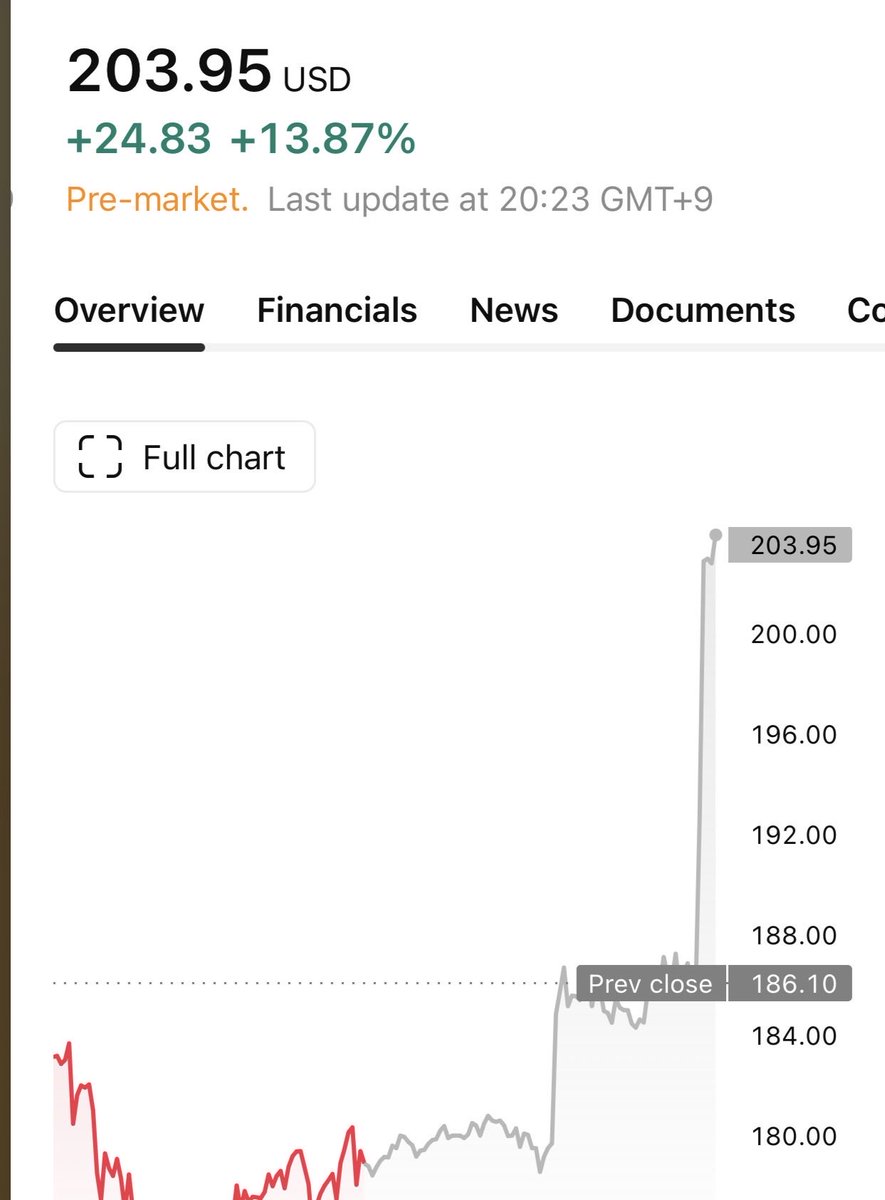

@Sandeman52 It's not that common to feel that something is generational. So many great opportunities in the market but the only one I was brave enough to go heavy was $NBIS.

English

visionarius

1K posts

@_visionarius

Seeing a future you can't see yet.

🚨❌ FC Porto president André Villas Boas denies reports on Robert Lewandowski: “As you can imagine, it’s financially impossible for us even to think about Lewandowski”.

