TIER Wealth

81 posts

TIER Wealth

@TIERWealth

TIER Wealth is built on a foundation of trust, deep relationships, and a commitment to always putting our clients first. Tax | Investment | Estate | Retirement

140 4 Avenue SW, Suite 1110 Katılım Mart 2025

55 Takip Edilen354 Takipçiler

If an RRSP or RRIF declines in value between the date of death and the date of final distribution to beneficiaries, the income reported on the terminal T1 would now exceed the actual amount received.

There is a fix for this.

File Form RC249 to deduct this post-death loss against the income originally reported on the terminal return. This is particularly relevant in volatile markets.

Without this filing, the estate effectively pays tax on income that was never actually received.

English

@bdkoepke It was adding pink streaks on the left side of our printed materials. This was unacceptable behaviour, and sadly it had to be destroyed by way of bat swings.

It also was not able to keep up with our printing demands as our office grew so we significantly upgraded.

English

@TIERWealth What did the printer do to deserve that? If it was an HP I’d understand, but that looked like a primo brother printer…

English

The market drops 3%.

The reactions jump 30%.

That gap? That’s where mistakes happen.

That’s why you don’t react on impulse.

That’s where a solid plan and a Portfolio Manager come in.

#OfficeSpace #Parody #MarketVolatility

English

Our first Quarterly Newsletter is out!

Each issue covers a topic related to Tax, Investment, Estate & Insurance. For our R-pillar (typically Retirement) we've decided to keep things interesting, so expect something Random, each newsletter.

tierwealth.com/newsletter/q1-…

English

As you can see here, probate fees vary (significantly) depending on the province.

This is why in Alberta nobody should create a trust simply to avoid probate, whereas this does happen in other provinces.

English

We actually have these guides customized for AB, BC, and Ontario.

The Alberta guide has 74 items, the B.C. guide has 77 items, and the Ontario guide has 76 items…. because there are very legitimate and meaningful differences.

Aaron Hector, R.F.P., CFP, TEP@AaronHectorCFP

If anyone in Alberta wants a very good executor’s guide… we just finalized a 7-page estate administration guide at @TIERWealth. Happy to share, shoot me a DM.

English

Buying a home is one of the biggest financial—and personal—decisions you’ll make. In this @globeandmail article, @AaronHectorCFP shares practical guidance on homeownership trade-offs and using FHSA/HBP wisely.

Read here: theglobeandmail.com/investing/glob…

English

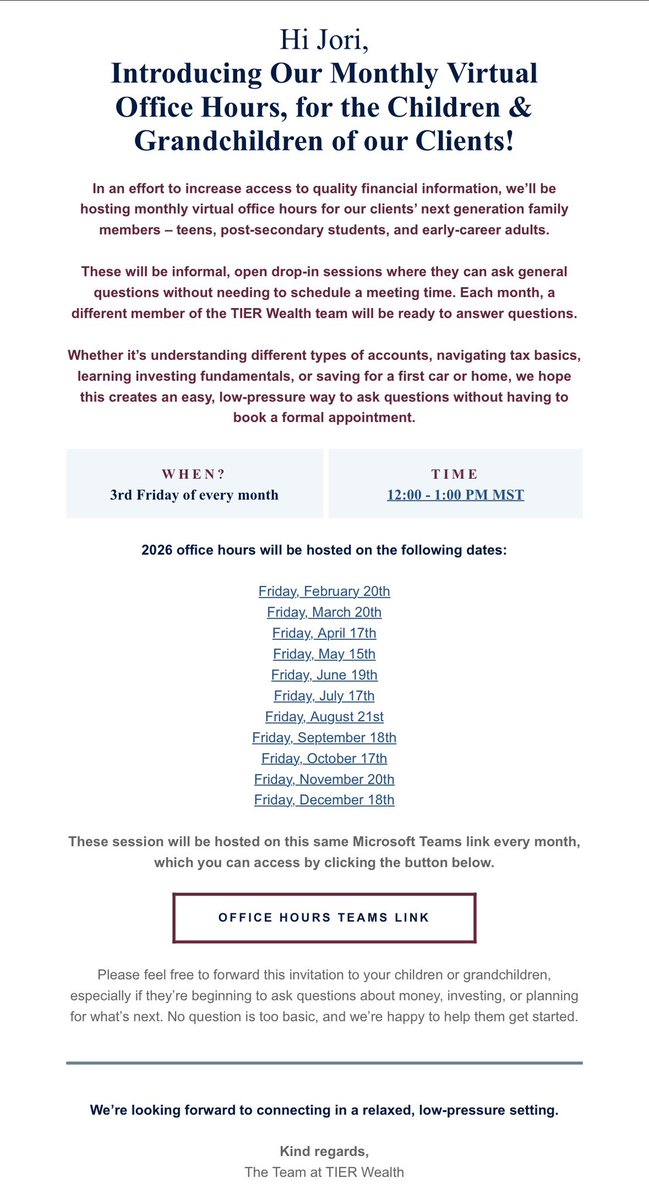

What a novel idea! It's so important to give our kids the tools the need to successfully steward generational wealth!

