Sabitlenmiş Tweet

80HD

1.3K posts

80HD retweetledi

English

80HD retweetledi

80HD retweetledi

Sure nice to see that somebody changed the name on the .gov Bank registration site. 😳

ffiec.gov/npw/

DirtΞvader@EvaderDirt

🤔 $BBBY "The RSSD ID is a unique identifier assigned to financial institutions by the Federal Reserve" Bed Bath & Beyond RSSD ID #4664848 ffiec.gov/npw/

English

80HD retweetledi

🦋Honey, I Found the Bear Trap🦋

Source: 8-K (dated Sept. 21, 2023), Ex. 99.1 (dated Sept. 29, 2023) — 20230930-DK-Butterfly-1, Inc. (f/k/a Bed Bath & Beyond Inc.), SEC Commission File No. 0-20214.

And just like that, there it is. The Bear Trap has been hiding in plain sight since September 29, 2023, not in Pacer or Kroll, but in an SEC filing!

It's been buried at the bottom of Exhibit 99.1, the Notice of Entry of Confirmation Order and Effective Date, this entire time. 😂🍿

Source Link

sec.gov/ix?doc=/Archiv…

1. Click the link above.

2. Scroll to the bottom of the page. Select Exhibit 99.1.

3. Scroll to the bottom of Exhibit 99.1. For reference, here it is again one more time:

Disclosure: This post is amateur dd for informational purposes only and should not be construed as legal, financial, or investment advice.

TLDR: The official notice confirming the BBBY Chapter 11 Plan contains a SINGLE SENTENCE on page 3 that explicitly declares legacy equity holders are PERMANENTLY BOUND to the Plan and its provisions, INCLUDING THEIR SUCCESSORS AND ASSIGNS, REGARDLESS of whether their Interest was impaired and REGARDLESS of whether they voted. You don't bind parties to a Plan that has nothing left for them.

Here we have Cole Schotz and Kirkland & Ellis confirming in writing, signed and dated September 29, 2023, the Effective Date of the plan, that the Plan still contemplates and perhaps anticipates a future legal relationship with legacy equity. 🎇

So let's set the stage.

I’ve spent a lot of time now tracking the security infrastructure. The CUSIP root. The GLEIF data. The Bloomberg FIGI records. The CIK and SIC code change. The potential meaning behind the FKA designation earlier this week. All of it pointing to the same conclusion below:

Legacy Bed Bath & Beyond Inc. survived in reorganized form as 20230930-DK-Butterfly-1, Inc., and the plumbing of global finance still treats it as a living corporate issuer.

But there's always been this one nagging question people have been throwing at us literally for years now: "Even if the shell is alive, so what? The Plan canceled equity. Class 9 got zero. You're done. Your shares are gone bro." 😂

NOT SO FAST 🏴☠️

"PLEASE TAKE FURTHER NOTICE that the Plan and its provisions are binding on the Debtors, the Wind-Down Debtors, and any Holder of a Claim or an Interest and such Holder's respective successors and assigns, whether or not the Claim or the Interest of such Holder is Impaired under the Plan, and whether or not such Holder voted to accept the Plan."

Read that again. Slowly.

The Plan and its provisions are BINDING ON ANY HOLDER OF AN INTEREST.

HOLDER OF AN INTEREST = LEGACY BBBYQ SHAREHOLDER 🎆

Not "applicable to." Not "noticed upon." BINDING. I believe that word has a very specific meaning in federal bankruptcy law but correct me if I'm wrong. It creates enforceable mutual obligations under a confirmed order of a United States Bankruptcy Court.

WHY DOES THIS MATTER?

Let's break down why this one sentence is so significant.

First, the Plan defines "Interest" as any equity security under Section 101(16) of the Bankruptcy Code. That definition includes shares, warrants, options, and rights to purchase equity. So when this notice says "any Holder of an Interest," it is referencing legacy BBBYQ shareholders. Full stop 👀

Second, take a look at the grammar. It does not say "Holder of a Claim or Interest." It says "Holder of a Claim or AN Interest." That article "AN" makes Interest a fully independent, standalone legal category. Claim holders are bound. Interest holders are bound. Each on their own terms. Each with independent legal significance.

Third, "successors and assigns." If equity were truly dead, there would be no successors or assigns. You cannot succeed to something that no longer exists. I suspect Cole Schotz and Kirkland & Ellis included this language because these Interests have a continuing legal existence sufficient to generate succession rights. I believe this means anyone who holds legacy shares today, steps directly into the shoes of a party bound by this Plan.

