可言

1.9K posts

FAの技術を「魅せる」ことに使った展示は圧巻でした!さすが世界の安川電機!

✅中国EV新興勢の「R&D投資効率の壁」が浮き彫りに 零跑汽車(Leapmotor/リープモーター)の朱江明会長 「最も経済的な方法を使っても、新型モデルの開発には「最低10億元(約200億円)」の投資が必要」 NIOの李斌会長は 「新型車の開発費用は10億元だったが、その寿命は6ヶ月未満だった」と述べています。 しかも深刻なのは量の問題も加わり 「年間1万台の生産能力を計画していても、実際に生産・販売が5,000台にとどまり、工場が半分空いたまま、2交代制から1交代制に縮小され、研究開発費+生産能力コストが1台あたりに分散され、極めて高額になってしまう」 まさに、R&D版ICOR(限界資本産出比率)の悪化そのものとなっています。 追加の巨額投資(ΔK)に対して、売上増加(ΔY)が追いつかない。 技術難易度が非線形に跳ね上がり(L2→L3自動運転、SDV、車載半導体内製化など)中で、規模の経済が効きにくい新興勢は固定費回収のジレンマに苦しんでいます。 Leapmotor自身は2025年に新興メーカー販売台数トップクラス(約60万台)と急成長中ですが、それでも会長が自らこのリスクを公言している点が象徴的と言えます。

BYD 2026年Q1決算から読み解く 「大きすぎて倒れない」から「大きすぎて立て直せない」へ 2026年Q1決算が示す構造的転換点 ※長文になります

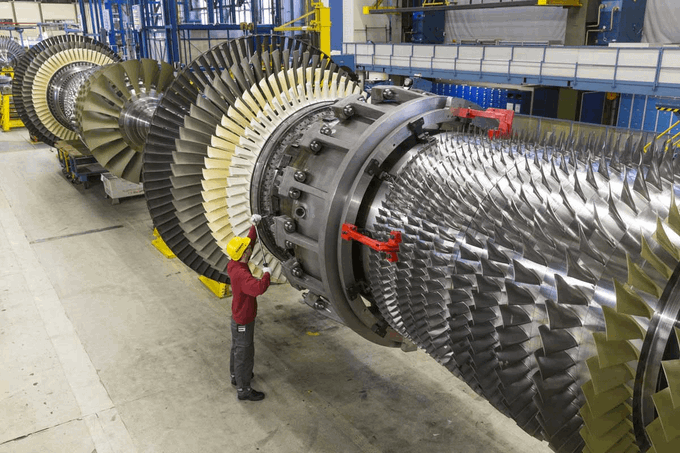

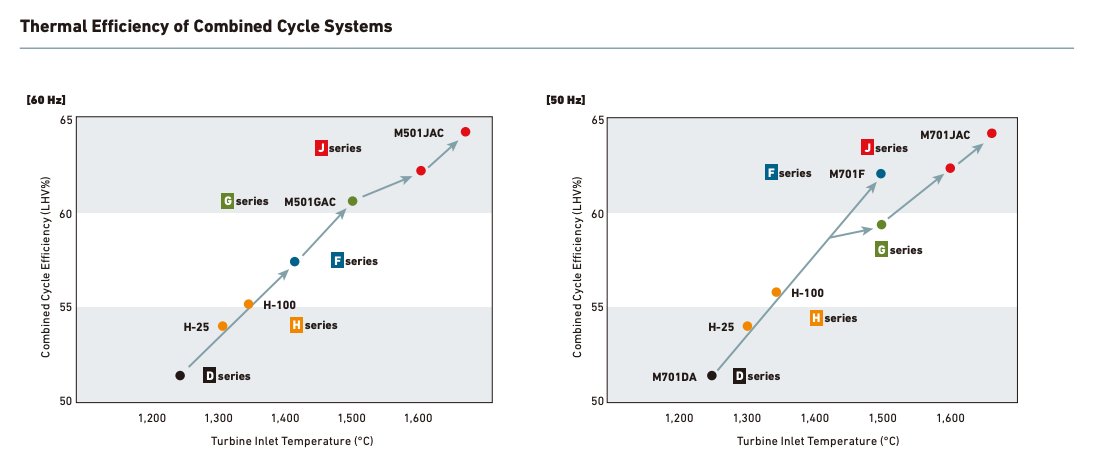

You cannot buy a new gas turbine until 2030. Order books at GE, Siemens, and Mitsubishi stretch to 2029. Turbine prices have nearly tripled since 2019. Every AI data center needs power and every gas plant needs a turbine. And every turbine has one part that bottlenecks the entire industry: The blade. It has to survive in gas 500°C above the melting point of the metal it's made from and spin at up to 20,000 RPM under 10,000 g of centrifugal force. Each blade is grown as a single crystal of nickel superalloy, pulled through a vacuum furnace at 3 mm per minute. A set of blades costs $600,000 and takes 90 weeks to grow. The same metallurgy powers modern jet engines. Only 3 companies on Earth can build one. China spent $42 billion trying to catch up. They bought a Russian fighter engine, took it apart, and copied every part. Their copy ran 30 hours between overhauls versus 400 for the original. Modern Western engines run 4,000. You can reverse engineer the shape of a turbine blade. You cannot reverse engineer 60 years of metallurgy.

