Treasury Hub GH@TreasuryHubGH

📊 March T‑Bill auctions are off to a roaring start.

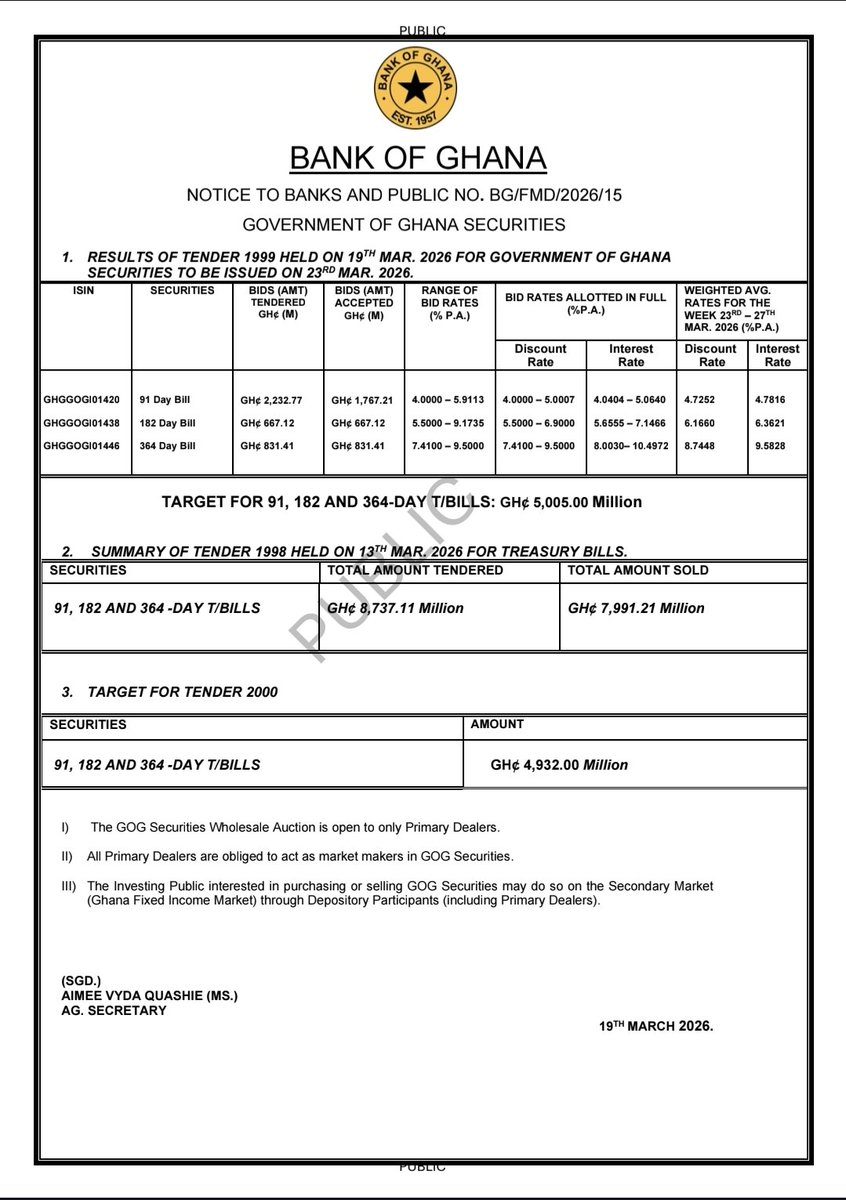

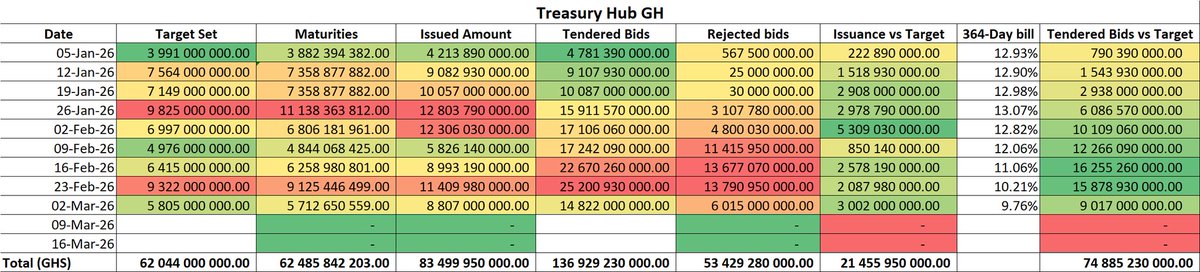

The first Treasury bill auction for March opened with a GHS 5.8bn refinancing target against maturities of GHS 5.7bn—but investor appetite came in well above expectations.

By auction close, total bids surged to GHS 14.8bn, with government taking up GHS 8.8bn and GHS 6bn left on the sidelines. A clear signal of robust liquidity and strong demand for short‑dated paper.

✅ Yields compressed across the curve, with all tenors clearing firmly into single‑digit territory:

91‑day: 5.32%

182‑day: 6.98%

364‑day: 9.76%

Year‑to‑date, T‑bill issuance has hit GHS 83bn versus GHS 62bn in maturities, translating into a net expansion of GHS 21bn in the T‑bill debt stock.

