Ernest

641 posts

Chronic trimming can be an issue.

Understandable to want to lock some in but if you’re constantly trimming off some of the position, at some point you’re going to have nothing left.

Big winners can’t be big winners if you trim the position down to nothing.

Let winners win.

English

GREAT FEEDBACK ON THIS POST;

I WILL BE DOING A TRADE BREAKDOWN LATER TODAY!

Tiger Line Trading@TigerLineTrades

GOOD MORNING TWITTER FAM; ☕️ COMMENT BELOW WHICH 3 STOCKS SHALL I DO A TRADE BREAKDOWN ON? *MOST MENTIONED WILL BE POSTED LATER TODAY

English

@aceddeca1 my wife certainly gets frustrated with my X addiction but is happy to see me deeply passionate about something which I hadn't had for a few years prior 😂😂🤝

English

When my X account was growing, I would answer EVERY comment I received without fail

I loved being reliable in that way. But as my account has scaled, it's become *impossible* to keep up with the volume.

Forgive me if this sounds egotistical but there is simply not enough Rould to go around 😂

So I apologize to anyone who used to get consistent responses from me. I will always try to answer as many as possible! But priority for thoughtful responses will of course go to subscribers.

I also have a lot of people with notifications on for my replies who don't need to bothered with me saying "thank you" or "yes" to simple questions. I aim to keep my signal high.

And I spend hours per day answering people now. I almost never scroll the For You feed because I spend almost all my X time responding to requests! But it's all good. I don't just love it, I am highly addicted to it 🤣

Thank you everyone again for the support 🤝 I am excited for the week ahead after a nice long weekend😎

English

@Jokillio Averaging ~80 replies per day which comes to something like one every 12-13 minutes while awake every day 😂😂😂

English

@WildBever 6/10 short term and much higher once revenue start pouring in

English

$INDI

+15% Friday.

2x volume.

Testing YTD / 8-month highs.

Please repost, bookmark, and consider subscribing for $1 to support the research.

The next $NXPI in plain sight chilling.

1B vs 79B

125$ 25x from here potential.

