Max Drawdown

576 posts

@agentedelcaos23 @BorisMacro You can still make money with it but it's not an investment, only for traders with good risk management

English

@_Max_Drawdown @BorisMacro A lot of people here try to pump it, is very weird they have “contracts” and “sells” but the company always going down, we need to start to say this Is garbage

English

$LASE got absolutely destroyed during pre-market and opening on warrant exercises. Show's over for now I was stopped out right below the diagonal myself. I might revisit this later.

Boris Macro@BorisMacro

Laser Photonics has reached a stand-still right above the diagonal support. Interestingly enough this PR was released yesterday: "LASE Group's Fonon Technologies Advances to Next Phase of U.S. Air Force Battle Lab Evaluation for Laser Shield Anti-Drone Technology" tradingview.com/news/reuters.c… Any news on even a small US Air Force contract or this lining them up for further defense contract competitions will cause volatility to return to the upside. On the risk management side I don't want this to drop too far below the diagonal, even on a potential liquidation wick, as it's still a micro cap company.

English

@_Max_Drawdown Welcom eto team Amkor :) Today was really the last exit before my scenario would have been collapsed. they announce a partnership with TSMC. Margins need to improve. If that happens next earnings it gonna fly.

English

$US100 $US500 $SPY

Today is the day of reckoning. If no buyers show up when the market opens, it could mark the beginning of a bear market. More on this once a decision has been made.

English

Max Drawdown retweetledi

Excellent price action for $ENHA, which is up over 13% in today's trading session in an overall red market. The S/R areas based on volume profile to watch in the near term are marked on the chart.

My mid to long term Fibonacci target lies around $17.60, for the more patient and ambitious among us.

Boris Macro@BorisMacro

"You want the truth? You can't handle the truth!" - A Few Good Men 1992 Why did this movie quote from 34 years ago resonate so strongly with so many people? Because people unironically can't handle the truth. The truth makes them uncomfortable. The truth challenges their made-up belief system. The truth requires you to neutralize your ego to be receptive to it. Only those who speak the absolute unfiltered truth will receive the most vile of hatred, slander and abuse. It's Biblical in a sense. I joined X a few months ago because I felt like I can speak and share my own truth here. I don't need new friends and social media will never be my career. I have already experienced that simply disagreeing with someone on the valuation of a company will result in people blocking or slandering me. God forbid you start mentioning the factually incorrect slop and course-selling posters. This is not because of me though, it is because my observation makes them uncomfortable. It challenges their belief system. If I am able to debunk claims made by their favorite stock influencer, what does that tell them about their (likely irresponsibly large) positions in the same stocks this influencer told them to buy? On the other side of this spectrum lie companies, people and ideas that make them uncomfortable. This is because they expose uncomfortable truths in unapologetic manners. Why did they not want to go near $PLTR below $20, but do they feel comfortable now that other people tell them it's okay to own? It is ego and assumption that will cost you money in the financial market. Stop looking for others to confirm your bias and start challenging your belief system. This is why a real trading strategy requires back testing and consistent methods of data processing. While I mostly dabble in the financial side of things I believe this phenomenon exists across every aspect of humanity. We are seeing the same in the fitness and sport industry. People cling to a status of being "natural" or "clean". This resulted in the "fake natty" syndrome that is especially predominant in bodybuilding. This gaslights people, especially teenagers, into believing they will achieve similar results without enhancements. This leaves them disillusioned at best, and results in them taking horrible health decision at worst. Similarly everyone that's not themselves involved in the relevant sport seems to be "surprised" when their idols and heroes turn out to have been performance enhancing drugs. More so than surprised though, they feel offended. They feel offended because their belief system was challenged, and this implicitly tells them something about their perception. This is why The Enhanced Games have attracted so much hate (free publicity) and slander based on misconceptions and lies. It exposes an underlying truth that is uncomfortable to most people. Real growth can only happen outside of the comfort zone. Learn to endure discomfort. Learn to be wrong and adapt. I did not plan this post, but I was inspired to write it just now since @C_Angermayer started following me. I realize it differs a lot from my usual trading setups. Nevertheless I believe this is much more important than any single setup. I have been following his fund @ApeironInvests for quite a while, initially due to their investment thesis surrounding companies conducting research in psilocybin. If anything is able to remove the egotistical filter standing between you and reality it would be psilocybin. While I have not taken any large quantities in several years I still actively micro dose. It means a lot to me being such a small and new account on X to have him follow and engage with me. Quality over quantity. TLDR; - Unapologetically speak and live your truth - Allow your ego and belief system to be challenged - Buy $ENHA - Follow @C_Angermayer and @ApeironInvests

English

@BorisMacro @agentedelcaos23 True but other people have been pumping it as if it was a safe bet. Even some people I know from real life. Now they learned a good lesson the hard way.