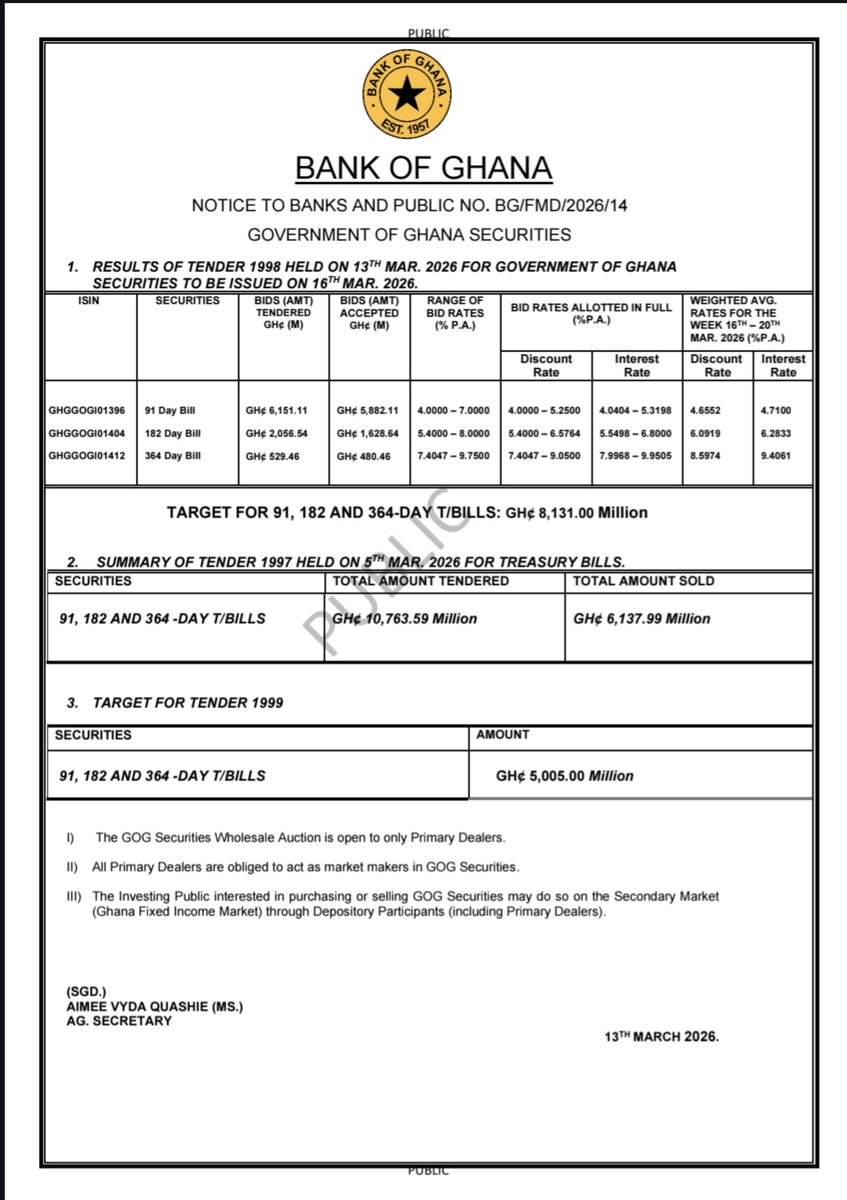

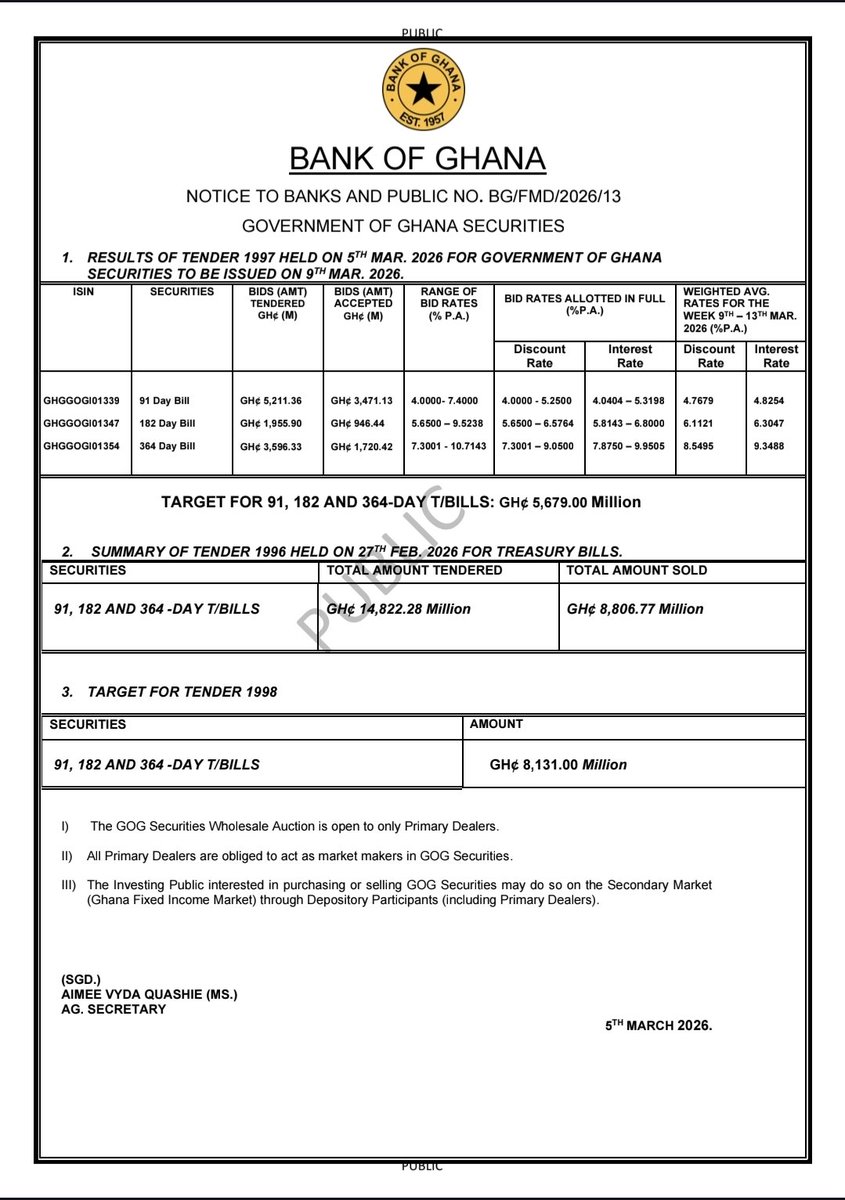

🔥 February was a standout month, with total bids ballooning to GHS 82bn, more than double January’s GHS 40bn—a strong confirmation of sustained demand and deepening market participation.

