Dr. Ganesh Kumar Ammannaya@DAmmannaya

FERMENTA BIOTECH - Interesting Stock Idea that merits further research.

(NOT A RECOMMENDATION / NOT INVESTMENT ADVICE, Merely a Stock Idea for further in-depth Study)

Currently trading at merely 8 PE on TTM EPS Rs 38.06 (Historical PE - last 10 yrs Mean PE 19.40, Lifetime avg PE 15).

ROCE 23%, ROE 24.9% (EBIDTA margin H1 FY26 25.9%) with excellent H1/Q2 FY26 Nos.

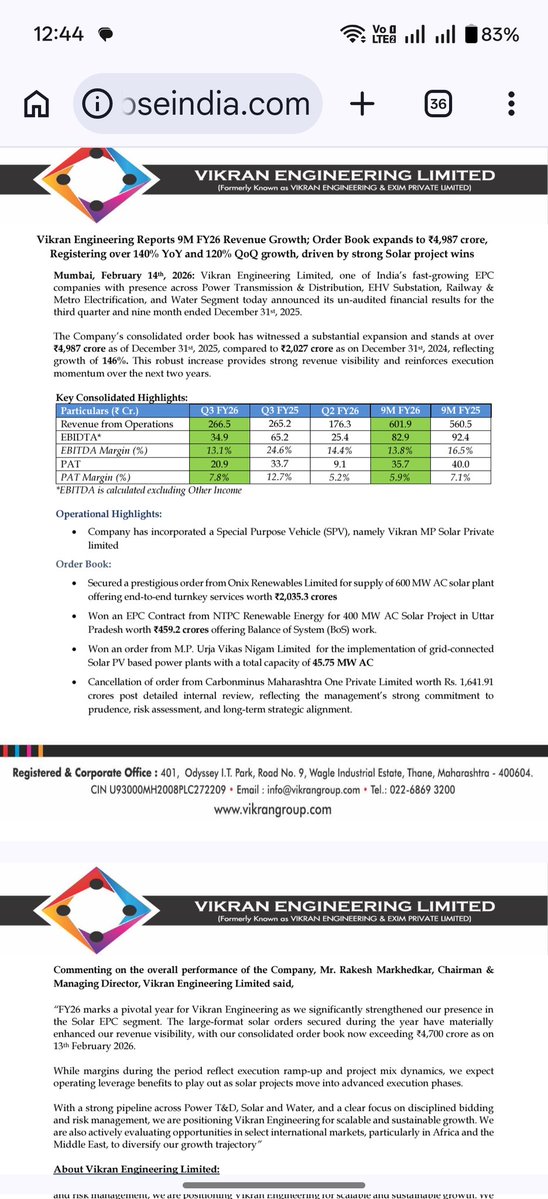

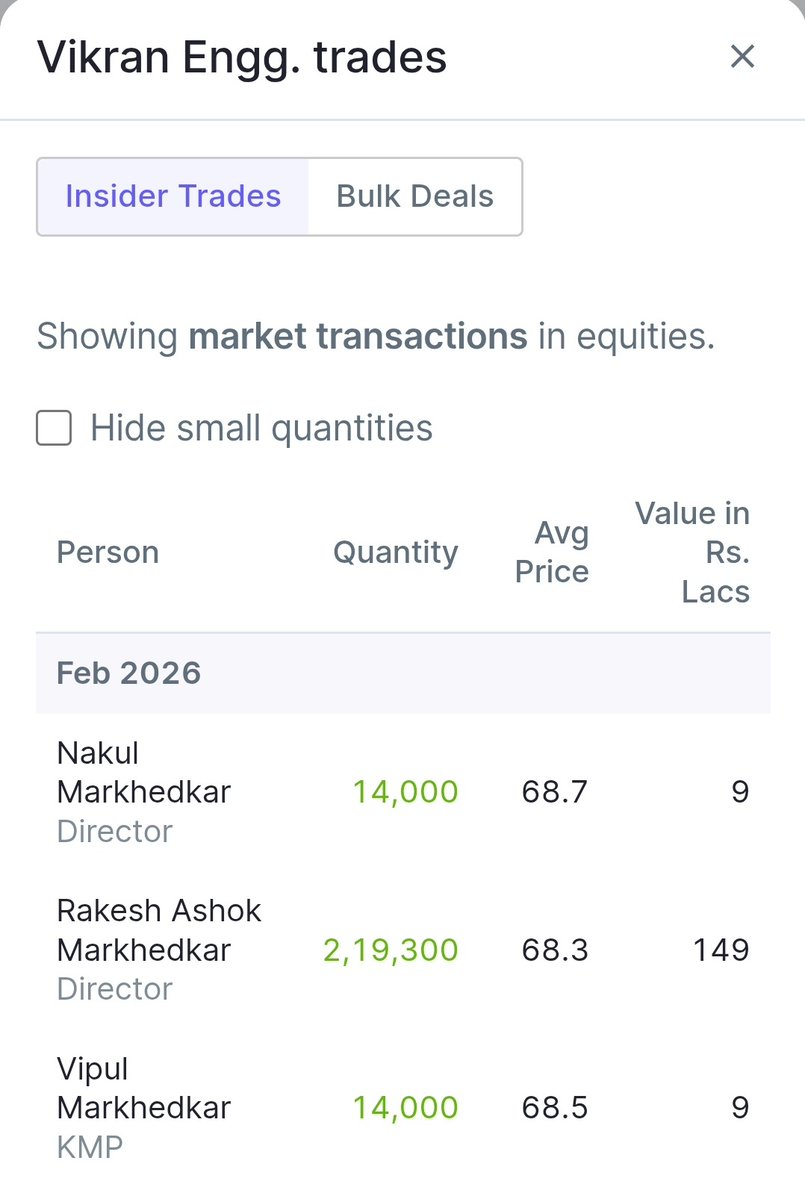

LATEST Development - (first 2 images) of MAJOR CAPEX.

VITAMIN D3 Moat - World leader (among Top 3 & the Only Indian Co) in Vitamin D3 (niche player)

Recent PATENT for its plant based (Vegan) Vitamin D3 expected to significantly expand margins as these command much higher premiums (image 3 gives a very rough idea about premium margins), expected to be a Key Growth Driver in core business, also for which CAPEX is primarily planned for this FY26 & FY27.

Increasing awareness worldwide about role of Vitamin D3 in virtually every organ system of human body, ill effects of its deficiency such as increased cardiovascular risks, infertility & recent European studies showing improved survival in Cancer patients on Vitamin D3 supplements, apart from proven benefits such as anti-ageing, anti cancer & immunity boosting effects, one of the mainstays in the treatment of osteoporosis (weak bones particularly elderly) etc., augurs well for wide scale use across all geographies.

Scale Up in GERMAN Operations - H1 FY26 revenue 34.3 Cr (Up 194% YoY) & EBIDTA 7.7 Cr (Up 103% YoY).

- Overall EU share increasing to 29% (from 27%),

