Estou no estande da MEXC na Blockchain Conference Brazil! #MEXCEventRocks @MEXC_Portuguese @MEXC_Official

HT

krazypepe

2.5K posts

@_krazyniko_

Always a Degen | Sometimes a Quant

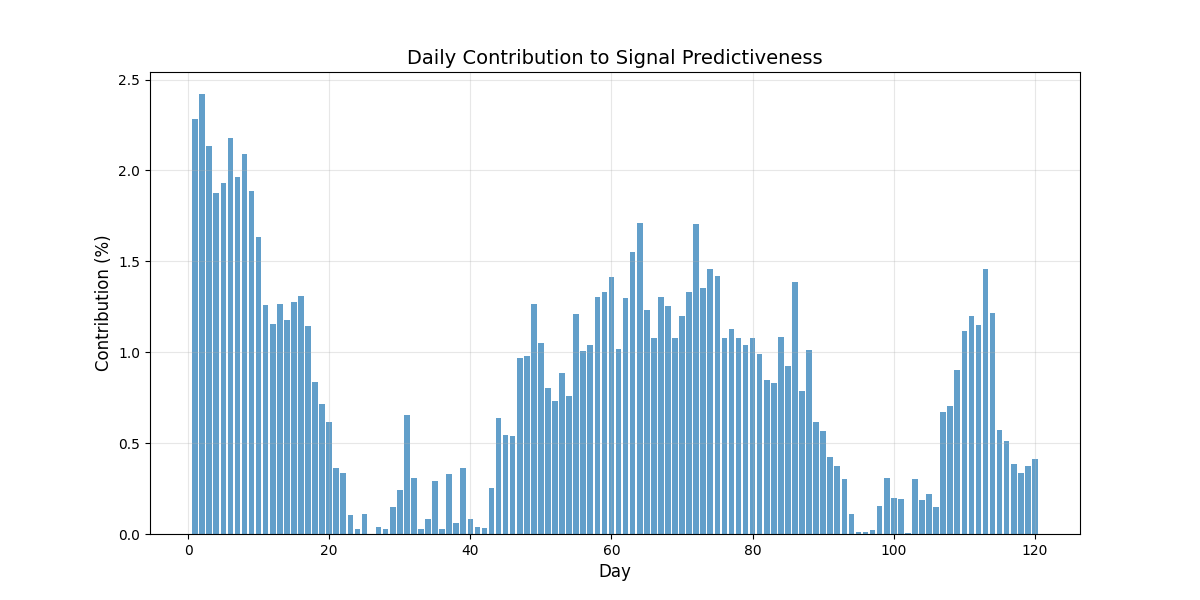

@moritzheiden @risk_biscuits @bylethquant Trend on crypto is most predictive 12-48hrs from signal, typically a continuous version of the same kind of signals the non-vol target systems use are better than looking at short timeframes This is correlation with next day returns at 1 day, 2 days, etc

finally, started modifying my infra to model for continuous signal exposure 3 days ago, and finished it today. now I can both model for traditional binary signals and continuous signals, with just a change of a variable. let's analyze what changed and reconcile. 1/n