Finally, "WHETHER OR NOT the Interest of such Holder is Impaired under the Plan, and WHETHER OR NOT such Holder voted to accept the Plan."

🎆BOOM 🎆

Cole Schotz and Kirkland & Ellis systematically destroyed every possible escape hatch. Impaired? BOUND. Unimpaired? BOUND. Voted yes? BOUND. Voted no? BOUND. Deemed to reject under 1126(g) and never voted at all? BOUND. There is no exit from this framework. ✅

BUT HERE'S THE THING PEOPLE MISS 👀

Binding is a two-way street.

A federal court cannot constitutionally impose the obligations of a confirmed Plan on a class of parties while simultaneously denying them any benefit from that same Plan. That's not how due process works and I don't think that's how the Bankruptcy Code works either. If you are inside the Plan's legal tent, you are subject to its terms AND entitled to invoke its provisions.

Remember, you don't lock the door on an empty room. And you don't bind parties you've truly eliminated. You bind parties who still have a role to play.

Let's pivot for a moment 😀

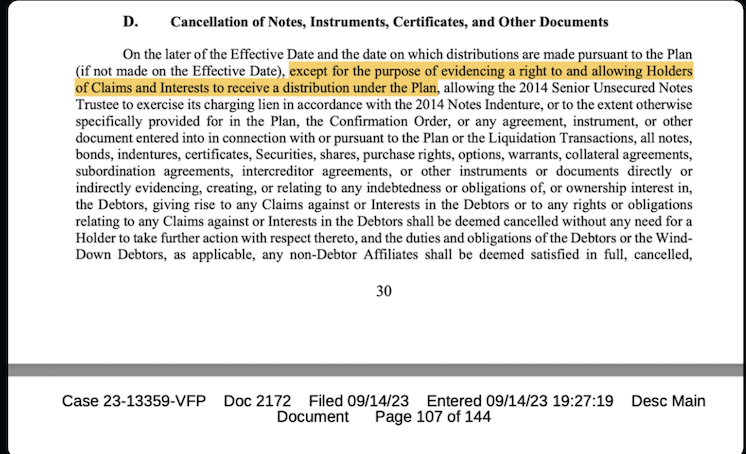

Remember Article IV.D of the Plan? The cancellation provision? It says all securities are cancelled "except for the purpose of evidencing a right to and allowing Holders of Claims and Interests to receive a distribution under the Plan."

Read that again. Holders of Claims AND INTERESTS. The Plan explicitly preserves the evidentiary function of legacy equity securities (retaining records of who held what) to the extent that they can evidence a right to receive a distribution down the road.

Combined with the binding provision mentioned previously, I believe we now have a closed legal loop: Interest holders are bound to the Plan, their securities can be preserved for evidencing a right to receive a distribution, and the injunction preventing them from taking action expires when all distributions are complete.

Pivoting Back to the Original Find Again

Remember, the original Notice contained within Exhibit 99.1 was signed on September 29, 2023, which was the same day as the Effective Date, the precise moment the Plan became enforceable federal law. 🔥

This wasn't some boilerplate afterthought. This is elegant architecture hiding in plain sight. It doesn't announce itself. It doesn't need to. We are witnesses to world-class professionals building something truly meant to endure and last. 🍻

WRAPPING UP

The Notice of Confirmation Order on page 3 contains a single sentence that permanently BINDS ALL HOLDERS OF INTERESTS to the 20230930-DK-Butterfly-1, Inc. Plan and its provisions, including successors and assigns, with NO EXCEPTIONS for impairment status or voting status.

I believe this binding is mutual under federal law. You cannot be bound to a Plan you have no stake in, right? As mentioned previously, the cancellation provision also separately preserves the evidentiary function of legacy equity securities (i.e., records of who owned what) for potential distribution purposes down the road. Together, these provisions demonstrate that legacy equity was never expelled from the Plan's legal universe. Instead, it appears that it was repositioned within it!

Anyways, the original binding provision identified today in this SEC filing appears to be the LEGAL BRIDGE that connects legacy equity holders directly to whatever this Plan still has in store for us next, and it was sitting quietly in this SEC filing since the Effective Date!

🦋🧱 BRICK BY BRICK🧱🦋

English

If we only get $15 after 3 years I don't know what to say 😂 (Credit to The Brokage)

English

@Trickster42069 I thought "death spiral convertibles" was clear.

English

80HD retweetledi

@PhantomBlack699 thank you for the compliment and clarity. do you think if I start punching air after reading your comment, that my fate can change?

