Sabitlenmiş Tweet

Poucas coisas mostram tão escancaradamente a limitação intelectual de alguém quanto a atitude de rotular outrém como forma de argumentar.

Português

Victor T.N.

598 posts

@VictorTN_83

The world is changed by our actions, not by our opinions

One of Korea’s leading semiconductor scholars, Professor Seokjun Kwon of Sungkyunkwan University’s Department of Chemical Engineering, said in an interview with Korean media today that China could secure advanced semiconductor manufacturing equipment approaching extreme ultraviolet, or EUV, lithography tools by around the mid-2030s, despite being blocked from accessing them by U.S. export controls. He said, “We should neither overestimate nor underestimate China’s technological capabilities. We need to assess them coldly and objectively.” Professor Kwon especially warned that Korea should not take the long-term potential of China’s semiconductor industry lightly. He said: “During periods of industrial transformation, technologies that once seemed unlikely to be used can suddenly emerge. That is what disruptive innovation is. China’s electric vehicles are a representative example. China chose EVs as a way to overcome the long-established ‘moat’ built by the U.S. and Japan in internal combustion engine vehicles, and as a result, it has developed world-class technological capabilities. There is no reason the same thing cannot happen in semiconductors. Across China, Huawei fabs and industry-academia cooperation centers are simultaneously developing EUV alternative light sources, optical systems, and PR, or photoresist, materials. If one of these technologies survives, China could quickly move onto a growth curve backed by its enormous domestic market. A crisis could emerge in which Chinese semiconductor equipment, materials, and technologies begin to have a global impact.” Professor Kwon was particularly concerned about the possibility of China developing next-generation lithography technology. “Today, everyone says that cutting-edge processes below 5nm are impossible without EUV. But precisely because of that, EUV, monopolized by the Dutch company ASML, is also an environment highly susceptible to disruptive innovation. China’s accelerator-based light source technology could become the next-generation technology after EUV. A prototype could emerge as early as the mid-2030s. If that happens, even if SMIC remains around ten years behind TSMC and Samsung Electronics, it could eventually enter the single-digit nanometer process regime, meaning advanced ultra-fine process technology.”

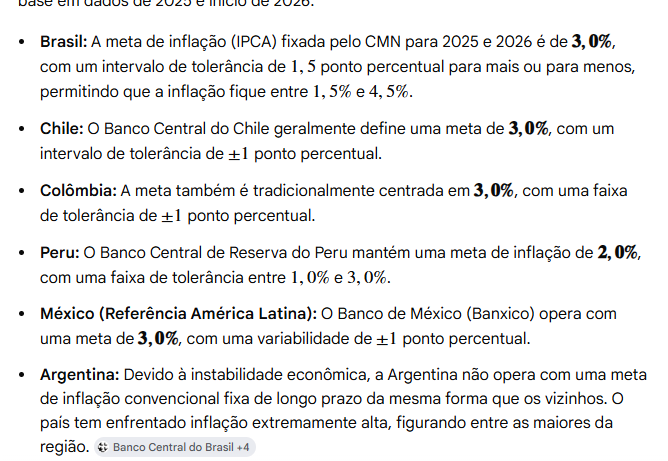

Muitos economistas e analistas do mercado financeiro brasileiro acreditam que mudar a meta de inflação abriria espaço para mais cortes da taxa Selic. Eles não entendem como a inflação funciona. As empresas atualizam seus preços/quantidades produzidas com base em uma expectativa de demanda futura + uma inflação média esperada, ancorada pela meta. No momento em que a meta é elevada, a inflação esperada sobe proporcionalmente e a inflação realizada converge para um nível mais elevado. Se o argumento é baseado na "credibilidade da meta", então não é necessariamente a mudança na meta maior que vai dar essa credibilidade, mas sim a capacidade do banco central de domar a demanda agregada. E essa demanda não tem nada a ver com a meta escolhida, ela é meramente uma combinação ótima entre estímulos fiscais e monetários. Quer saber mais então leia um post do meu antigo blog em português, abaixo.

The death of inbound applications is upon us: and yes, it’s in a big part because of AI making it dead simple to apply. And so inbound applications become noisy, with increasingly more of non-qualified people. And so companies rely on referrals and recruiters to source instead.

Claude Cowork can apply to 50 jobs in under 30 minutes. Here's how to set it up.

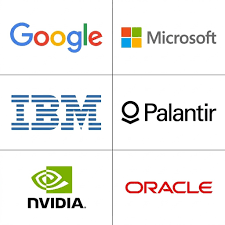

BREAKING: 🇮🇷 Iran is expanding the targets Iran published a hit list naming Google, Amazon, Microsoft, Nvidia, IBM, Oracle, and Palantir offices across Israel, Dubai, and Abu Dhabi as legitimate targets - CNN Billions of dollars of investments are going to be destroyed.

TRUMP MULLS A NORTH AMERICAN TRADE PACT WITHOUT CANADA - NYT

in a recession the continued progression of AI technology is deeply bearish but y’all ain’t ready for that conversation

NYC Mayor Zohran Mamdani: "We'll replace rugged individualism with collectivism"