client just advised me that while rolling over his wife's $500k 401k, he inadvertently clicked the wrong account and rolled it into a Roth.

didn't have that on my 4/14 bingo card...

This is damage from deer eating the leaves. The well-defined line is called the “browse line”. They can’t comfortably reach above that line.

You can see they ate the tender leaves and left the brown stems behind. This person should remove the lower branches completely and plant something deer proof underneath.

Person in Michigan is asking what happened to her arborvitae hedge. They looked perfect last year.

This will be obvious to anyone who has dealt with it before.

I’ll put the answer below.

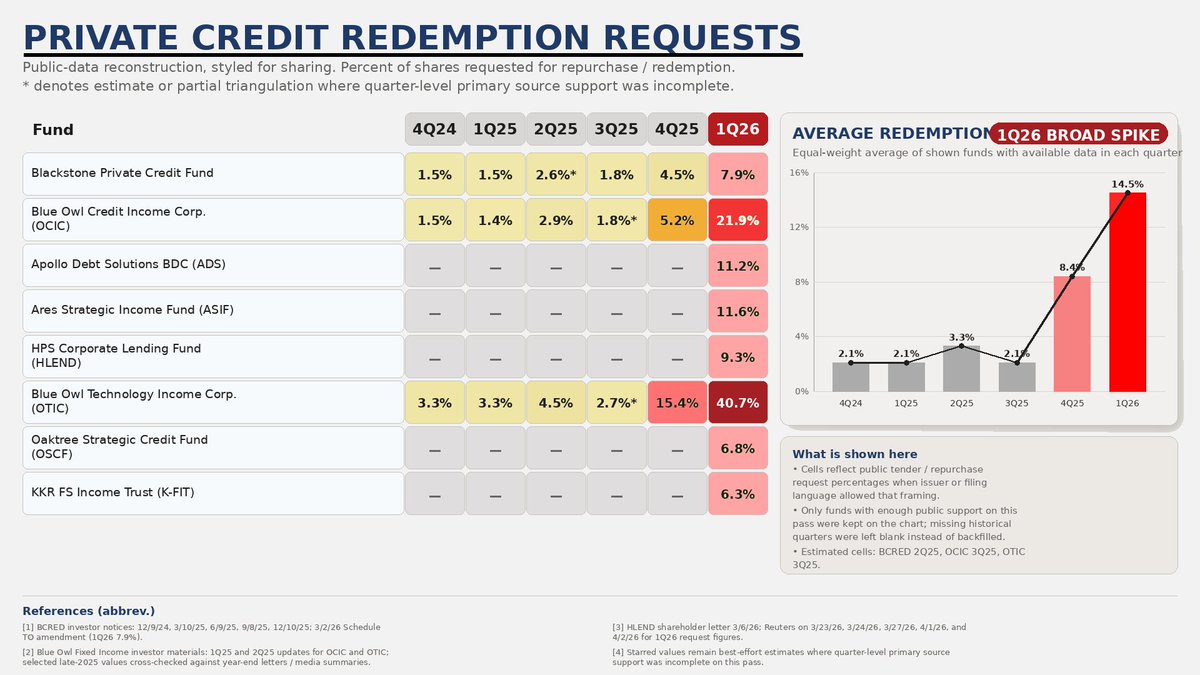

PRIVATE CREDIT FLASHING WARNINGS FOR STOCK MARKETS

I've been posting about this for months and its getting worse. Let me explain what investors and traders need to know here.

THE SHORT NOTE: If redemption requests keep accelerating in private credit, it will become a broader risk asset story for $SPY, $XLF, small caps, and the economy overall.

WHAT THIS CHART SHOWS: Redemption requests are rising across several large private credit funds. That matters because many of these vehicles effectively cap repurchases around 5% per quarter to avoid being forced sellers into illiquid markets. As you can see, what started as a Blue Owl $OWL issue in Q4 has now spread to 9 major groups exceeding 5% in Q1 of 2026. That's a rapid spread and its only the surface.

WHY THAT MATTERS: Private credit is sold as source of "durable yield steady income" that investors can rely on. Its boring but regarded as safe. The problem is that narrative can shift fast into a liquidity mismatch once too many investors want out at the same time.

