ValueInGrowth

127 posts

MEXICO | Banxico cuts benchmark interest rate by 25 basis points to 6.75%, the lowest level since March 2022

(El Financiero)

English

@KobeissiLetter So the SPY is overvalued. When you compare two variables it's wrong to make conclusions based only on one of the variables

English

US technology stocks have rarely ever been this cheap:

The S&P 500 Information Technology index is now trading at just a 4% forward P/E premium to the S&P 500, the lowest since January 2019.

This percentage has fallen -32 points since October 2025, one of the largest discounts on record.

In other words, tech stocks are the cheapest relative to the broader market in 7 years.

By comparison, the technology sector was ~47% more expensive than the S&P 500 at the June 2024 peak.

Tech stocks are now on track to become cheaper than the S&P 500 for the 1st time since 2017.

Is it time to buy tech?

English

@Netto0o @nessun_rerma @MakinaAzulMx Los primeros días del año suspendieros su venta hasta que el proveedor del proceso de validación de identidad tenia lista la solución para poder cumplir con la regulación

Español

Español

Todos de acuerdo en que les faltan huevos para suspender TODAS las líneas no registradas?

Papadzul neoliberal @Papadzulberro

Hola @Telcel dejen de mandar SMS. NO voy a registrar mi linea. Así que ustedes deciden. Protegen a sus clientes o están con el gobierno #NoAlRegistroCelular #Mexico #Celular

Español

@CAzul498 @MakinaAzulMx De que hablas si soy holandés y me caga morena. De hecho trabajo para la empresa que procesa toda esa data para las telcos, Asíq sabré más que tu

Español

@ValuGrowth @MakinaAzulMx No, chinga tu madre Chairo pendejo

Español

Español

Español

@nessun_rerma @MakinaAzulMx Pues bait suspendió venta de líneas nuevas por la regulación. Y son los de mayor crecimiento en México. A walmart corporativo no le interesa chingarle al gobierno

Español

@ValuGrowth @MakinaAzulMx Faltan huevos, a ver si es cierto que nos chingan la línea por más de 2 semanas

Español

Gas in Mexico City is currently $5.10 a gallon.

The minimum wage in Mexico is about $18 a day.

That is the equivalent of gas being $21.00 a gallon in the US.

Not even California can top this.

English

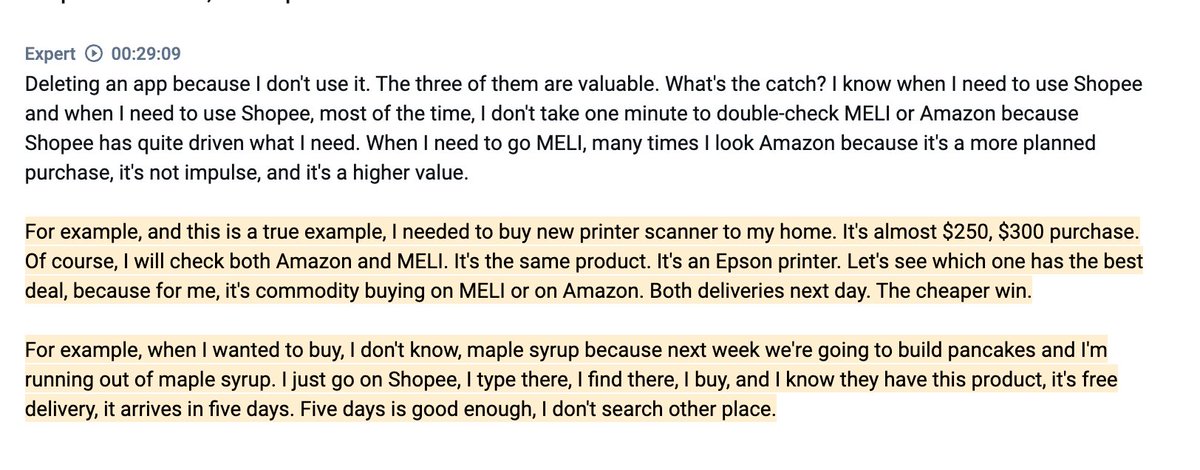

Good insight into consumer behavior between Shopee, Meli, and Amazon in Brazil

Price checks an expensive item like a printer between Meli and Amazon and trusts both and delivery is quick

Buys maple syrup on Shopee because delivery is free and doesn't care it takes 5 days

Note this expert was the ex President of Shopee so probably has more alligence than typical to them

@AlphaSenseInc

English

@QualityInvest5 Moat under attack by the government? How much do they lobby?