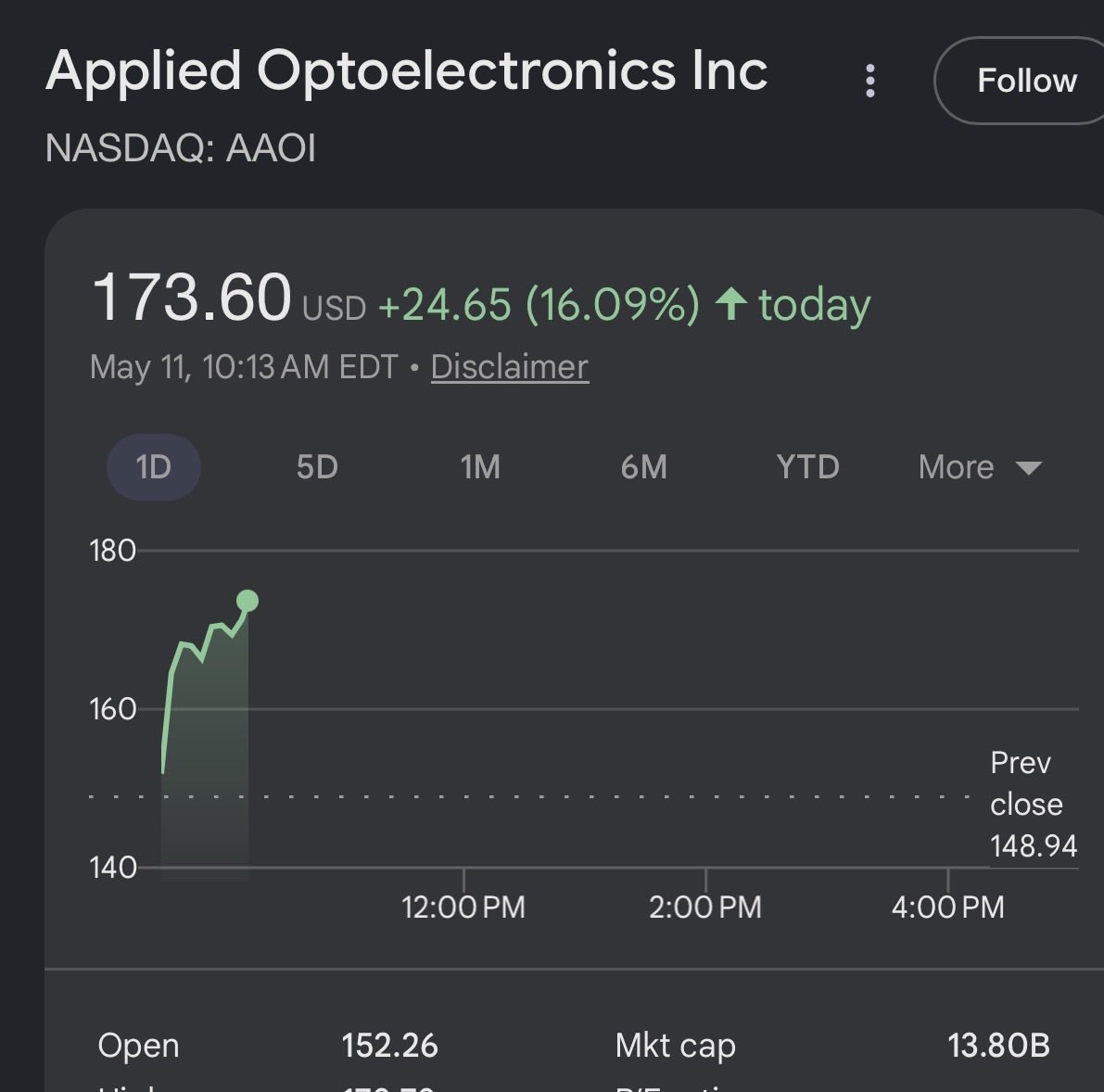

$AAOI reported earnings, it's actually extremely positive so far contrary to market reactions. Like all 2027 hyperbolic forward growth companies: Nobody should care about current financials. Key things market missed was: AOI: hit They hit 100K units/month capacity for 800G transceivers. And: -> "Significant larger growth expected starting in Q3 as capacity comes online" If you do look at financials: It's ~29.2% non GAAP gross margin on ~$151.1M revenue, guiding $180-$198m Q2. We already know from Lumentum earnings that it's more of capacity bottleneck, not a demand one. And anything they make they sell out. It's a forward growth story, so important thing aside from these notes is the earnings call on hyperscaler demand implications and capacity ramp.