English

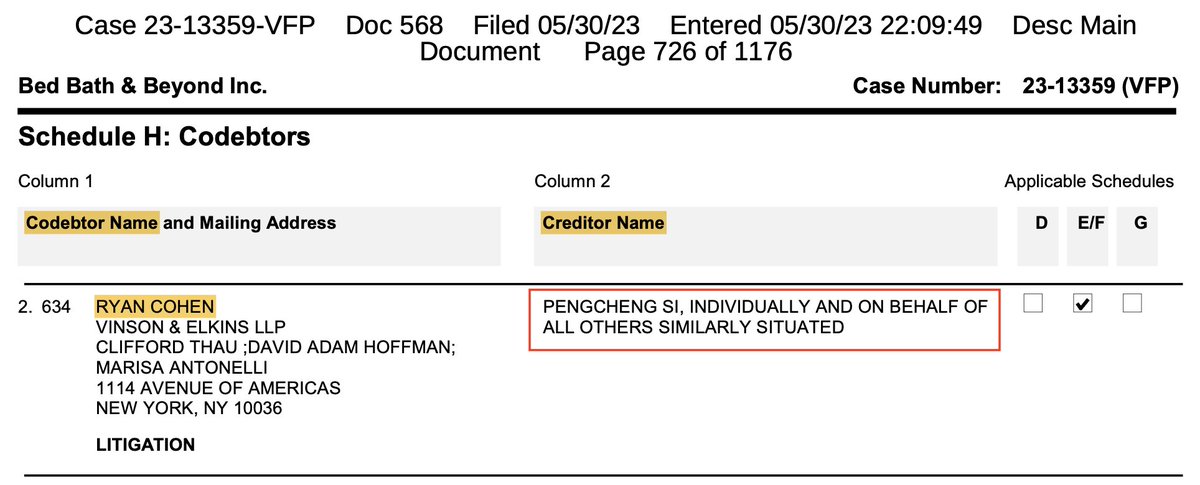

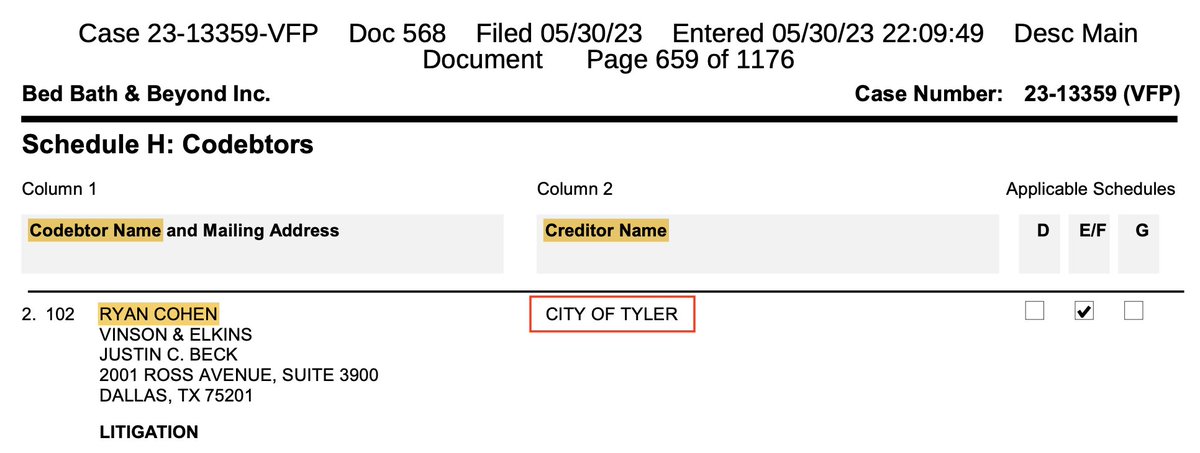

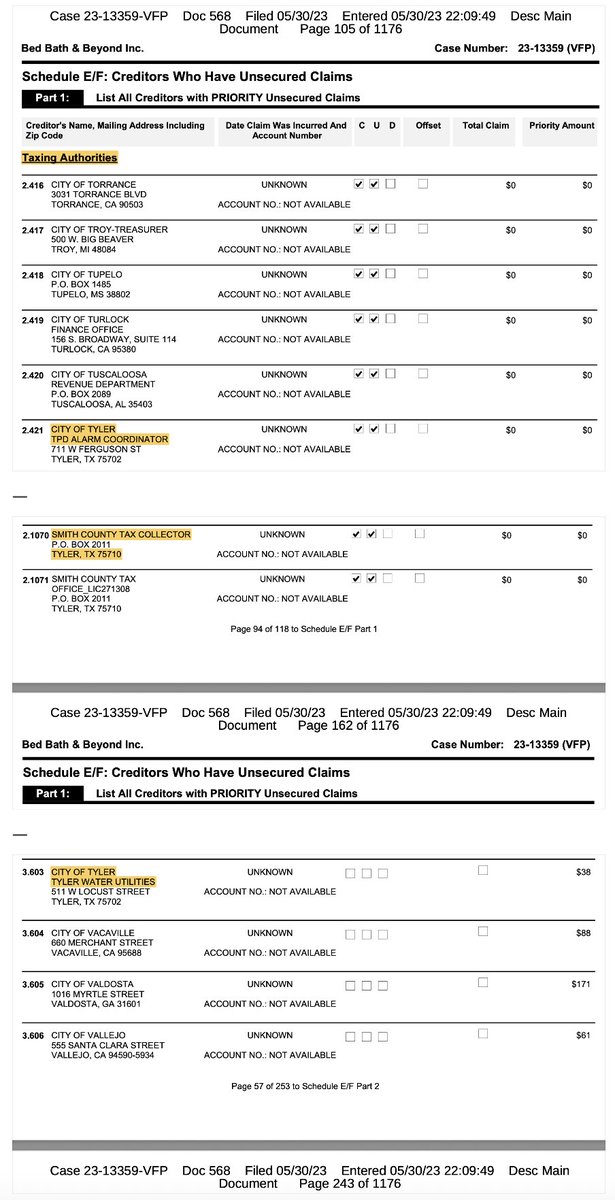

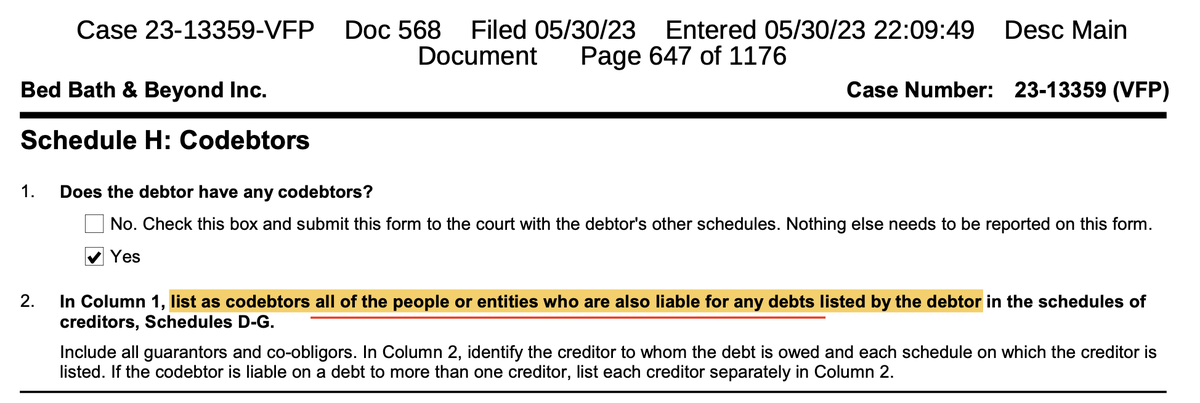

one thing I didn't get to spend much time discussing on the Space call was the $BBBYQ Statement of Financial Affairs and it disclosing RC's co-debtor status.

first I want to establish the importance and legitimacy of this disclosure. the Statement of Financial Affairs (SOFA) is a document that must be filed with a Chapter 11 and has to be accurate; it is considered perjury to lie. the point of it is to give a history of financial transactions and activities leading up to a company's bankruptcy filing:

"The Statement of Financial Affairs is designed to disclose relevant financial information to the bankruptcy court, the trustee, and your creditors. It helps establish an accurate picture of your financial affairs, including your income, expenses, assets, liabilities, and recent financial transactions. The form assists in assessing your eligibility for bankruptcy relief and aids in determining the best course of action for your case."

jdsupra.com/legalnews/unde…

I am trying to emphasize this point because you cannot dismiss the significance of seeing RC listed here and it is not a mistake. do you really think his lawyers would allow for that when he had two ongoing litigations involving the company? that is ridiculous. it is also not "because he is being sued", that argument is either repeated because someone was too lazy to look, they don't understand what they are reading or they are intentionally being misleading. it is laughable.

