Hello readers. Thanks for joining me on this X stream. I appreciate the follow by you and as time allows I will follow back.

This X stream will be devoted to my faith in Jesus Christ and my objection to a world going wrong with my hometown of Minneapolis where we still have properties as part of our summer stay.

Question.

Are there any traders who followed me and are reading this. Please reply. I posted a three part history of my trading over on the PeterLBrandt stream and may continue it here.

The PLB X stream will be repurposed later in the 2nd quarter to more pure trading research. I will again post charts there starting again next week.

DUMMIES GUIDE TO BEING QUANTUM SAFE.

In the past it was about protecting your PRIVATE KEY (your seed phrase). In the age of big scary quantum computers (BSQC) that are coming, you need to protect your PUBLIC KEY also.

Basically a BSQC can figure out your private key from a public key.

The present day taproot addresses (the latest format) are NOT safe, these are addresses starting with "bc1p" and they embed the public key into the address, not good.

Prior formats hide the public key behind a hash, so a BSQC can't easily crack it.

Do this:

1) create a new segwit wallet. It will start with "bc1q" (NOT "bc1p"), you can use older formats too like ones starting with "1" and "3"

2) send all your BTC into this new address

3) you can continue to stack sats into this new address

4) NEVER send BTC out of it, once you do you're BSQC hackable because your public key is revealed

5) wait for Bitcoin to upgrade to a quantum safe protocol, this may take 7 years, who knows

6) send your BTC into the new quantum safe address when the network is NOT congested, once you send, you reveal the private key for a short time. It's unlikely a BSQC will steal your coins in that short window

2025, day 149

Good morning from Asia.

In trade, Trump’s tariffs were declared illegal by a panel of three judges at the US Court of International Trade - which can be appealed to a federal court;

Brussels is asking EU firms how exposed they are to U.S. investments - a hint of a possible use of their nuclear trade anti-coercion instrument(?); as

Those hoping for an EU-U.S. trade deal are “dreaming” (Politico) because “European politicians have no appetite to give the White House big concessions and revisit the inflammatory topics that dominated the TTIP talks a decade ago.”; and

The U.S. told software makers in the semiconductor industry to stop selling to China - once again showing this 90-day tariff pause is not a peace but a ceasefire to rearm;

In geopolitics, President Putin’s reported peace demands are: a "written" pledge not to expand NATO east; Ukraine to be neutral; some sanctions lifted; a resolution of frozen Russian FX reserves; and protection for Russian speakers in Ukraine - presumably on top of keeping the territory he’s taken. Will Ukraine and the EU agree, because presumably the U.S. will(?); as

Brussels plans to upgrade Black Sea infrastructure to handle military equipment as Germany will produce long-range weapons with Ukraine allowing it to strike deep inside Russia & give it another €5bn in military aid. So, EU escalation… with no clear plan to deescalate(?);

Prague accused China of hacking & the EU slammed Beijing for a “malicious cyber campaign”; and

The U.S. is concerned Israel may strike Iran with mere hours warning, as the two negotiating sides could issue an interim declaration of principles soon;

Israel announced it has a functioning anti-drone system based on lasers - a world first that changes warfare - does that still mean Canada has to pay $61bn for a U.S. Golden Dome?; and

Hamas said it agreed to a framework for a permanent Gaza ceasefire;

In politics, Elon Musk has left President Donald Trump's administration, the AP reported;

Foreign students wanting to study in the U.S. may need social media vetting to get a visa; as Secretary of State Rubio will deny them for foreigners who are "complicit in censoring Americans….the days of passive treatment for those who work to undermine the rights of Americans are over.”;

Portugal’s far right Chega party came second in its election when all the votes were counted, shattering decades of political norms; and

Greece shut down the agency at the center of a probe into a massive EU farm fraud involving it;

In markets, ECB President Lagarde discussed leaving her job early to run Davos by 2027 at the latest says Klaus Schwab, who’s under investigation for impropriety: Lagarde was found guilty of negligence in 2016;

OPEC+ is expected to approve a further increase in oil production for July at its meetings this week, according to delegates, says Reuters; and

U.S. VP Vance publicly backed Bitcoin and crypto.

Any one of these stories would be a huge headline alone. Today, they are just part of the 2025 cocktail.

I have some good news and [maybe] some bad news for you.

GOOD NEWS: Risk SIgnal is trending downwards, meaning over the broader environment buy-side liquidity is dominating. We are setting up for another solid run on the long time frame.