On the secondary bond market, the week wrapped up on a bullish note as yields eased by ~200bps across the curve. Excess cedi liquidity continued to drive strong demand for longer‑dated bonds, pushing prices higher.

🔭 Looking ahead:

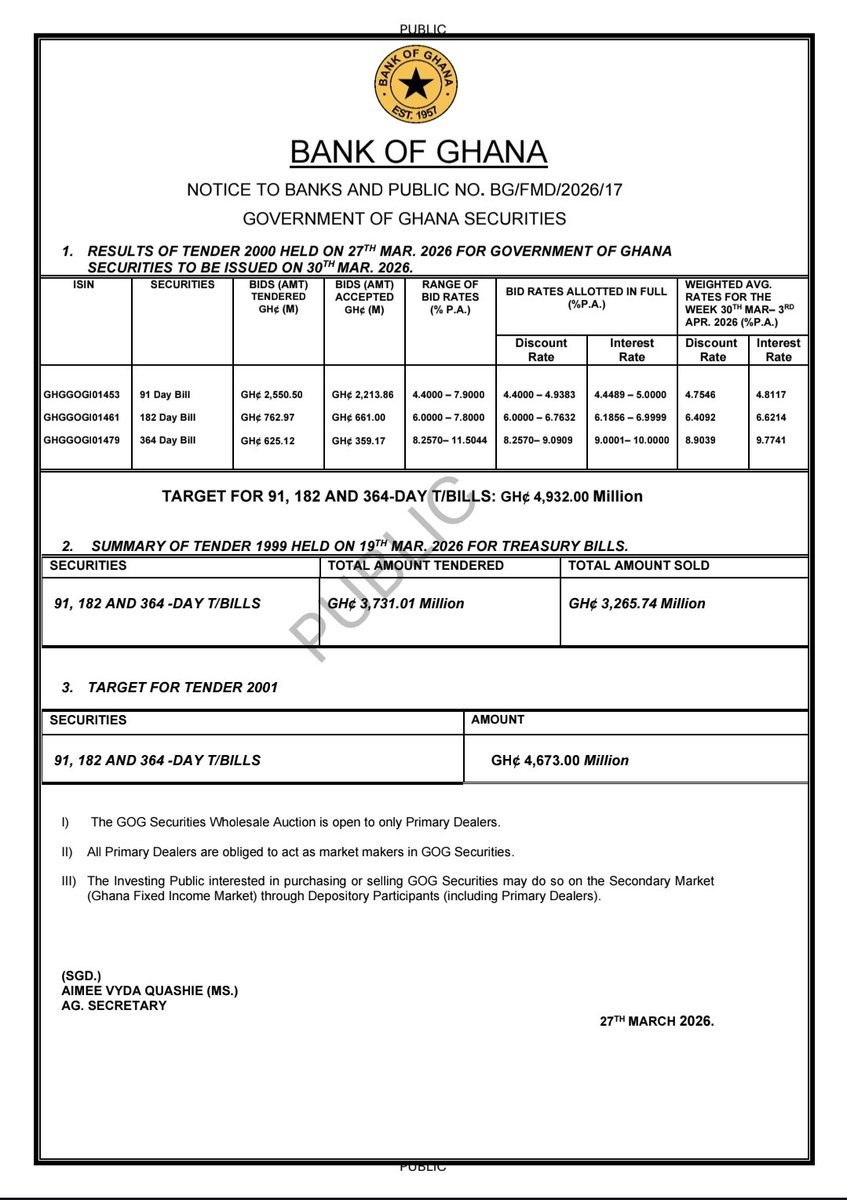

Next auction targets GHS 5.7bn against maturities of GHS 5.6bn—setting the stage for another closely watched liquidity test.

#FixedIncome #TreasuryBills #BondMarket #CapitalMarkets #GhanaMarkets #Liquidity #YieldCurve #MacroWatch