I'll explain how we know:

here we see RC listed opposite the plaintiff of his class action suit before the lead was changed to Bratya. it is listed.

here is why you cannot dismiss finding RC in the sofa:

because here we see RC listed again, separate of the class action and 16(b) lawsuits. unless you believe that a municipality where there used to be a $BBBY and Baby store location is involved in the litigations against RC, this is what is referred to as a "slam-dunk find."

the previous comment was obviously a joke but in case you really did believe (or someone has claimed) that Tyler, TX and several other municipalities are involved in the lawsuits, further in the sofa we will see the city of Tyler disclose to the court exactly why they are in the creditor list:

to no one's surprise, they are a taxing authority. do you remember the Texas Taxes and the Comptroller, for who the Plan reserved the right to pursue a third-party for taxes owed by the OldCo? who would agree to that? only an acquirer.

RC is listed in the full financial disclosure presented to the US Court that he is a co-debtor of the Old $BBBY company, opposite of a municipality claiming they are owed for county taxes and water utility bills.

do you really think that RC's attorneys would allow a "mistake" of this magnitude to exist, when he is being litigated relating to the same business? do you think the signatory for the Statement of Financial Affairs, would make the "mistake" of falsely attributing company debts to a third party, under penalty of perjury? of course not. that would be laughable.

make no mistake, that is exactly what this says. RC is a co-debtor for the OldCo and a co-debtor is a person other than who is filing for bankruptcy, who is also legally responsible for paying the debts. there is no alternative interpretation. and you don't have to believe me, it is written at the top of the sofa itself:

liable for debt nearly a year after he sold his shares. RC had a chip on his shoulder seeing how the former board treated him and his ideas for transforming the company. he could not turn away from the destruction of shareholder value resulting from the "October 2020 plan" and he held everyone to account as the Holder of Interests through the third-party release.

look at the information filed with the US Court and decide for yourself. the facts are right there in front of you and they do not care how difficult it is for anyone "to get there" with their own opinion to believe them.

English

He opened the door with Bed Bath because he saw an opportunity. Once that door closed, he sold.

He made lemonade out of lemons, which I respect him for.

He saw the same opportunity in GME. Within 2 years, GME looked different. He kept his promise because that opportunity grew the longer he stayed.

As $GME shareholders, we supported this. We hit positive earnings and haven't looked back. He knows we need something big to bring us to the next level, and I have no doubt he's going to deliver

I voted for the guy who knows when to walk away and when to commit.

💎👐🚀

Ryan Cohen@ryancohen

The Hollow Men American capitalism is rotting from the head down. We have replaced the "Owner-Operator"—the risk-taker-with a new, parasitic class of corporate bureaucrat: The Risk-Free Insider. By "Insider," I am not referring to a specific title. I am referring to the entire administrative state that has captured the modern corporation. This includes the Directors who exist solely to collect fees, the Executives who exist solely to collect bonuses, and the Managers who exist solely to hire consultants. These are the hollow men of the boardroom. They are masters of PowerPoint. They wear the right suits. They say the right buzzwords about "governance" and "ESG." But they are mercenaries fighting a war with someone else’s ammunition. In a functioning economy, authority is tied to liability. If you make a bad decision, you lose your own money. That fear of loss is the only thing that keeps a business honest. It forces you to cut waste, obsess over the customer, and stay late to fix what is broken. Today, we have severed that link. We have rigged the game so that heads, the Insider wins; tails, the shareholder loses. If the stock goes up, the Insider collects a massive performance bonus. If the stock crashes due to their own incompetence, they are fired with a "Golden Parachute" worth tens of millions. They are gambling with the house’s money, and they never leave the table poorer than they arrived. This looting starts in the boardroom. We have normalized a "Country Club" culture where directors are selected based on social profiling rather than their ability to build a business. The modern board member is often a professional tourist—paid an average of $350,000 a year. Let’s be brutally honest about what that number represents. The average director is paid nearly five times the GDP per capita of the United States. They earn more for attending four quarterly lunches than the vast majority of Americans earn in five years of hard labor. And for what? Most of these directors are "over-boarded," sitting on three or four boards simultaneously. They treat directorships as a gig economy for the elite. They fly in, rubber-stamp a compensation package they didn't read, and fly out. They collect checks from companies they do not understand, do not use, and certainly do not love. They are not there to ask hard questions. They are there to be collegial. They are there to protect the other Insiders. And what happens when these boards hire executives who also have no personal capital at risk? We get the Delegation Economy. When a Risk-Free Insider faces a crisis—bloated expenses, a broken supply chain, or a stale product—they do not roll up their sleeves. They hire a consultant. They pay a strategy firm millions of shareholder dollars to produce a 100-page deck telling them what they already know. This is not management. It is intellectual money laundering. They use shareholder capital to buy an insurance policy for their own careers. If the plan fails, they can blame the consultants. They delegate the work because they are terrified of the responsibility. They would rather preside over a slow, comfortable decline than risk a bold mistake. While American Insiders are busy optimizing their severance packages, our global competitors are optimizing their products. They are not slowed down by bureaucracy. They are not waiting for a slide deck. They are outworking us. If we continue to fill our C-suites with administrators instead of operators, we will lose our edge. We will see iconic American franchises hollowed out by fees, managed for the benefit of the Insiders, while the true owners—the shareholders—are left holding the bag. The time for polite governance is over. If we want to save the American economy from mediocrity, we must demand a return to the "Owner’s Mentality." We need leaders who treat shareholder capital with the same reverence they treat their own savings. The era of the Risk-Free Insider must end.