Re the U.S. debt downgrade, you should know that credit ratings understate credit risks because they only rate the risk of the government not paying its debt. They don't include the greater risk that the countries in debt will print money to pay their debts thus causing holders of the bonds to suffer losses from the decreased value of the money they're getting (rather than from the decreased quantity of money they're getting). Said differently, for those who care about the value of their money, the risks for U.S. government debt are greater than the rating agencies are conveying.

#principles#howcountriesgobroke#debt

2025, day 129

Good morning from Asia.

White smoke! We have a new *American* Pope, the first, Leo XIV; and

A first U.S. trade deal, with the U.K. Those who like FTAs say it isn’t 3,000-pages and legally binding. Those who understand geopolitics know Tehran, Yalta, and Potsdam weren’t long on technocrats either;

The U.S. gets lower tariffs and can push special interests like beef and ethanol, and the U.K. will buy $10bn of Boeing jets. The U.K. is still going to face 10% on most exports - for the closest U.S. ally; a 100,000 car quota at 10% not 25%; and steel & aluminium (& pharma?) & engines for (fighter) jets **tariff free**. The latter shows the U.K. in the U.S. bloc for national security supply chains; and

No mention of China, but this was called “an economic security blanket” - whom else does that cover? Indeed, the Telegraph says “Starmer hands Trump ‘veto’ on Chinese investment in UK” - as a start;

Again, critics wanted more, as if this were still the Rules-Based Order. It isn’t. This deal undermines the WTO. Which is the point - and it was agreed by a U.K. government committed to the old global system because it couldn’t see anything better. The template is now there for others to follow; as

PIMCO warns Trump is really serious about keeping really serious tariffs for those who won’t play his new ball game; but

Things aren’t going so well on talks with China, as those who understand the protocols point out; and

The ‘EU takes aim at U.S. planes, autos in €100bn counterstrike against Trump tariffs’ (Politico), as “Brussels moves ahead with its retaliation, conceding its transatlantic ties with Washington may be beyond repair.” Clearly the EU aren’t going to do the same U.S. deal as the U.K., which leaves the two further apart and Europe with no bloc or with China - who are as close to Russia as possible; as

Ukraine is starting to consider a shift away from the US dollar, possibly linking its currency more closely to the euro amid the splintering of global trade and its growing ties to Europe, its Central Bank Governor told Reuters; and

While Europe is considering banning Russian energy, which would leave it reliant on the U.S. it is heading for a tread war with, Reuters claims the U.S. wants to help Russian gas get back into it again(!);

Meanwhile, after the U.K., over to you, Canada, Australia, New Zealand, Japan, South Korea, and India…; as

Pakistan sent swarms of suicide drones against India last night, to which India responded with reported strikes on air defences in Lahore, Pindi, and Karachi. The situation there continues to escalate; yet

The US no longer demands Saudi peace with Israel as a condition for advancing civil nuclear cooperation with it; and

The U.S. Ambassador to Israel says it “isn’t required to get permission from Israel” to cut a deal with the Houthis, and will only respond to them attacking it if Americans are hurt; so

Expect a new Iran deal soon(?) Aside from the Israelis, not everyone is happy about that - the Telegraph claims Iran’s IRGC was behind a recently-thwarted plot to bomb Israel’s embassy in London in order to derail nuclear talks.

And President Trump is back to telling people to buy stocks again.

Habemas a good day and weekend.

BREAKING: US 10Y rises to 4.48%, the largest single weekly increase since 2001.

U.S. 30-year treasury yields rise to 4.95%, weekly increase is biggest since 1982.

The EU is about to kill GDPR as we know it.

After 7 years of:

• Crushing European innovation & startups

• Making American tech giants even stronger

Brussels finally admits it: GDPR was an economic disaster.

Here's why this rollback could save Europe's dying tech scene 🧵:

2025, day 86

Good morning from Asia.