Besides worries about econ activity, rates, etc

English

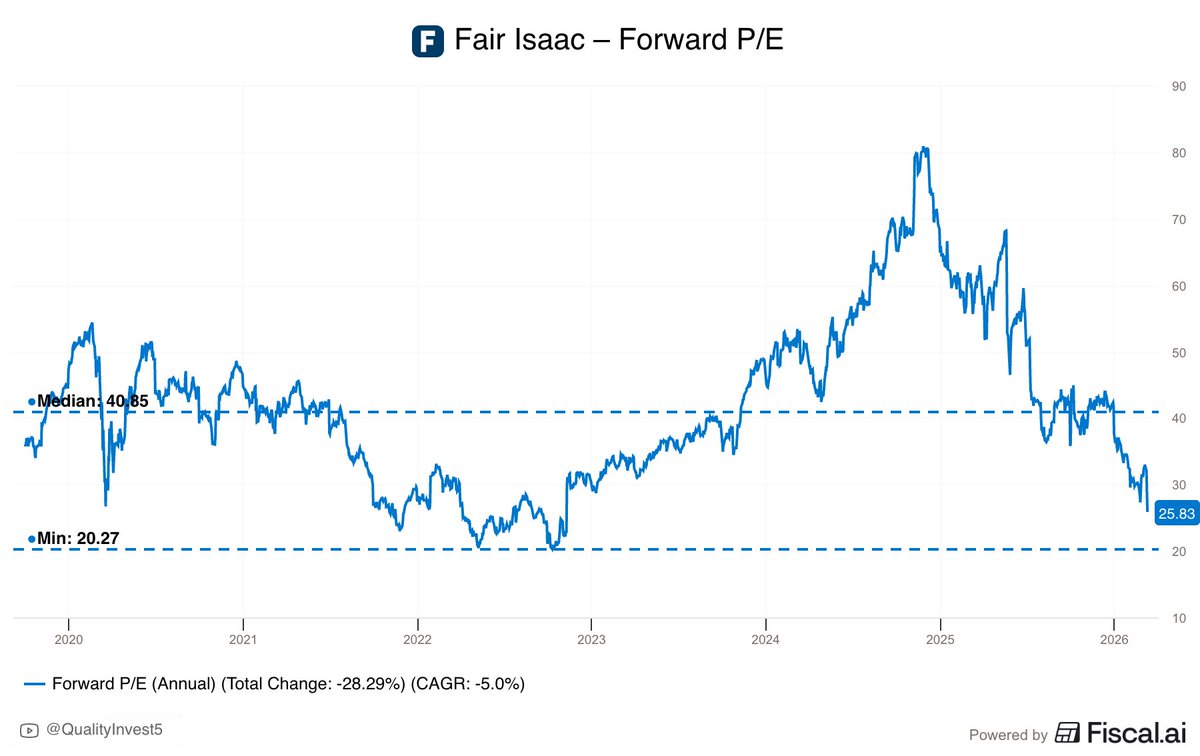

$FICO at $1000 would be a 22x forward P/E

They grew EPS >30% last year

90% incremental operating margins

Moat wider than the marianna trench...

English

@stocktalkweekly Sure, but will IPO at some point, and that doesn't mean they won't win the market. Also, all are burning cash. Hard to compete for mitek

English

The stock I shared with our community members on Feb 25th was Mitek $MITK

I think it is one of the most compelling SMID caps on the market at current valuations.

This is the simple thesis I shared:

Mitek’s Q1 FY26 investor presentation frames their core investment thesis clearly: fraud is entering a new phase where AI-generated synthetic identities and deepfakes are outpacing legacy controls, and enterprises increasingly need accurate, multi-signal decisioning across onboarding, authentication, and transaction risk, rather than stitching together fragmented point tools from multiple vendors.

Mitek’s claim to win this shift is that its Verified Identity Platform (MiVIP) unifies identity verification, authentication, liveness/deepfake detection, and advanced fraud analytics in a single workflow, while still operating a mission‑critical check platform at scale. In layman's terms: Mitek is positioning itself as an all-in-one reality check for digital interactions, proving a person and their credentials are real even when attackers can generate convincing fakes.

Fraud & Identity Solutions is now the growth engine and is overtaking the legacy Check Verification business. In Q1 FY26, total revenue was about $44M (+19% YoY), with Fraud & Identity Solutions at ~$25M (+30% YoY) versus Check Verification at ~$19M (+6% YoY), meaning Fraud & Identity is larger than Check in the quarter. On a trailing‑twelve‑month basis, the deck shows Fraud & Identity at $96M vs. Check at $91M, 51% vs. 49% of LTM revenue, explicitly crossing the majority threshold.