English

@agentedelcaos23 @_Max_Drawdown I never posted any fundamental analysis on it. I just predicted the initial rally from $0.90 to $4.50. It's a micro cap company suitable for degenerate trading.

English

@agentedelcaos23 @BorisMacro When I did my DD I was also shocked, that's why I always used a stop loss and small size. They got a history of dilution and I think there are investigations regarding fraud or something like that, I would need to look it up as it has been quite some time since I did this DD.

English

@BorisMacro I told you, this fuckin company Is a scam, just garbage

English

@BorisMacro Damn I'm glad I didn't take this trade I was considering it when you posted it but I was too busy 😂 I hope you got out in time without slippage 🙏🏻

English

@CaesarCapitalz When I see real capitulation and when the broader market is not at ATH

English

$NBIS is now down ~40% in just one month.

It’s definitely starting to look attractive again at current levels.

At what point would you consider buying back in?

Caesar Capital@CaesarCapitalz

I just sold ~5% of my $NBIS at $290! Celebrating being up 1,100% in 13 months! Current situation: I’ve taken my initial investment out and have now sold around 12% of my $NBIS position in total. I can now ride all my remaining shares for free! My next PT is $1,000! I believe we can get there by the end of 2027 or early 2028! Forever grateful @nebiusai ❤️

English

@italianinvesto @daniel_koss Couldn't agree more. It's not responsible for himself and for his subs if he does stuff like this. Who knows how many people followed him into this trade... I think there are times one can consider going all-in but it's very rare. I only did it two times in the last two years.

English

Max Drawdown retweetledi

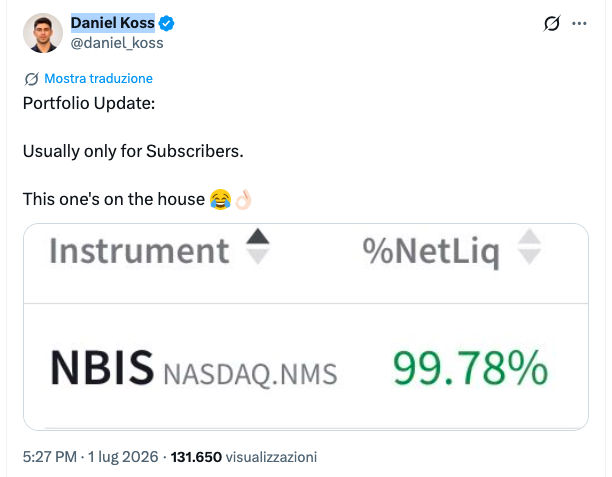

This guy @daniel_koss went all-in on $NBIS on the 1st of July.

As of now he burnt 25% of his net worth and he also blocked me for some reason.

I'm long Nebius but I find this type of extreme investing strategy really absurd.

Nebius is great for sure, but it's an unprofitable "early stage" company.

As much as this kind of post is cool and fun for the community, that's not a wise financial decision, I'd say it's rather a suicidal financial decision.

For 1 guy who wins with an "all-in" strategy there are 20 other guys who lose everything.

What do you guys think about this? Let me know

English

Max Drawdown retweetledi

Feels bad, -49.4% drawdown this month after the recent crash.

My portfolio is mainly AI chokepoints and bottlenecks.

In the memory, photonics, robotics, and upstream semis, (on margin) which all tend to be higher beta than others. But reduced leverage recently from the crash.

I see a lot of people making fun of the drop or AI names, saying it’s obvious that:

- “AI is a bubble”

- “memory/kospi is a bubble”

- “photonics is a bubble”

- “humanoids won’t get anywhere”

- “neoclouds will get replaced by hyperscalers like Meta”

And a bunch of retail + bots saying “sell everything, it’s never going to recover”.