LIQUIDITY MISMATCH: The issue is that these funds don’t own highly liquid assets. They own loans that are harder to price and harder to sell quickly. Think of it like panic selling a low float, low volume stock that has a wide bid to ask spread: If you keep smashing the bid or hitting sell at market, you take worse and worse prices. In private credit, forced selling into thin liquidity can pressure marks, confidence, and future redemption behavior.

SELF-REINFORCING RISK: This is where things start looking like a slow motion bank run (remember Silicon Valley Bank?). Investors see redemption requests rising, so they worry that they may get stuck behind gates or queues, and put in redemption requests or their own. Then other investors who may have been calm see the numbers rising and decide to sell as well - son on and so forth. That can make the next quarter’s demand even worse and feed into headlines discussing investors who can't get their capital out.

IMPACT ON STOCK MARKETS: This could weigh on $SPY, $XLF and $IWM by tightening financial conditions beneath the surface. Credit stress usually hits economically sensitive areas first, then bleeds into broader equity multiples as investors reprice growth, liquidity, and default risk.

BANKING FEARS / FINANCIALS: This is worth watching for $XLF but mostly credit sensitive financials. Even if private credit isn’t the same as the banking system, rising stress in lending markets can reignite fear around credit quality, funding, and who is truly holding the risk.

SMALL CAPS / DOMESTIC GROWTH: Smaller companies are especially exposed. If private lenders get more defensive, credit availability can shrink. That is a real issue for more financing-dependent parts of the market and could pressure cyclical stocks and parts of small-cap land.

MORTGAGE & LENDING: The bigger issue is not just housing, it is the broader cost and availability of credit. When lenders tighten, business formation slows, investment slows, refinancing gets harder, and economic momentum weakens.

WHY THE FED CARE: If private credit starts showing real cracks, it is another sign that monetary tightening is still working through the system. That may not show up immediately in headline data, but it can tighten conditions faster than many expect and force the Feds to make a move.

BOTTOM LINE: Private credit was supposed to be the “durable yield” boring but safe trade. If it starts turning into a liquidity story, markets will care as these groups manage a lot of US capital and once confidence in credit structures weakens, that rarely stays contained for long. We're already seeing those signs when comparing Q4 of 2025 to Q1 2026 - quick erosion of confidence and some early stage panic.

I’ve just seen this angle of the Arsenal penalty and I stand corrected, Madueke didn’t dive and it was a foul.

I hold my hands up 🙌

x.com/Mshari5350861/…

Next time somebody tells you somebody is a “No Brainer” NBA guy, remember that this dude was a top 10 recruit, doing all of this, went to Duke, and he’s not in the league

The 0.1% is different

You’re given $2m.

You have 20 minutes to spend it.

You can’t spend it on cars, airplanes, yacht or a house. You can’t spend it on golds or diamonds either.

What will you buy?

This is what we get when you don’t let players go straight to the NBA and force a 1 and done

A guy who can score a disinterested 32 in a Big 12 win with an angry fan base

This step in his journey is unnecessary and has been a s*** show - Still top 3

@ogpinions Very well done. I would add de bruynes goal in the first leg at Madrid. Maybe the most important goal in history of city. Hopefully we can add more at the end of the year!

@SteveOnSpeed Also escrow has to put on that monthly to own a home. Yes the mortgage is $2,684 but depending where you live add on another $500-$1000 a month.

A $500K home at 5% interest: 30-year mortgage = $2,684/mo & $466K interest total.

Stretch to 50 years = $2,271/mo but $862K interest.

Marginally lower monthly payment.

Almost double the interest.

Terrible plan.

Ok here’s more 📸 (I’ll be gradually flooding your timeline with these. Not sorry)

These may look plain or too simple to some. But the story and connection to every AJ17 makes these incredible.

Final US Open giveaway.

You get this duffle bag, my US open credentials, a pair of my Footjoy premier shoes that I’ll sign (worn during my titleist shoot)

Winner is first person to guess my locker number this week. 1-200

No cheating!

Some of you asked insiders to look my locker number up 😂

23 years ago a 22-year-old Rookie Mark Prior (in the red bill hat) sent prime Barry Bonds a message to back off his plate and then not backing down is what made Mark Prior different. #MarkPriorForever