Russia says it won’t allow a Black Sea ceasefire until sanctions are lifted. The EU says it won’t lift sanctions until all Russian troops leave Ukraine;

The EU Readiness 2030 defence fiscal plan gets shot down by Southern Europe, which wants Eurobonds to pay for it, not higher national debt, which they don’t think they can afford; as

Rheinmetall is pressing ahead with a production line for parts for F-35s, despite recent headlines about not buying U.S. defence goods;

The EU calls for households to stockpile 72 hours of food and water amid war risks(!) Which, worryingly, is how long Poland admits its ammo stockpiles would last for in a war. x.com/kownackibartos…;

The U.K. saw more austerity and aid cuts to pay for 2.7% of GDP on defence spending by 2027;

Anti-Hamas protests in Gaza are popping up for the first time;

We will get 25% U.S. auto tariffs from Tuesday, even within the USMCA, as President Trump proposes the tax deductibility of interest on loans to buy U.S.-made cars. USMCA auto parts will NOT be tariffed, so Canada and Mexico could keep the lower value-added parts of that supply chain;

25% tariffs on copper are also being seen as imminent; lumber is being looked at; and chips and pharma have previously been floated as next but won’t happen immediately;

President Trump added on reciprocal tariffs, “We’re going to make it all countries, and we’re going to make it very lenient. I think people are going to be very surprised. It’ll be, in many cases, less than the tariff that they’ve been charging us for decades…. We have not been treated nicely by other countries, but we’re going to be nice. So I think people will be pleasantly surprised.” Vietnam and India are lowering tariffs anyway;

He also dangled the prospect of lowering tariffs on China if it does a deal over TikTok;

Markets are unhappy, to put it mildly; and

After some claim the pyramids are built on top of giant columns(?!), others say the CIA may have found the Ark of the Covenant back in 1988. Where’s Indy when you need him?

2025, day 84

Good morning from Asia.

A day after President Trump was pumping his own meme coin and it doesn’t even get a financial market headline…;

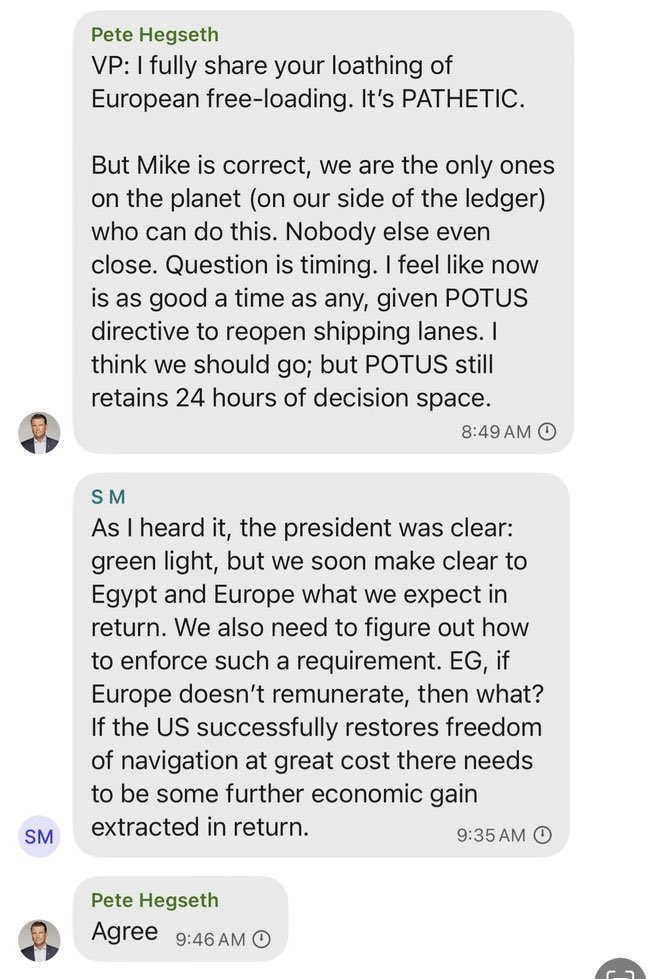

…we get a security breach —or, some posit, a deliberate plant— over Signal where, of all people, anti-Trump journalist Goldberg from The Atlantic is added to a group discussing attacks on the Houthis;

Not noticed in some of the furore is the U.S. Vice President not being interested in reopening the Red Sea to trade as only 3% of U.S. cargo goes that route vs 40% of Europe’s; and

The Defence (soon, War?) Secretary agreeing Europe are “freeloaders” and “pathetic”, and will be paying for the current U.S. operation to take out the Houthis one way or another. Last week I flagged in ‘In Deepest Ship’ that the next logical statecraft move for the U.S. was for the Navy to be made “pay to play” for those who don’t pay taxes for it;

Meanwhile, the USTR hearings on proposed port fees seen as a “trade apocalypse” proceed, and the U.S. appoints a new Secretary of the Navy promising radical changes;