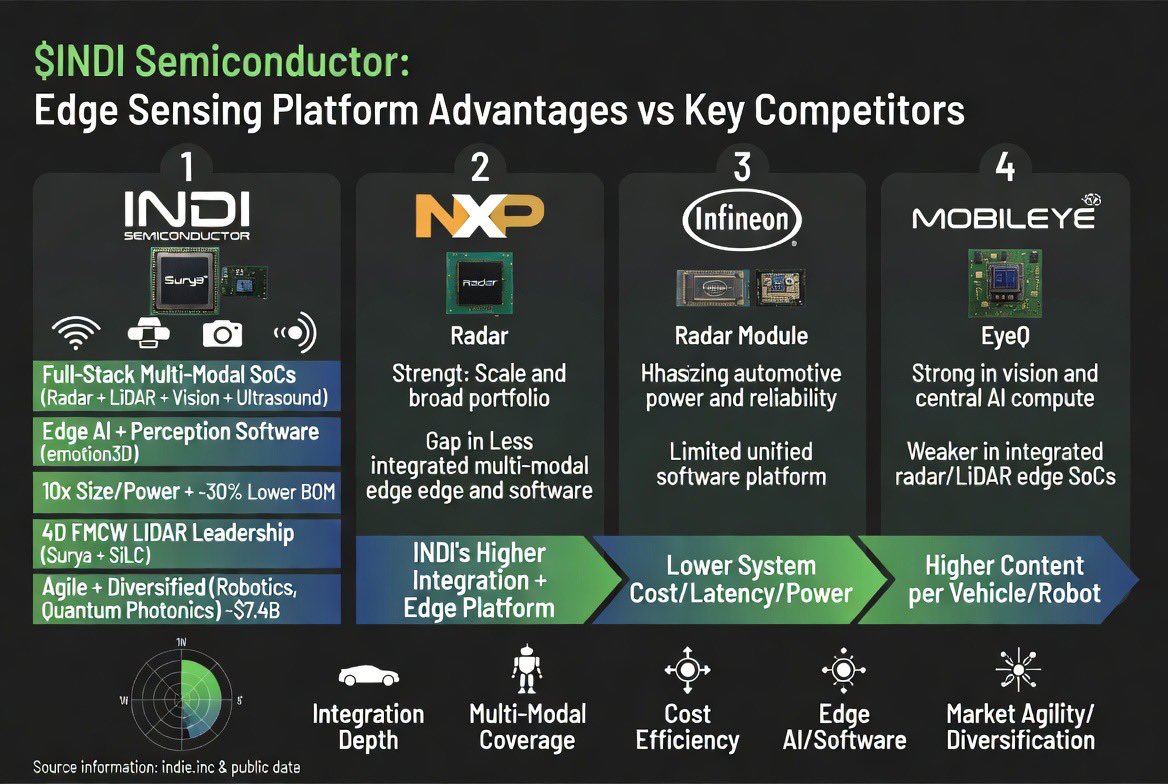

Most investors continue to evaluate automotive semiconductors through the traditional framework:

$MBLY $NXPI $ON $ADI $TXN

However, $INDI is targeting an entirely different layer:

The distributed AI sensing layer.

Radar.

LiDAR.

Vision.

Sensor fusion.

Edge AI processing.

Photonics.

And the underlying metrics are becoming increasingly difficult to overlook:

• Q1 2026 revenue: $55.5M

• Q2 guide: $59–65M

• TTM revenue: ~$217M

• Strategic backlog: ~$7.4B

• Backlog/revenue ratio: ~34x

• $25M Gen8 radar production order in Q1

• iND880 vision processor shipping in volume at NIO

• ams OSRAM CMOS sensor acquisition expected to close Q3

• 28% short interest

• 63.8M shares sold short

That backlog figure is what makes this setup particularly compelling.

A company with an approximate $1B valuation holding roughly $7.4B in strategic design-win backlog directly tied to the ADAS buildout cycle.

And that cycle is accelerating globally.

Europe has already implemented mandatory safety systems through GSR regulations.

The U.S. NHTSA AEB mandate arrives later this decade, meaning OEMs are designing hardware platforms today.

Every major OEM is moving toward:

• more radar

• more cameras

• more LiDAR

• more edge compute

• more sensor fusion

That trend significantly increases semiconductor content per vehicle.

This is where $INDI differentiates itself.

It has established exposure across:

• 77GHz radar

• 120GHz radar

• LiDAR SoCs

• vision processors

• ultrasound

• photonics

• perception software

The LiDAR segment in particular may be more important than many investors appreciate.

