of Defense Programs”

Today, 2 separate analysts said this:

“Mistral is expected to add more than $100M to Ondas’s prior 2026 revenue target…”

Since 2025 earnings were technically pre-announced BEFORE the Mistral announcement, this line is critical:

“This guidance does not reflect any new acquisitions announced in 2026.”

Minutes later, they dropped the Mistral bombshell on us.

Today, Needham and HC Wainwright are telling you they expect this to add $100M+ to 2026 guidance.

This would result in $270M to $280M in revenue for 2026 🤯

Is management waiting for the earrings call to officially tell the world about this? 👀

English