Strata@strata_markets

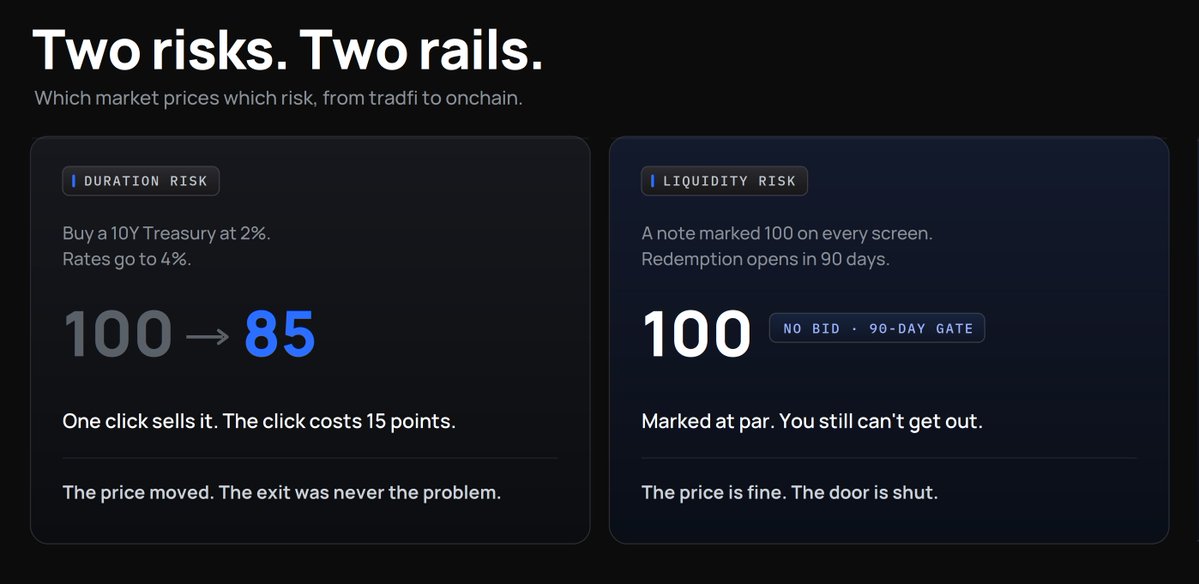

The real constraint on tokenized credit isn't credit quality. It's duration.

AAA tokenized paper is high grade, but it settles on the fund's clock: redemption windows running monthly to 180 days. Onchain capital wants a stablecoin-shaped exit: instant, any hour. Paper that can't offer that isn't pristine collateral, so it sits idle between the two poles that work: liquid dollars that loop and volatile assets that trade 24/7.

A liquidity layer is already forming to close that gap. @grovedotfinance Basin, @upshift_fi Clear, and @symbioticfi Liquid Lane front the exit so holders redeem at T+0 while settlement runs in the background, real progress on taking the lag off the holder's book.

Strata approaches duration from a different primitive: tranching, the securitization playbook that built CLOs and mortgage credit, gated behind accreditation for decades and now onchain and open. Every tranche does one job, split a single risk to fit a mandate: a protected senior with priority and instant exit, a junior paid to hold what the senior won't.

Strata already runs this playbook across multiple risk types.

1. Performance risk, at scale, on onchain dollars like @ethena's USDe.

2. Credit & counterparty risk, live, on @HastraFi's PRIME: exposure to @Figure's HELOC warehouse facility. mHYPER market, srmHYPER pays ~7–8% with ~170% coverage, a thick junior buffer beneath it posted by @hyperithm themselves. Skin in the game, aligned by construction. More originators landing soon.

3. Duration risk is what's being built now.

V2 makes it modular, and the point is that Strata splits the claim rather than just relocating the exit cash. Multi-strategy mode puts an interval-fund liquidity sleeve inside that split: the senior redeems in USDC from a liquid slice, the junior inherits the lockup and is paid a premium to hold it, so the duration cost lands on the party that chose it instead of being socialized.

Isolated mode goes further: the junior's own USDC pot is the senior's exit and loss buffer, so the senior is covered against duration, liquidity, even technical failure, because its exit never touches the underlying. AAA paper with quarterly redemptions becomes collateral.

The facilities move duration off the holder. Strata's aim is to price it, so duration becomes a market and the senior becomes collateral the rest of onchain finance builds on.