@SilasAveryNZ @RoaringRagnar @TanukiTreasury Mined supply makes no difference at this point. Daily trading volume is 300k plus. 450 new mined BTC doesn’t matter.

English

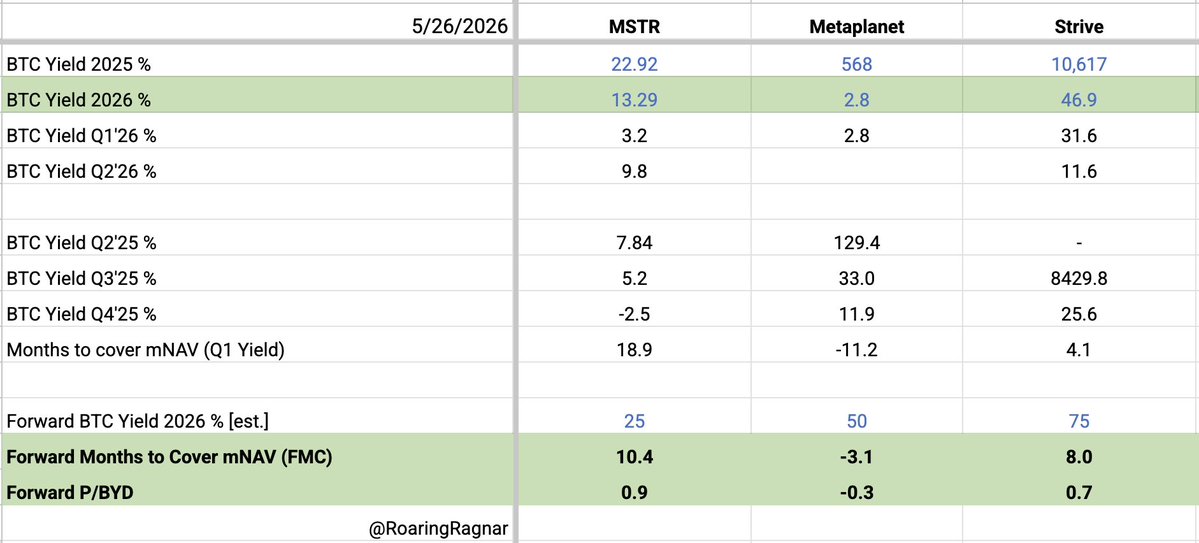

Jesse

26 posts

SpaceX claims they have identified the largest TAM in human history at $28.5 trillion. (Source: S-1) But... the TAM for Digital Credit is an order of magnitude larger. $STRC

You could literally - - Stack 5 BTC at $70k ($350,000 total) - Bitcoin reaches $1M - Borrow just 4% against it yearly That’s $200,000/year in liquidity No capital gains tax & still holding the asset Why are people still trading their Bitcoin away?

Instructions say this’ll take 3 people 18 hours to build… I’m going to do it in 9 hours by myself.

Got bad news for @Strive ( $ASST) investors - y'all are royally f*cked for a long while. Tl;dr: • 100% of shares from the warrant exercises and 98.9% of the existing commons have been registered for sale. • $1.35 could end up being the price ceiling for a while. This is based on the 424(b)(7) prospectus [1] filed on Oct 10 that allows shares from the PIPE unlock to be sold. Details below. Number of shares and warrants: • 449,696,631 shares of Class A outstanding as of Oct 1 • 177,246,462 unexercised Pre-Funded Warrants w/ EP of $0.0001 per sh • 545,629,627 unexercised Traditional Warrants w/ EP of $1.35 per sh Once all the warrants are exercised, here's how the numbers for Class A breaks down: • Beneficially Owned: 1,296,210,145 • Registered for Sale: 1,283,904,392 (99%) • Not for Sale: 13,870,799 (1%) In summary: • 100% of both warrant types have been registered for sale • Only 1% of the Class A commons have NOT been registered for sale (Ignoring Class B and options since not relevant to this analysis.) What does this mean? Based on my experience with PIPE unlock plays over the years, I think: 1⃣ Share price will remain depressed for the foreseeable future since more shares than are currently outstanding are waiting to be dumped. 2⃣ The 177M Pre-funded Warrants will likely be dumped first since EP is effectively $0. 3⃣ The 545M Traditional Warrants will see dumps as price rise above the EP of $1.35. Even if the holders do not dump, market will anticipate it and front run by selling longs and loading shorts. (e.g. Metaplanet.) 4⃣ Credit to CEO @ColeMacro for not registering his shares for sale. 5⃣ Shame on CFO @BenPhiat for registering his for sale. What's the rush, man? 6⃣ Management will claim that "registering to sell" doesn't necessarily signal "intent to sell," let alone an impending sale. Every management team says this. They have to. We were not born yesterday and have seen this play out before. I wonder which of $ASST or $NAKA remains in purgatory longer. Sources: [1] #tSUM" target="_blank" rel="nofollow noopener">sec.gov/Archives/edgar…

🗓️ THE SCHEDULE IS LIVE! 🗓️ #B4E2026 is 3 days away — and now you can see exactly what's in store. ⚡️ Thursday through Sunday. Workshops, keynotes, side events, and more. Portland, May 22–23 (+ pre & post events). 👉 bitcoinisforeveryone.com/schedule 🎟️ Last chance to grab your ticket: bitcoinisforeveryone.com/tickets #BitcoinIsForEveryone #BTC #PDX