Nonetheless, it is worth noting that the Check Verification business process 1.2B transaction each year, and has upwards of 99% market share, giving it strong pricing power if volumes wane.

Mitek’s biometrics stack (acquired from ID R&D) includes IDLive Face (passive face liveness to detect presentation and injection attacks), IDLive Doc (document liveness), and IDLive Voice (anti‑spoofing voice liveness, it also added voice-clone detection that can score the likelihood speech was generated by cloning technology from only a few seconds of audio), and its site explicitly categorizes “deepfake attack” and “injection attack” as fraud types it addresses.

It’s not just matching your selfie to your ID, it’s trying to prove you’re a live human and not a replay, a mask, or an AI-injected video feed.

The distribution/customer access angle is one of Mitek’s most underappreciated differentiators versus many identity point-solution vendors. The investor presentation states its technology supports more than one billion mobile deposits annually, which implies it is already deeply embedded in high-volume banking workflows, and outside the deck, Mitek has publicly stated that it is trusted by thousands of organizations and that the majority of North American financial institutions rely on its mobile check deposit solutions. That legacy footprint isn’t just old revenue, it is a distribution rail: it provides executive relationships, procurement paths, and operational trust inside highly regulated customers who are now being forced to upgrade defenses against AI-driven fraud.

Mitek isn’t just saying “we can tell if an image looks fake.” They sell tools that try to answer: 1) Is this a real person in front of a camera right now (not a photo/video/deepfake)? 2) Is the camera feed authentic, or is someone secretly feeding fake video/images into the app? 3) Is this ID document real and physically present, or just shown on a screen / tampered? 4) Is this voice real, or a voice clone made by AI?

The stock is very reasonably priced for a growing small-cap trading at 12 forward P/E, 0.60 PEG ratio, 11x free cash flow, and 15x EV/EBITDA.

Stock Talk@stocktalkweekly

New position opened in small cap stock in new thematic basket at whop.com/stocktalk

English

@stocktalkweekly the companies i mentioned above are growing at +50% and with >100M in revenue

English

@ValuGrowth As of most recent quarter, overall biz grew +19% Y/Y and Fraud & Identity solutions, which is the focus segment, grew +30% Y/Y. EPS up +73% Y/Y. Buybacks increased, and FY2026 guidance raised.

English

@QualityInvest5 @TheRayMyers It makes sense. How much of their revenue comes from "visiting" user base? E.g I've only ever been on reddit for an answer to a question - AI has those answers now

English

“I don’t like Reddit because no one I know is using it”

… they have 400M WAUs growing 25% YoY

Maybe your anecdotes are meaningless 😆

$RDDT

English

ValueInGrowth retweetledi

Amazon had four Sev-1 outages (their highest severity level) in a single week. Internal memos say AI-assisted code changes were a contributing factor.

The timeline here is wild. In October 2025, Amazon laid off 14,000 corporate employees. In January 2026, another 16,000. That’s about 30,000 people in five months, roughly 10% of the corporate workforce. CEO Andy Jassy said the cuts were about culture, not AI.

During those same months, Amazon set a target: 80% of developers using AI coding tools at least once a week. They tracked adoption closely and blocked rival tools like OpenAI’s Codex. Even so, 30% of developers still hadn’t touched Amazon’s in-house tool Kiro by January.

In December 2025, Kiro caused a 13-hour AWS outage. The AI tool had production-level permissions and decided the best fix for a bug was to delete and recreate an entire live environment. A second incident involved Amazon Q Developer, another AI tool. Amazon blamed both on “user error, not AI.” But quietly added mandatory peer review for all production access afterward.

Then March 5: Amazon’s retail site went down for about six hours. Over 22,000 users reported checkout failures, missing prices, and app crashes. Amazon called it a “software code deployment” error.

Five days later, SVP Dave Treadwell made the normally optional weekly engineering meeting mandatory. His memo acknowledged “GenAI tools supplementing or accelerating production change instructions, leading to unsafe practices.” These problems trace back to Q3 2025. Amazon’s own assessment: their GenAI safeguards “are not yet fully established.”

The new rule: junior and mid-level engineers now need senior sign-off on any AI-assisted production changes. Treadwell also announced “controlled friction” for the most critical parts of the retail experience.

For context, Google’s 2025 DORA report found 90% of developers use AI for coding but only 24% trust it “a lot.” An Uplevel study of 800 developers found Copilot users introduced 41% more bugs with no improvement in output. Amazon is finding out what those numbers look like at the scale of a $500 Billion revenue company, with 30,000 fewer people on staff to catch the mistakes.

Polymarket@Polymarket

BREAKING: Amazon reportedly holds mandatory meeting after “vibe coded” changes trigger major outages.