That’s as discussion continues about rumours the Fed might not make swap lines available to the ECB. Some say that’s ‘the end of the dollar’; @josephwang points out it would mean Europe would have to hold much higher levels of $ FX reserves, like an emerging market. So, DM = EM. Or everyone can default on all dollar debt. And find their own aircraft carriers;

That’s as Germany confirms its F-35 procurement plans, and emphasises transatlantic cooperation;

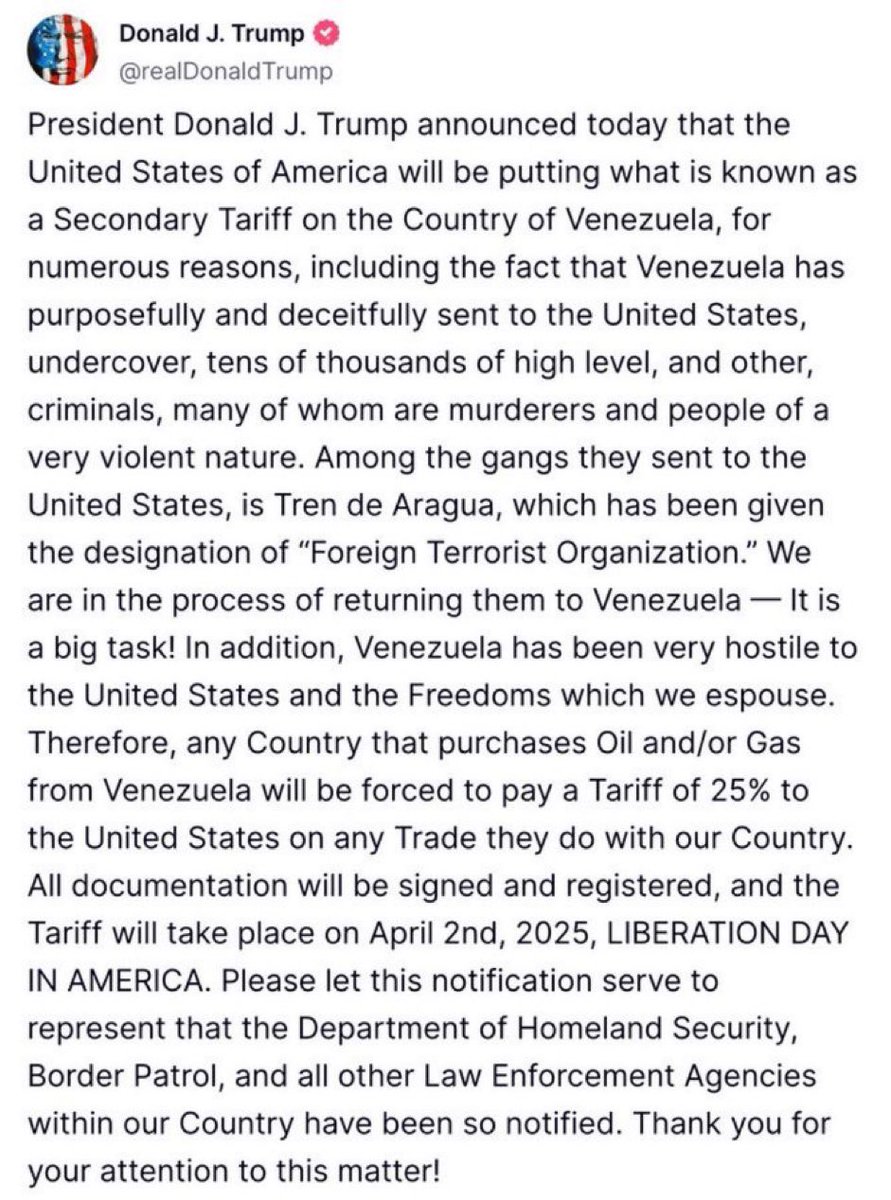

Just after finishing a conversation where it was agreed the U.S. would be focusing on Venezuela imminently, President Trump announced 25% tariffs on anyone who buys their oil. Welcome again to the Monroe Doctrine; and

Trump says U.S. auto tariffs are coming in days; as the WSJ says trade wars are exploding like in the 1930s; and

China explores a services subsidy and shuffles slowly towards consumer stimulus… despite its policy framework assuming exports will grow much faster than GDP, so increasing its already vast trade surplus; yet

The FT editorial board says U.S. tariffs won’t work…. Unlike Biden subsidies, when a tariff and a subsidy work in similar statecraft ways. The FT ignores that most of the countries now exporting so much to the U.S. used subsidies and tariffs to achieve that end, but hey ho. And still no critique of the Mar-a-Lago Accord.