English

@TIERWealth @AaronHectorCFP Very good idea. I see the Office Hours service take off in the tech community, and such a great way to learn.

Great to see it take hold with financial planners and advisors.

English

I should also say - been debating something like this but almost an office hours or AMA for recent grads, newly graduated midwives etc

I have been trying to think of how to help that population in a way that is easy to tie into my regular work,

You doing this makes me feel like “ok I’m not alone in how I think about this”

English

@willbarreca People commonly underestimate tax drag. The dollars not invested in a RRSP - assuming TFSA is maxed - ends up having its income taxed annually in a non-registered account. Those tax bits that are shaved off to CRA annually add up over time.

English

A common retirement myth: your RRSP or RRIF can get too big.

Yes, withdrawals and your estate will be taxed, but along the way, you get tax-deferred growth

Focus on the big picture: the goal is to grow your after-tax wealth, not just minimize taxes

English

TIER Wealth retweetledi

Today at @TIERWealth we had a Teams meeting with a client’s daughter who is in her early 20s.

We talked about:

- how some of the withdrawals that come out of her parent’s RESP are taxable to her, but others aren’t.

- what her plans were for summer employment and how much she might make so we could use that in our RESP withdrawal planning conversations we’ll have with her parents.

- we guided her along in a discussion to determine her risk tolerance, in other words, what was her willingness and ability to take on risk as an investor. We explained investing fundamentals like risk and return, and how time horizon works into this as well.

- we knew we were going to open a TFSA and RRSP, but we discussed the pros and cons of a FHSA at this time. After our discussion, we opted to not open a FHSA as it was unlikely to be significantly funded, and we didn’t want to start the 15 year clock just yet.

- we made a plan to have current contributions go into the TFSA because her income is low.

- we talked about how her (very small) accounts would be reported to her separately for privacy, but for fee calculation purposes they would get pooled together with her parents (much larger) accounts. This provides a low fee access point for her that she couldn’t have gotten on her own. As her portfolio grows, she will help her parent’s fees decline as well because they all work together.

- we explained what a beneficiary was, and asked her to choose a beneficiary for her new accounts. She named her sibling.

- we explained the importance of a Will, Power of Attorney, and a Personal Directive, and offered to give her a code to prepare documents online with ‘willful’. I said when the time was right, I’d be happy to talk her through this process. We wanted to help to make sure these important things happened because they are important, even at her age.

(TIER Wealth approached Willful last year to explore synergies, and we became the first company in Canada to onboard into their Willful for Professionals service. We pre-purchased wills for the purpose of offering them to our client’s children who have simple estate needs.

In the past I had given advice to client’s that their children should have these documents, but it never seemed to get done, so we decided to do something about it.)

- we talked about the upcoming tax season and that we would be preparing her tax return and what to expect for communication in the next months.

- after the meeting, the paperwork to open her accounts was sent out via email through Docusign. Assuming she signs over the weekend, the accounts should be open on Monday.

At @TIERWealth we’ve put a lot of intentional thinking into exactly how we can help not only our clients, but the children of our clients. It’s about having the necessary conversations that are important to get started. It’s about looking after the important details that so often fall through the cracks. It’s about providing an early education. It’s about helping to ensure that your financial legacy will be well looked after if something were to happen to you.

In fact, we even have this next-generation service model listed on our website, it’s called the Foundation TIER, and it’s one of the things we’re the most proud of.

English

Wishing you a season of peace, reflection, and time well spent.

Happy Holidays from TIER Wealth!

English

@smaugizbored @AaronHectorCFP We may need a dragon on staff one day to make sure we don’t make such foolish mistakes

English

A one page RRIF minimum withdrawal explainer.

TIER Wealth@TIERWealth

Have you ever wondered how RRIF Minimum Withdrawals work?

English

@smaugizbored @AaronHectorCFP Thank you for expressing your interest in a career at TIER Wealth.

We will let you know if we have an appropriate position in the future.

Until that time, the dragon-friendly team at TIER wish you the best!

English

Outside the office, you’ll find him tackling endurance challenges as a 2x Ironman finisher or exploring the world (visiting 36 countries and counting)!

Join us in welcoming Kevin to the TIER team!

English

Kevin holds both the CFP® and CIM® designations and is passionate about helping clients elevate their financial lives.

A born-and-raised Calgarian, Kevin is a dedicated family man with a two-year-old daughter and another little one arriving in February.

English

We are excited to welcome Kevin Langman as the newest Wealth Advisor at TIER Wealth! 👏

With 10 years of experience in financial services, Kevin brings deep knowledge in delivering thoughtful, holistic financial planning.

English

In our latest blog, we explore two scenarios where making an over-contribution to your RRSP in December can make sense. tierwealth.com/blog/two-smart…

English