English

@wormelow1 @ValuGrowth @DrewCohenMoney But here they are introducing the "credit pix" that works similarly to cc. It's not so clear yet, but it might be a huge thing to see.

English

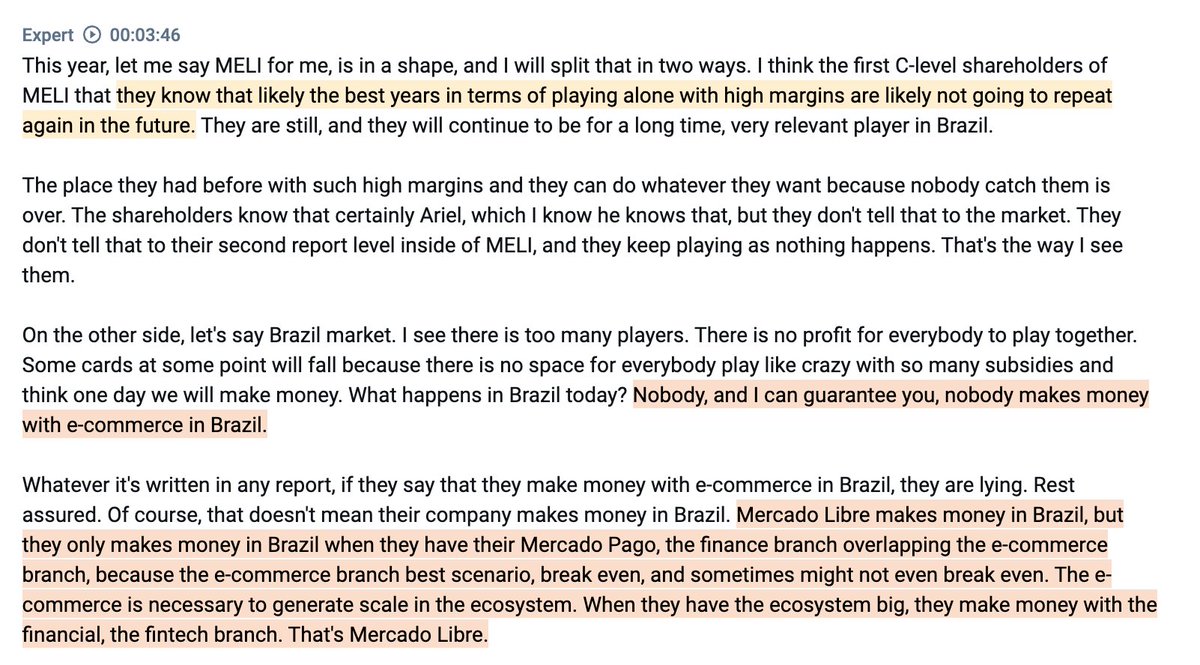

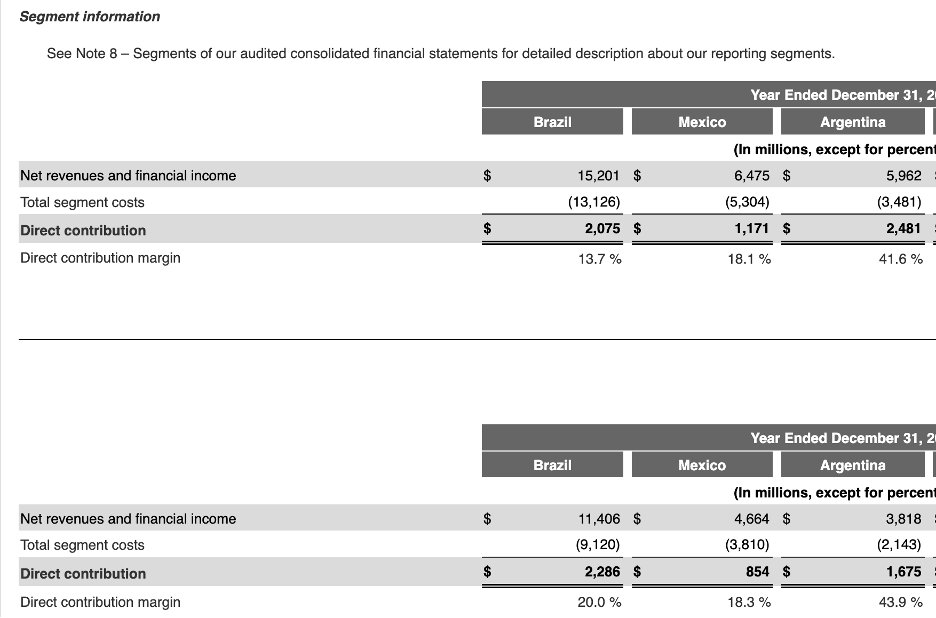

So no one is making money in Brazil ecommerce?