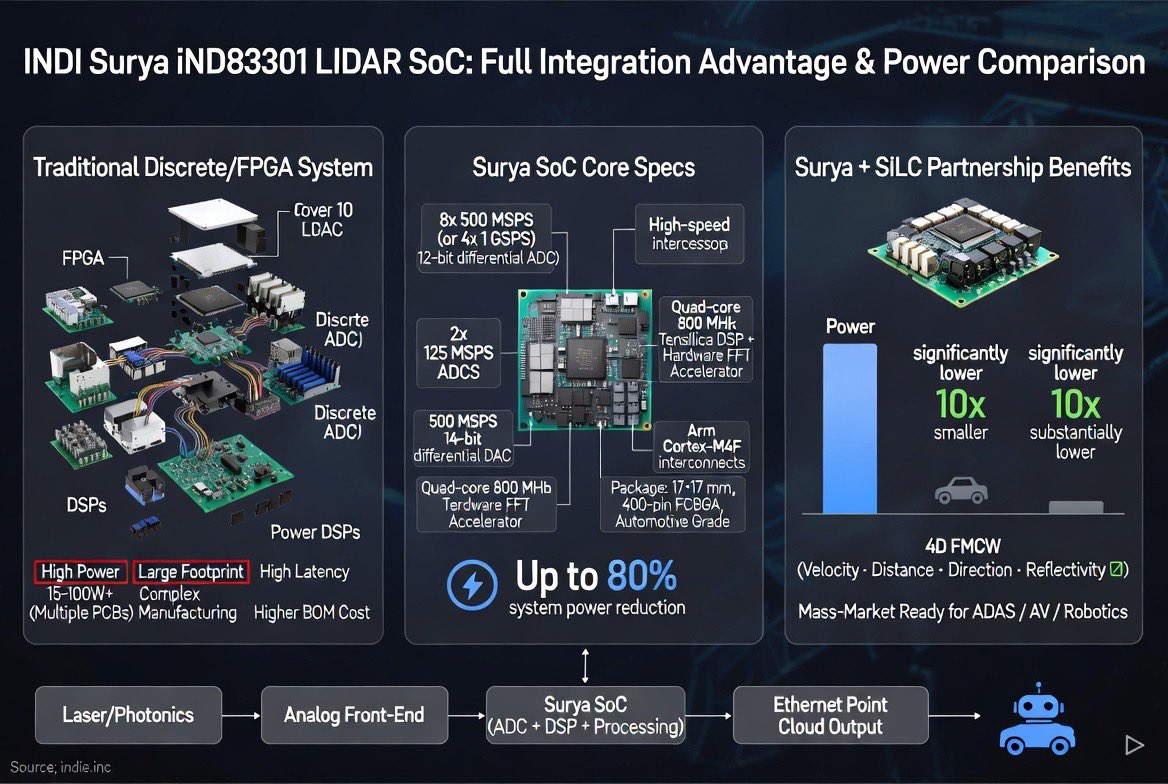

Its Surya LiDAR SoC was designed to replace bulky FPGA-heavy architectures with highly integrated edge processing.

The platform integrates:

high-speed ADCs,

DSP compute,

FFT acceleration,

and real-time signal processing directly at the sensor layer.

Smaller footprint.

Lower power consumption.

Lower latency.

Lower BOM cost.

That architecture is important because OEMs are seeking greater sensing capability without materially increasing vehicle cost or thermal load.

Even more notably:

$INDI is emphasizing FMCW LiDAR rather than traditional time-of-flight approaches.

FMCW enables:

• direct velocity measurement

• stronger weather performance

• interference resistance

• richer 4D sensing data

These capabilities become increasingly valuable for autonomy, robotics, and industrial perception systems.

Partnerships with SiLC and LightIC reportedly demonstrated:

• up to 10x improvements in performance/power/form factor/cost

• ~80% power reduction

• ~40% size reduction versus legacy FPGA systems

$INDI is not merely building chips.

The company is building distributed edge intelligence infrastructure.

Rather than pushing all processing into one centralized computer, OEMs increasingly prefer intelligence to be processed directly at the sensor edge:

lower latency

lower power

lower bandwidth

lower system cost

That is exactly where $INDI’s architecture is positioned.

The overlooked component here may ultimately be physical AI.

And $INDI quietly sits adjacent to all of these themes simultaneously.

Recent flow included:

$413K worth of Nov 7.5C call buying.

Aggressive ask-side positioning.

50% OTM.

On a stock with:

• 28% short interest

• high beta

• relatively small float

• Q2 earnings — early August

• potential guide raise

• further radar ramp conversion

• NIO scaling

• ams OSRAM close in Q3

• Q3 earnings in November

At present, the market still largely values $INDI as:

“another small unprofitable auto semi.”

That represents a materially different valuation framework.

Industry names:

$MBLY $NXPI $ON $ADI $ALGM $TXN $AEVA $LAZR $INVZ $NVDA $TSLA $SIVE $LITE $POET $LIDR $OUST $AMD $MU

English

@jrouldz @Garrett_Watton Insightful and I was wondering where this company was possibly going. 1000 shares, not sure if it's worth holding at 10 bucks?