- US share dropping to 13% (from 15%).

- Rest Domestic - 40%,

- Others-18%

Expanding to Other Vitamins - Vitamins K1 (one of the few global suppliers), Vitamin- fortified Rice (Govt schemes, like in AP) with plans of Vitamin A, E over next 5 yrs.

MoU with NIFTEM to establish Centre of excellence for Food Fortification enhancing public nutrition.

Additionally, Environmental solutions including Waste WATER management. fermentabiotech.com/environmental-…

Co seems to be focusing keenly on this segment as evidenced by further investment of Rs 7.9 Cr more recently in the subsidiary.

Result of this increased focus on Environmental Solutions Subsidiary Visible as - H1 Revenue up 127% in H1 FY26 (to 15.1 Cr, from 6.6 Cr YoY).

Co has been unlocking Value from Real Estate well. Has excellent LAND BANK primarily in Thane 5.5 acres (apart from Thane One) & 45 acres in Takwe, Pune, alongside steady leasehold income like Thane One.

Debt levels cut down more than half from 239 to 112 Cr, with Turnaround Positive Cash Flow.

Promoter stake has increased steadily from 59 to 64% over last 2 yrs with No of Retail shareholders coming down from 17 K to 13 K during times of extreme stress for the Co until the recent Turnaround.

Technically, C&H with probably a “W” shaped Bottom (256, that’s a DOUBLE BOTTOM, also the Key Support) in the handle seems supportive & Key multi-year resistance being (also ATH) ~450, which it tested 2-3 times in the last 7 yrs.

Thus, makes a case for further in-depth research.

(NOT A RECOMMENDATION / NOT INVESTMENT ADVICE, Merely a Stock Idea for further Study)