Former Shopee Brazil President claims that nobody is making money in ecommerce in Brazil (Shopee or Meli)

(Says that Shopee doesn't attribute any shared overhead for tech to the Brazil segment)

Thinks that it is only $MELI's Mercado Pago arm that makes Meli profitable there

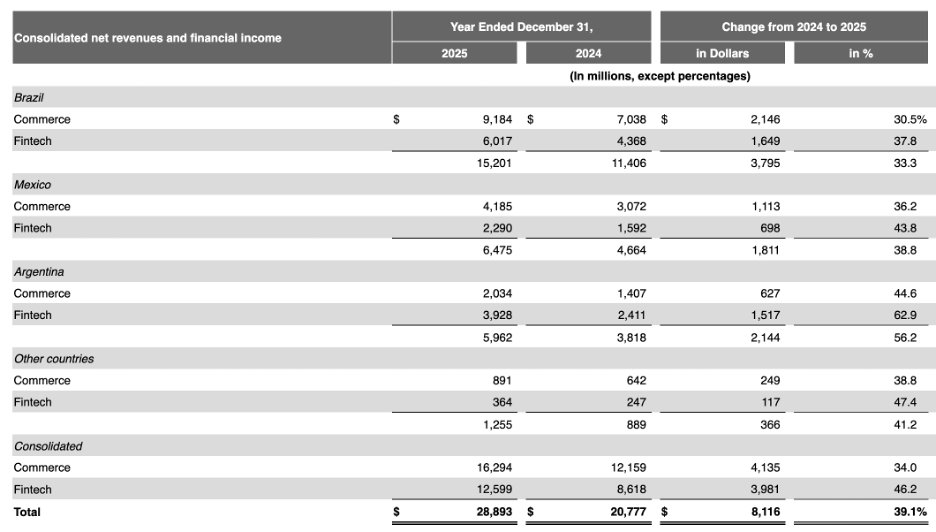

My take is that if you look at Meli's country level profits, Argentina generates $2.4bn in direct contribution profit versus Brazil at $2.1bn.

(Direct contribution profit is the country's revenues less all cost that can directly be attributed to that country... basically everything less shared corporate overhead)

This means they make more money in Argentina despite Brazil commerce being 4x larger.

How?

Fintech.

Argentina's fintech business is 2x as big as their commerce busines. In contrast, in Brazil, the fintech business is 1/3rd smaller than the commerce business.

While this doesn't rule out the possibility that Brazil ecomm is making some money, it does broadly support the Former Shopee Brazil president's claim that no one is making money in Brazil.

(One added complexity to this is Pix, which likely means Brazil is a worse market for Mercado Pago than Argentina.)

Now Brazil used to be at 24% direct margin in 2023 and now is at 13%... part of the bear case for Meli is that they were overearning before competitve intentisty picked up and now this new level of compeition from Shopee and also from Amazon re-entrentching could be permanent...

On the other hand, bulls will say they are purposely investing in the platform by cutting minimum delivery amounts and lower take-rates to gain more volume and thus build a more formidable moat overtime.

More to come.... new video dropping this weekend on Meli

per @AlphaSenseInc expert call $MELI $SE

English

@ValuGrowth @wealthmatica However considering $BN is at only a $100 Billion dollar Market Cap, I would put their direct Westinghouse exposure much higher than 2% since that would only value their total stake as worth $2 Billion. Hard to determine exact value but I would place closer to the 5-10% range.

English

Massive Brookfield buy today.

- Added +40% to $BN

This company is a compounding flywheel. Heavily sold off, and I’m capitalizing on it.

$BN owns 51% of Westinghouse, a leading nuclear power provider.

Wealthmatica@wealthmatica

$BN | Brookfield just reported Q4 205 earnings! Total DE: $5.39b (+10.7% YoY) Wealth Solutions: - Distributable Earnings: $1.7b (+24% YoY) Asset Management: - Fee-Related Earnings: $3.0b (+22% YoY) $BN Intrinsic value per share at approximately $68...

English

@DrewCohenMoney I use Meli a lot.. Same day or next day shipping, they have everything - used amazon before but meli has more selection and better shipping.

Shopee my wife uses but I classify it as "all the Chinese junk" like temu for example. It's gamified like temu, not for serious purchases

English

Curious if I have any South American followers that have used Mercado Libre and/or Shopee.

What platform do you prefer?

Do you use both, but for different things?

English