English

@AustinTobitt So basically what you are saying is Ryan Cohen is a failed activist investor. Right. Got ya.

GIF

English

80HD retweetledi

80HD retweetledi

The Hollow Men

American capitalism is rotting from the head down. We have replaced the "Owner-Operator"—the risk-taker-with a new, parasitic class of corporate bureaucrat: The Risk-Free Insider.

By "Insider," I am not referring to a specific title. I am referring to the entire administrative state that has captured the modern corporation. This includes the Directors who exist solely to collect fees, the Executives who exist solely to collect bonuses, and the Managers who exist solely to hire consultants.

These are the hollow men of the boardroom. They are masters of PowerPoint. They wear the right suits. They say the right buzzwords about "governance" and "ESG." But they are mercenaries fighting a war with someone else’s ammunition.

In a functioning economy, authority is tied to liability. If you make a bad decision, you lose your own money. That fear of loss is the only thing that keeps a business honest. It forces you to cut waste, obsess over the customer, and stay late to fix what is broken.

Today, we have severed that link.

We have rigged the game so that heads, the Insider wins; tails, the shareholder loses.

If the stock goes up, the Insider collects a massive performance bonus. If the stock crashes due to their own incompetence, they are fired with a "Golden Parachute" worth tens of millions. They are gambling with the house’s money, and they never leave the table poorer than they arrived.

This looting starts in the boardroom.

We have normalized a "Country Club" culture where directors are selected based on social profiling rather than their ability to build a business. The modern board member is often a professional tourist—paid an average of $350,000 a year.

Let’s be brutally honest about what that number represents. The average director is paid nearly five times the GDP per capita of the United States. They earn more for attending four quarterly lunches than the vast majority of Americans earn in five years of hard labor.

And for what?

Most of these directors are "over-boarded," sitting on three or four boards simultaneously. They treat directorships as a gig economy for the elite. They fly in, rubber-stamp a compensation package they didn't read, and fly out. They collect checks from companies they do not understand, do not use, and certainly do not love.

They are not there to ask hard questions. They are there to be collegial. They are there to protect the other Insiders.

And what happens when these boards hire executives who also have no personal capital at risk?

We get the Delegation Economy.

When a Risk-Free Insider faces a crisis—bloated expenses, a broken supply chain, or a stale product—they do not roll up their sleeves. They hire a consultant. They pay a strategy firm millions of shareholder dollars to produce a 100-page deck telling them what they already know.

This is not management. It is intellectual money laundering.

They use shareholder capital to buy an insurance policy for their own careers. If the plan fails, they can blame the consultants. They delegate the work because they are terrified of the responsibility. They would rather preside over a slow, comfortable decline than risk a bold mistake.

While American Insiders are busy optimizing their severance packages, our global competitors are optimizing their products. They are not slowed down by bureaucracy. They are not waiting for a slide deck. They are outworking us.

If we continue to fill our C-suites with administrators instead of operators, we will lose our edge. We will see iconic American franchises hollowed out by fees, managed for the benefit of the Insiders, while the true owners—the shareholders—are left holding the bag.

The time for polite governance is over.

If we want to save the American economy from mediocrity, we must demand a return to the "Owner’s Mentality." We need leaders who treat shareholder capital with the same reverence they treat their own savings. The era of the Risk-Free Insider must end.

English

80HD retweetledi