So, another “quiet news day”.

2025, day 83

Good morning from Asia.

Trump family members plan a trip to Greenland, and some Danes call for them to be barred, as VP Vance says, “Denmark, which controls Greenland, is not doing its job, it’s not being a good ally. If that means that we need to take more territorial interests in Greenland, that is what President Trump is going to do. Because he doesn’t care about what the European scream at us.”;

Underlining how talk is cheap and fast rearmament isn’t, Sweden —one of Europe’s more credible military forces— sees its planned timeline for two new submarines, which had already incurred a five year delay, now sees 2028 delivery slip to “later than 2031”;

China is floating itself as a Ukraine peacekeeper, which could force Europe into some uncomfortable choices;

The U.S. insists on a full Iranian dismantlement of its nuclear program, not just scaling back of uranium enrichment; as reports have Iran militarising the Strait of Hormuz - a gun-to-own-head threat that could disrupt global energy markets hugely, via higher insurance premiums even before any firing starts; as Iran and Russia cooperate on producing electronics;

Turkey, in political turmoil after the arrest of an opposition presidential candidate, has banned short selling of stocks;

Israeli PM Netanyahu, also facing a constitutional crisis and street protests, huddles with defence ministry officials over Turkey’s expanding military footprint in Syria and aid to the new Islamist government. Local media reports a source saying direct Israeli-Turkish “friction” in Syria is unavoidable;

The FT notices “ships are the new chips”, as Bloomberg warns of a “trade apocalypse”, given the USTR holds public sessions today over proposed port fees for Chinese-built and operated ships in fleets of those who make calls in the U.S., and on export quotas for U.S. exports on U.S.-flagged, crewed, and —soon— built ships. (See this for more: media.rabobank.com/m/335caadb6132…);

The FT worries the U.S. is losing its “exceptionalism”, as stocks and the dollar fall in tandem. Have they seen what some big EM are doing?; and

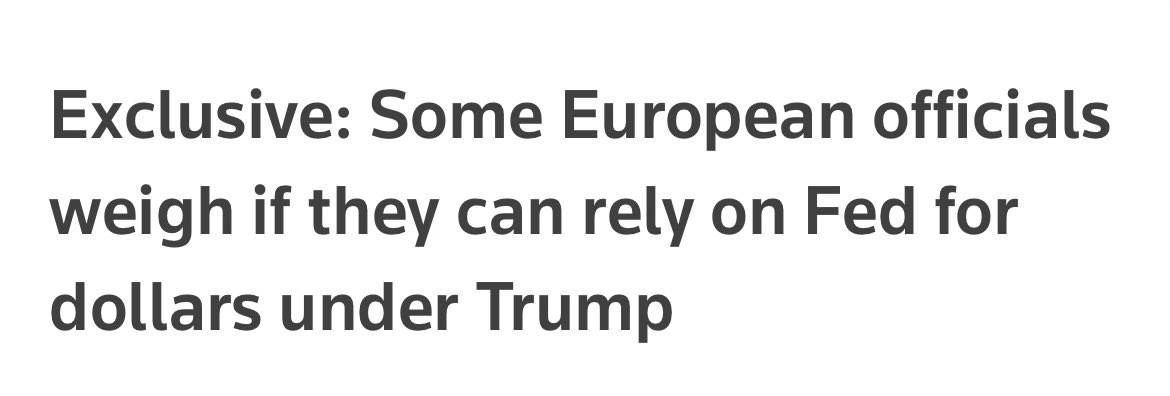

Some European central bank officials reportedly worry they can no longer rely on Fed swap lines in a crisis. Or rather, they can probably no longer rely on *apolitical* swap lines. There will be a quid pro quo for the dollars pro quids & euros; as

“Don’t fight the Treasury” is the new mantra for some. You mean there might be a correlation between a U.S. admin embracing radical economic statecraft and the key market pivot point they openly say they are now focused on? 😱

2025, day 82

Good morning from Asia.