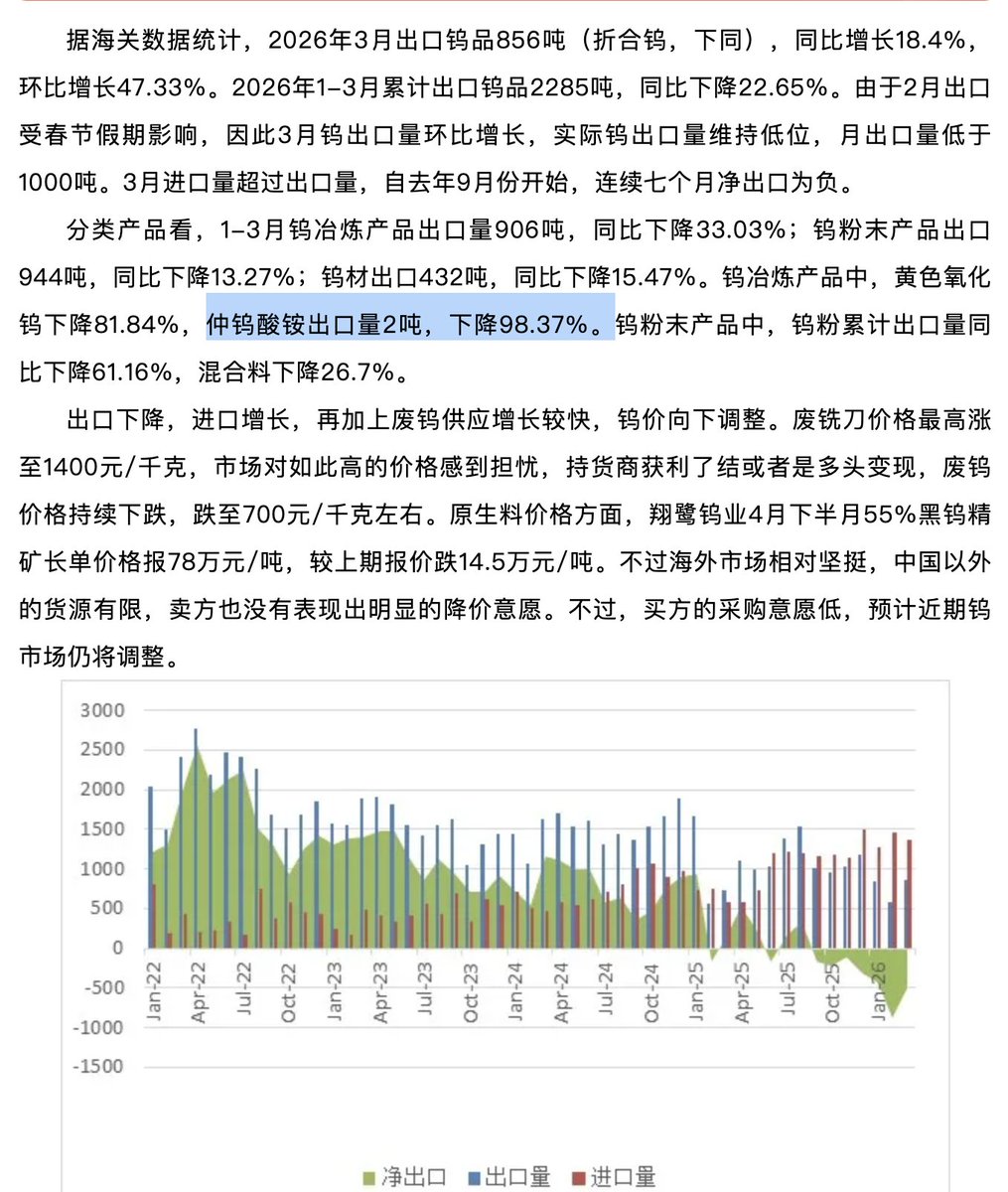

China’s tightening grip on tungsten is reshaping the global market. Ammonium paratungstate (APT), the key intermediate used in tungsten production, has surged more than 200% year-to-date, crossing $3,000 per metric ton in Rotterdam as supply conditions tighten across the value chain. The drivers: ▪️China, which accounts for the majority of global tungsten output, has restricted 2026–2027 exports to 15 authorized firms and tightened controls on certain dual-use materials. ▪️Defence demand is rising ~8% annually, with tungsten used in aerospace and military applications. Outside China, supply remains thin. The US currently has no active tungsten mines, increasing reliance on foreign supply chains. In South Korea, Almonty’s Sangdong mine began production in March — one of the most significant new non-China sources in recent years. #Tungsten #Mining #CriticalMinerals #SupplyChain mining.com/web/tungsten-b…