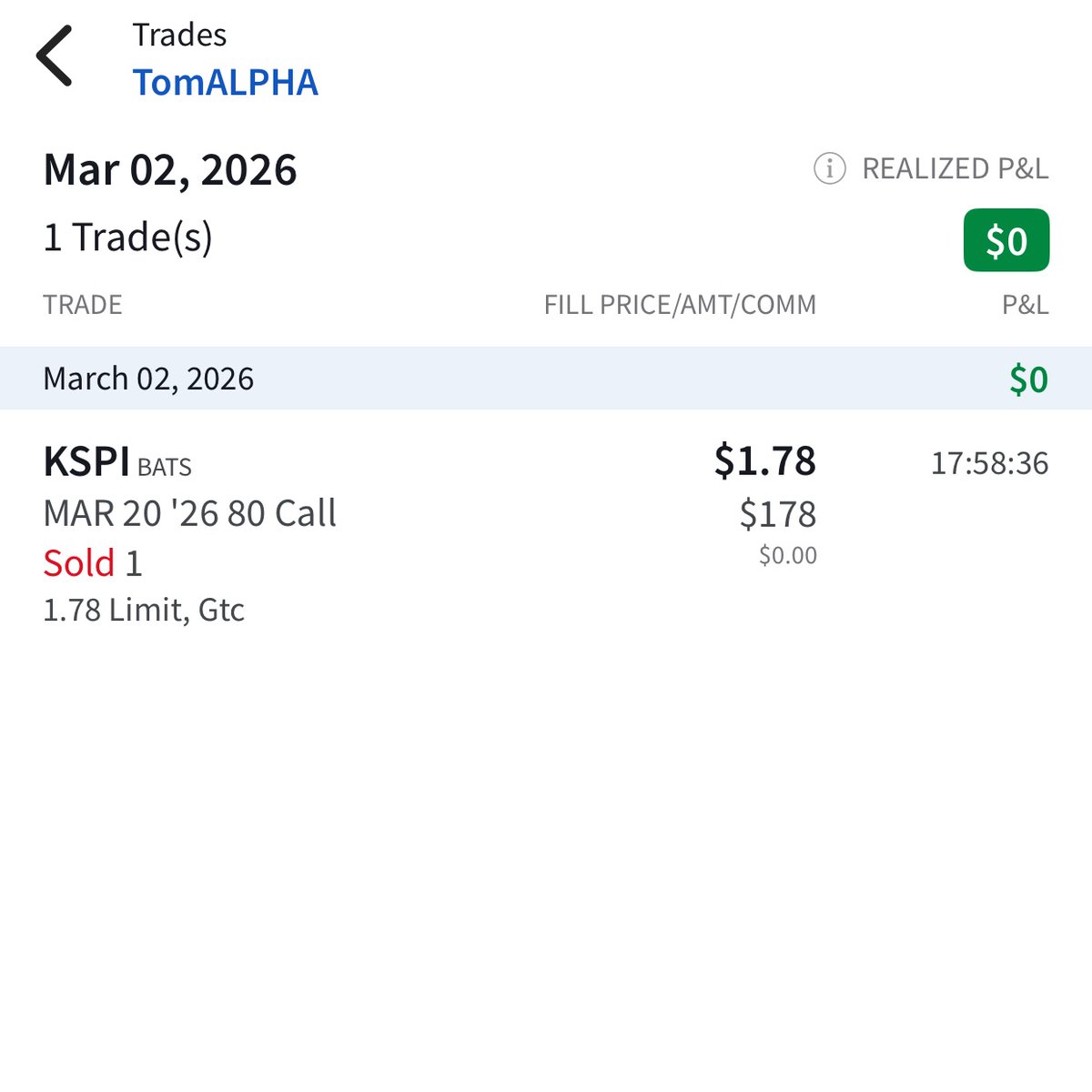

Sabitlenmiş Tweet

📈 Portfolio Update – February 17, 2026 📈

Real money swing trading results since inception (April 5, 2021):

TomALPHA: +338.12%

SPY: +67.77%

-Asymmetric risk/reward focus: fintech, payments, and undervalued growth.

- Real brokerage screenshots on every fill. Patient through drawdowns.

- Portfolio currently hedged with 3 written SPY PUT options for downside protection. No hype, no noise.

🔥 Top 7 positions by weight:

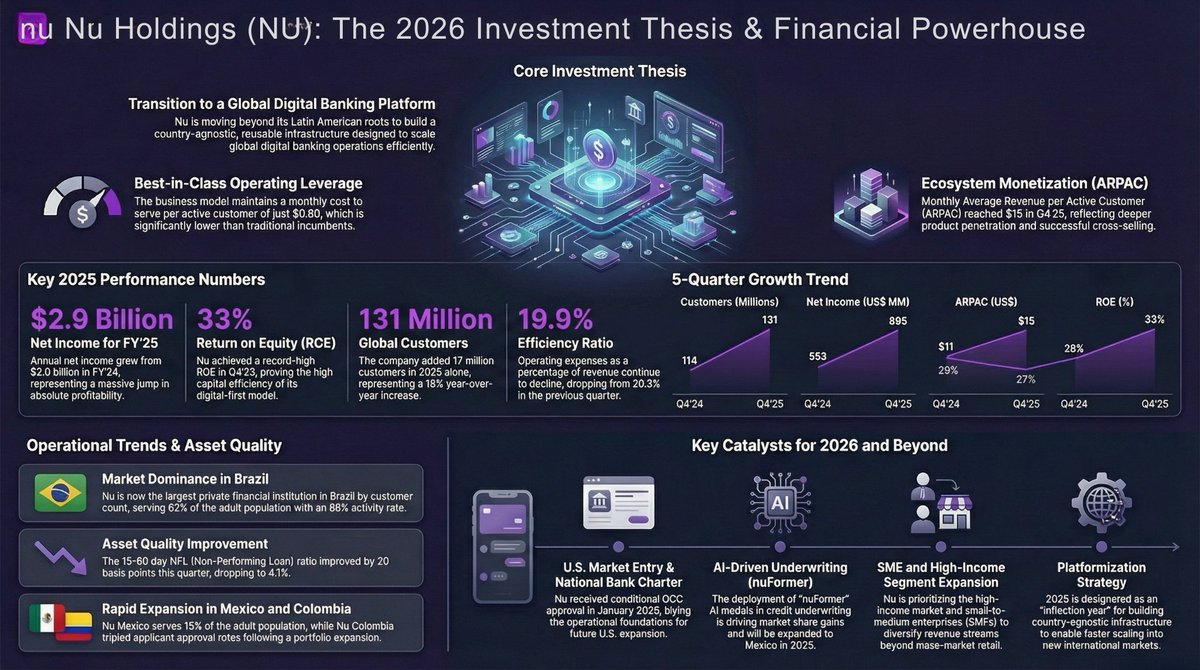

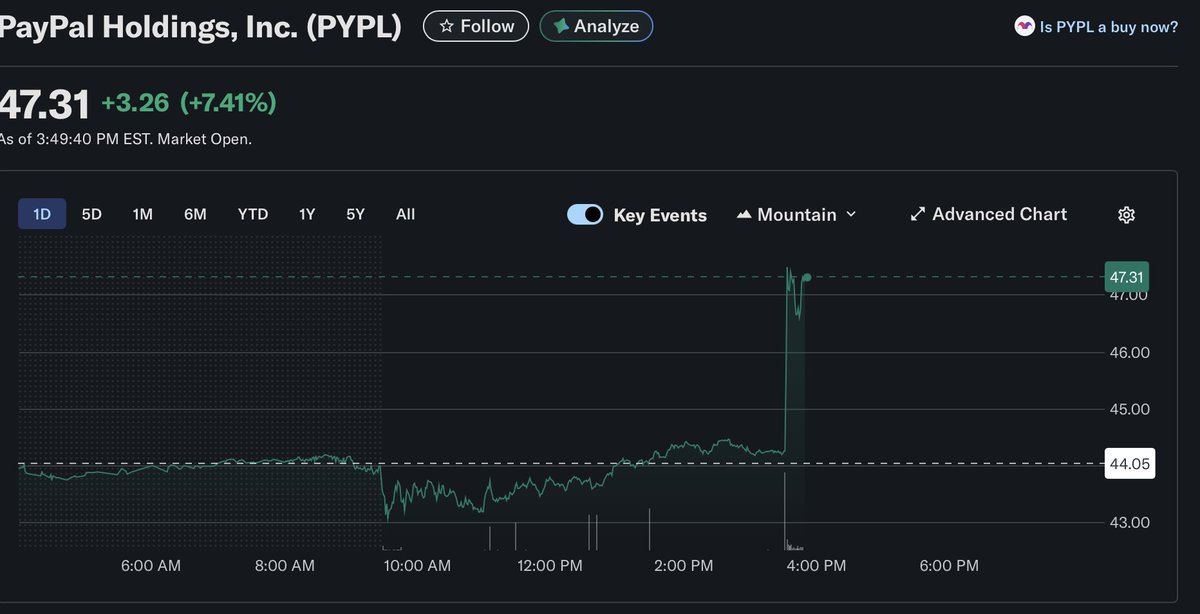

• $PYPL – 12% (target $80 → +99%)

• $S – 10% (target $28 → +102%)

• $EEFT – 8% (target $165 → +143%)

• $ZAL – 8% (target €34 → +57%)

• HKG:0175 (Geely Auto) – 8% (target HK$24 → +41%)

• $BABA – 7% (target $215 → +36%)

• $DIDIY – 7% (target $7 → +52%)

Highest conviction upside plays right now: $EEFT (+143%), $S (+102%), $PYPL (+99%), and several others with 60-140% potential.

Continuing to average down selectively on multi-year lows where fundamentals remain strong and valuations are historically attractive.

Which of these looks most compelling to you? Best risk/reward? 👇

Not financial advice. Past performance no guarantee of future results. Investing involves substantial risk of loss.

Full portfolio breakdown, deeper models & real-time updates → tomalphatrades.com

#Fintech #SwingTrading #ValueInvesting #Payments

English