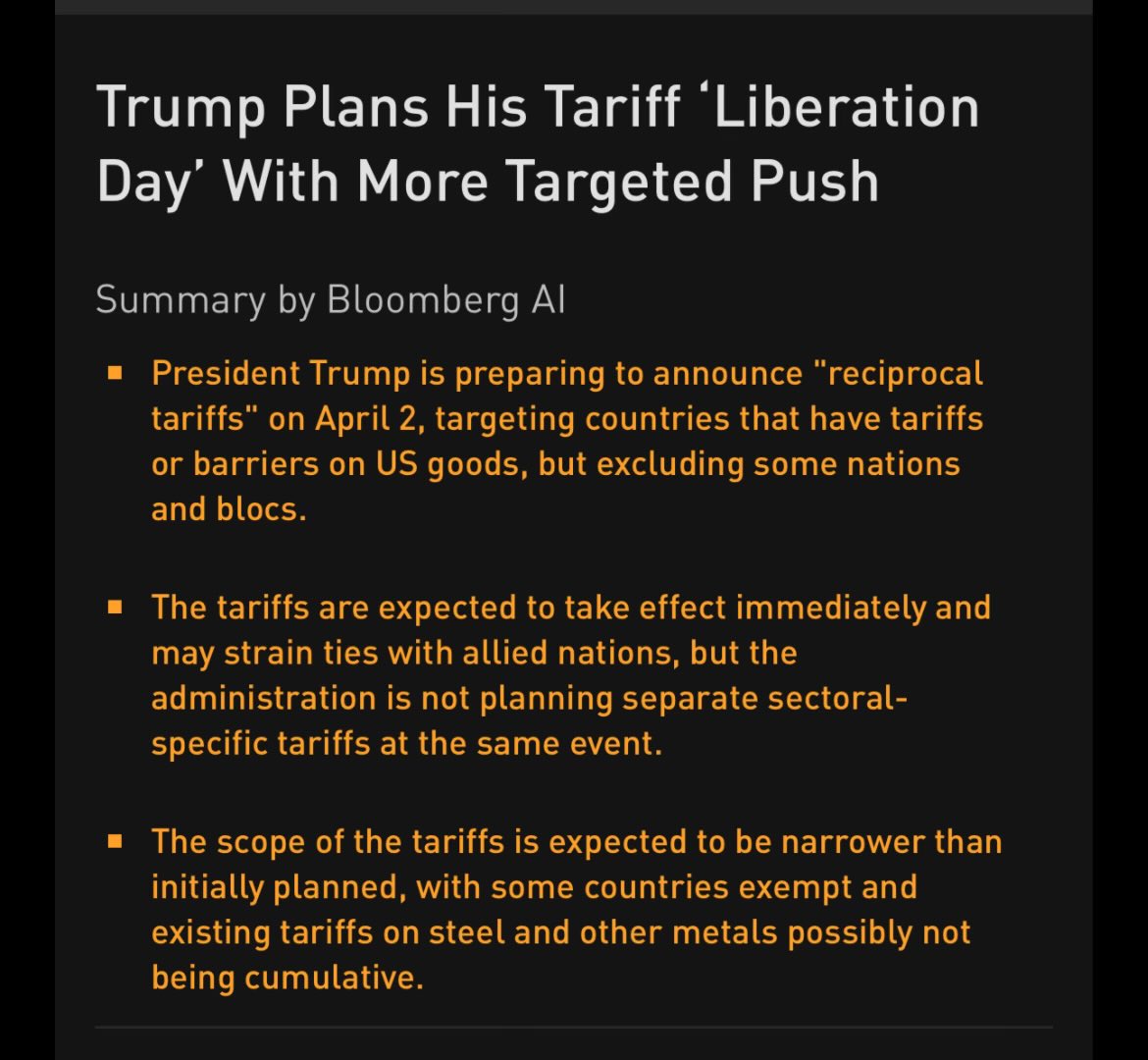

More Trump tariff rumours from

Bloomberg just over a week out from April 2 “Liberation Day”. It seems sectoral and reciprocal won’t stack, and as already stated, reciprocal won’t be high for everyone - just those running large bilateral U.S. trade surpluses, where the market impact will be largest. But it’s all still very fluid;

A report on the U.K. says everyone will be worse off by 2030, as the government now plans huge spending cuts to try to balance the budget as growth stalls again; as

PM Starmer prepares another attempt to get a Coalition of the Willing together in Ukraine; and

A former speech-writer for Japanese PM Abe floats his country buying one of the U.K. aircraft carriers they can’t afford to keep at sea;

China says it’s prepared for “external impacts that may exceed expectations” and will open up more sectors of the economy to international investors; as it also reveals a new deep sea cable cutting device that could threaten global communications;

Australia’s PM calls an emergency meeting after the U.S. cuts $100m of funding for… Australian universities; and

There’s weekend rumination over recent market turbulence in Turkey and Indonesia, and a sell-off in Indian markets.