But I have conviction that all these themes are backed by structural revenue growth or technological shifts.

And I’ve had similar drawdowns back when there admin threatened global tariffs, before markets pulled off a recovery.

I personally have a longer horizon + higher tolerance for volatility than others, to see how this plays out.

Especially considering a lot of retail view things on a week to week basis: no, my thesis isn’t wrong yet if I project revenue inflection in H2 2027 and it’s 2026 now.

Anyway, feels bad short term just wanted to share anyway for transparency.

Serenity@aleabitoreddit

Agreed! It’s nice to remember your thesis during a market crash. From my own personal thesis, if $AAOI hits $1.4B quarterly revenue start of Q3 2027. Which is annualized $5.6B off a $8B MC. Is it “over” for the company if that revenue ramp hasn’t even shown up in the quarterly earnings… when it’s 2026? Same applies to my CPO sector exposure like $SIVE, an architecture shift led by $NVDA. If scale out volume ramps from H2 2026 into 2027, and scale up heavily volume ramps into 2028. Is it “over” that $0 -> $91B TAM expansion (per GS) hasn’t even hit yet? With robotics like Agility, is it over in 2026 if the listing hasn’t even happened yet and humanoids haven’t ramped? I personally think current market conditions are a reflection of liquidity and leverage, not individual fundamentals. It’s brutal for everyone to see KOSPI, TW, Nikkei, and AI, space, robotics sector stocks crash recently. Especially when there’s a lot of irrational behavior stemming from those leverage. In the end, we can’t tell you what stocks to buy, what timeframe you should sell, how to size your positions, or what you should do. Only share personal thoughts or research and track if they get validated over time. So it’s extremely important to build your own thesis, since everyone has unique risk tolerance or investing timeframes. And that usually leads to having higher conviction during crashes.

English

@HedgebergCom Many thanks 🙏🏻 I was looking to get into Amkor for a very long time now but it just went up with no real pullback 😂 When the market turns around this thing will probably fly 🙂 Didn't they even get a deal after you published your article and I think earnings have also been good.

English

@_Max_Drawdown Yes, I will. $60 is the key level. If I personally would buy here if I wouldn't be invested. Cause a break below would be really bad and I could have a close stop loss in case we see a bear market

English

@BorisMacro Also exited long time ago fortunately. What about $SIVE and $LPK , any ideas where they can bottom out or are you taking it day by day?

English

My stoploss got hit on $XFAB. While I remain interested in the European semiconductor space, I need to see more technical confirmation before reconsidering a position.

Boris Macro@BorisMacro

$XFAB is back in my area of interest. Downside risk here is limited right below the Fibonacci support level below my marked diagonal.

English

The $SIVE dump is brutal.

Thankfully I got in at 8 SEK and exited at 80 SEK.

10x and out.

Burak Finance@burak_finance

I got many questions about why I sold $SIVE today. Bought at 8 SEK. Took profits at 80 SEK on the way up. Sold at 75 SEK, this was a 10-bagger. Sold purely on TA. 75 SEK was a key level of defence. Once it broke, I sold immediately to protect the gains. It’s already trading at 67 SEK now. I have nothing against the company; I’m still long-term bullish and may look to jump back in lower or higher. I warned my subscribers before I sold and alerted them the second I executed. With the cash, I opened a new position today.

English

$NFLX Three years ago, Netflix bottomed in July. I was buying back then.

Today, the chart is again deeply sold in July.

Price is sitting under both the 20 & 50 EMA.

Will this July mark the next major low?

English

Max Drawdown retweetledi

$NBIS

If there is a chance for a short term rebound before heading lower it must happen now.

Hedgeberg | Technical Precision. Fundamental Depth@HedgebergCom

$NBIS - seems like Nebius doesn't have the power to break the $222. It's becoming more likely to see lower prices before bouncing. Wave c would bring us down to roughly $170 imo. I cut the position at $215.2 today. Wave c isn't confirmed yet though.

English

@HedgebergCom Interesting. You expect further downside then I guess.

English

@_Max_Drawdown No I didn't add more

English

$NBIS

The $205 obviously didn't hold. I still think we'll see a rebound though to $240. It's heavily oversold on the lower time frames and we almost hit the theoretically target of the double top.

English