English

been tracking $MBLY for a while

lots of hype and potential and right market at right time and all that. really formidable competition in form of $TSLA and Waymo etc so that turns me off fundamentally. Not players I'd want to be competing against

technical: formed bottom and broke downtrend

but I am worried about horizontal line flipping from support to resistance. This gets interesting again if it can reclaim $11 but more importantly they will have to prove sustainable demand

English

Fair warning to anyone chasing the $QBTS pump this morning:

I will be using you as exit liquidity 😆

English

@WildBever @steady_profits Yes no problem! Have a great day bro

English

$HIMX

THE BREAKOUT MAY HAVE JUST STARTED

20$ taps overnight.

Himax Technologies makes display drivers, automotive semis, AI sensing chips, and optical components powering next-gen AR + AI infrastructure.

The market just re-rated it in a single week from “forgotten display IC company” to “AI optics + CPO infrastructure play.”

But moves like ~+45% in a week don’t eliminate risk — they compress it into sharper momentum and faster repricing.

Watching closely.

Himax just went through a major structural breakout:

~+30% Day 1 after earnings

~+11% follow-through Day 2

highest weekly close ever

broke a ~5-year base

potentially breaking a structure that has existed since IPO

This is no longer just “good earnings.”

It’s price discovery after a decade-long compression structure.

The core technology moat (what actually matters long term)

Most investors still think $HIMX is just a display driver company.

That’s outdated.

The real story is monolithic wafer-level optics (WLO) for Co-Packaged Optics (CPO) infrastructure.

Why this matters:

Traditional optical systems use discrete components:

separate microlens arrays

separate prisms

separate fiber alignment structures

all assembled individually

That works for older pluggable optics.

But AI infrastructure is entering a completely different scaling regime.

Future AI GPUs and switches require:

extreme thermal precision

sub-micron alignment tolerances

massive optical bandwidth

semiconductor-scale manufacturing volume

Discrete assembly becomes the bottleneck.

This is where Himax becomes interesting.

$HIMX uses nanoimprint lithography to manufacture monolithic optical structures directly at wafer scale:

microlens arrays

integrated prisms

fiber alignment grooves

all built simultaneously into a single structure.

No multi-piece stacking.

No compounded alignment drift.

No slow discrete assembly scaling problem.

Himax didn’t build this process for AI originally.

That forced them to master:

sub-micron wafer uniformity

high-yield monolithic optics

mass-scale production economics

Now AI infrastructure suddenly needs the exact same capabilities.

That’s where the asymmetry appears.

The CPO positioning (this is the key)

$HIMX is currently the exclusive wafer-level optics supplier to FOCI for TSMC’s COUPE optical engine platform.

Management commentary:

Gen 1 validated

initial shipments expected H2 2026

Gen 2 already in customer validation

“meaningful” revenue contribution expected 2027+

The revenue potential starts getting large fast:

2027 potential → ~$80–100M

2028 potential → ~$250M+

2030 potential → potentially $600–800M+

Current HIMX annual revenue is only around ~$800M total.

Meaning CPO alone could eventually rival the size of the existing company.

And likely at materially higher margins.

The valuation disconnect

$HIMX still trades closer to a legacy semiconductor multiple despite now having real AI optical infrastructure exposure.

~9–10x EV/GP while AI optics peers and photonics infrastructure names trade materially higher.

The market is still debating whether this is:

“legacy display business with temporary hype”

or

“early-stage AI optical infrastructure supplier.”

That distinction matters.

Because if the market fully accepts the second narrative, valuation frameworks change completely.

Phase shift

Early → ignored legacy semi

Mid → earnings validation + breakout

Late → AI optics / CPO repricing cycle

$HIMX now appears to be transitioning from validation into institutional price discovery.

The risk is execution.

The opportunity is that the market may still be massively underestimating how important monolithic optics become as AI interconnect scaling accelerates.

$POET $AAOI $LWLG $MRAM $QUIK $GSIT $MU $SNDK $NVDA $DRAM $AMD $GOOGL $HIMS $VOO $AVGO

AI infrastructure is no longer just GPUs.

The bottleneck is moving into optics.

English