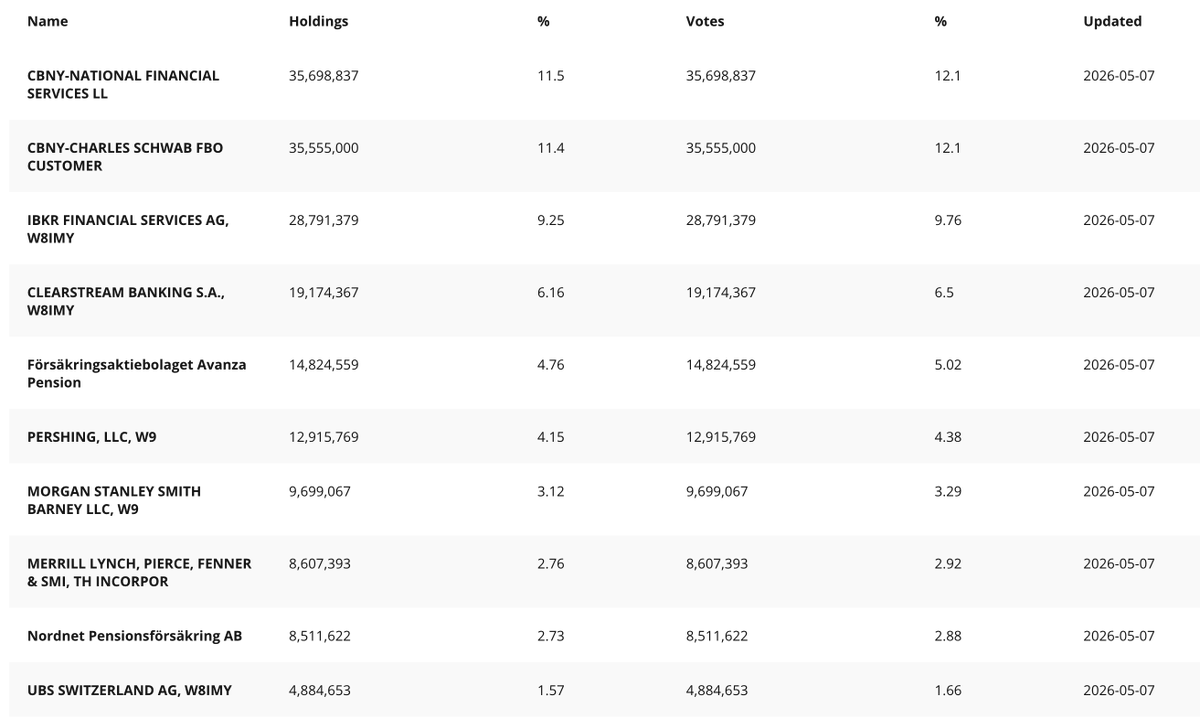

@aleabitoreddit Updated shareholder list………

I'm still laughing how much Swedish hate their own frontier companies so much. That they write hit pieces every day on $SIVE. This one was entertaining: Local journalists show up to an empty $SIVE administrative building uninvited. Because they can't fathom the CEO is in Silicon Valley or design team is working on US Gov CHIPS act dev in the US. And because there weren't many cars parked outside + CFO wouldn't take questions about secretive hyperscaler deal financials. They wrote a random negative hit piece. By repeating "There are several who make lasers like these and Sivers are far from alone". Several like $LITE, $COHR, $60B+ companies. and reported earlier that "CPO is nothing special, it's been around for years." While GS projects CPO going from $1B -> $91B TAM over the next two years. Even put "Plans" in quotation marks because they didn't think Sivers is supplying lasers to $JBL 1.6T LRO. IMO, $SIVE ends up as a $10B+ company next year, especially if they follow what $LITE / $COHR did with downstream IP integration to capture more of CPO module BOM. Just don't think Swedish people understand hyperscaler supply chains, concept of forward growth, or the fact that employee count doesn't equate to revenue. Transfer of control from local Swedish -> West is always appreciated, as this was a majority owned local retail company before.

Introducing Tab Tab Tab, our new prompt auto complete engine in @GoogleAIStudio's vibe coding experience. Now when you show up with your fuzzy ideas, you can rely on Gemini to fill in the blanks : )

The current bottleneck: Transformers/Switchgear. Trade Idea: Long Hammond (~2.2B CAD / ~$1.5B USD) at 184 CAD. They dominate the market for: -Transformers (dry, multi year bottleneck ~23% of market), -serve to switchgear (2-3Y bottleneck) -and manufacture liquid too (5Y, larger bottleneck) I personally anticipate components price hikes like NAND, as $AMZN, $MSFT and others compete for allocation. You might have seen: “Half of US data center builds have been delayed or canceled, growth limited by shortages of power infrastructure”… Then you go further: “To address shortages… Canada, Mexico… became the biggest suppliers of high-power transformers for AI data centers to AI data centers” Guess who is in Canada (Guelph).. Mexico (Monterrey 3 and 4)… and the US? Hammond Then here’s the reason the articles cite why hyperscaler DB buildouts are falling apart: “Major reason behind these setbacks is the availability of key electrical components — such as transformers, switchgear”. Institutions are probably looking at Powell, Eaton, and others… but little do they know? Companies like these actually buy Hammond’s transformers to put inside their own switchgear (“strong sales into data centres, switchgear manufacturers") Their market share over the transformers market is actually pretty large (eg. ~23% dry). The most compelling signal: -> 122% Y/Y 2025 backlog increase. And we can infer this to be 1B+ CAD. Eg. company achieved 898m CAD in sales in 2025, capacity ceiling. Management said close of Q3 2025 orders were valued at 53% of the entire closing third-quarter backlog. Given that Q4 2025 revenue was 254 million and the backlog is "more than doubled," we can infer a total backlog value exceeding 1 billion CAD. Also: “Gross margin compression last year was due to the buildout of their Mexico facility, but both gross margins are expected to increase and the facility expansions are expectied to turn into accelerated revenue Q2 2026)” which is now. Downside is if raw material costs (copper, electrical steel) spike again, but given this bottleneck, they can price hike. Personal FWD P/E estimates would be ~18-21 for 2026, <15 for 2027 from volume ramp. But I think it’s possible to hit single digit fwd P/E if they do price hikes mixed with hyperscaler emergency orders. But that might get a little mixed with the new acquisition. Regardless still looks cheap. Just a TLDR: $AMZN, $MSFT, $META, $GOOGL, $ORCL datacenter are being bottlenecked because of a lack of transformers/switchgear. Seems like markets missed this little player with large market share, despite backlog visibility and increasing revenue from capacity expansion coming online. I personally found it pretty compelling, so I went long. Just sharing my personal thoughts, of course DYOR before making any decisions yourself.

Where is Serenity????????