Adu

1.4K posts

Adu

@Adu

🏡 NYC • 💼 Formerly X1, Twitter

New York, USA Katılım Eylül 2011

286 Takip Edilen417 Takipçiler

If you had to convince a beautiful girl from nyc to move to Sunnyvale, CA

How would you do it?

English

NYC is no longer a city, it is an algorithm.

If you live in, say, Cincinnati, when you go to get ice cream with your friends, you really are just going to get ice cream with your friends.

In NYC, this is not possible. You cannot just go to get ice cream, because, against your will, you are very self-consciously “someone who lives in NYC, going to get ice cream with their friends, in NYC.”

You are never able to achieve full presence of mind because you are constantly placing yourself inside a chapter in some made up, schizophrenic and highly disorienting book.

Put another way, as a New Yorker, you do not live in a city, but a massive, procedurally generated simulation of one. You are nothing more than a vapid unit of flesh and bone trapped since a Baudrillardian infinity mirror, where the references have their own references.

You become more of a vague concept than a real person—some strange, soulless mix of ambition and violent/sexual impulses—and in your constant confusion you fail to ever become a true subject.

You pay $17 for the ice cream cone. Then, you pull out your list of saved Instagram Reels which tell you where to get reservations for pasta later.

When you arrive, you find yourself stuck in yet another long line, with people who look just like you.

The longer you wait in lines like these, the harder it becomes to ever recover the soul of the person you were before you moved into your East Village studio.

Connor Paton@connorpaton

nyc has a froyo epidemic line is pure insanity

English

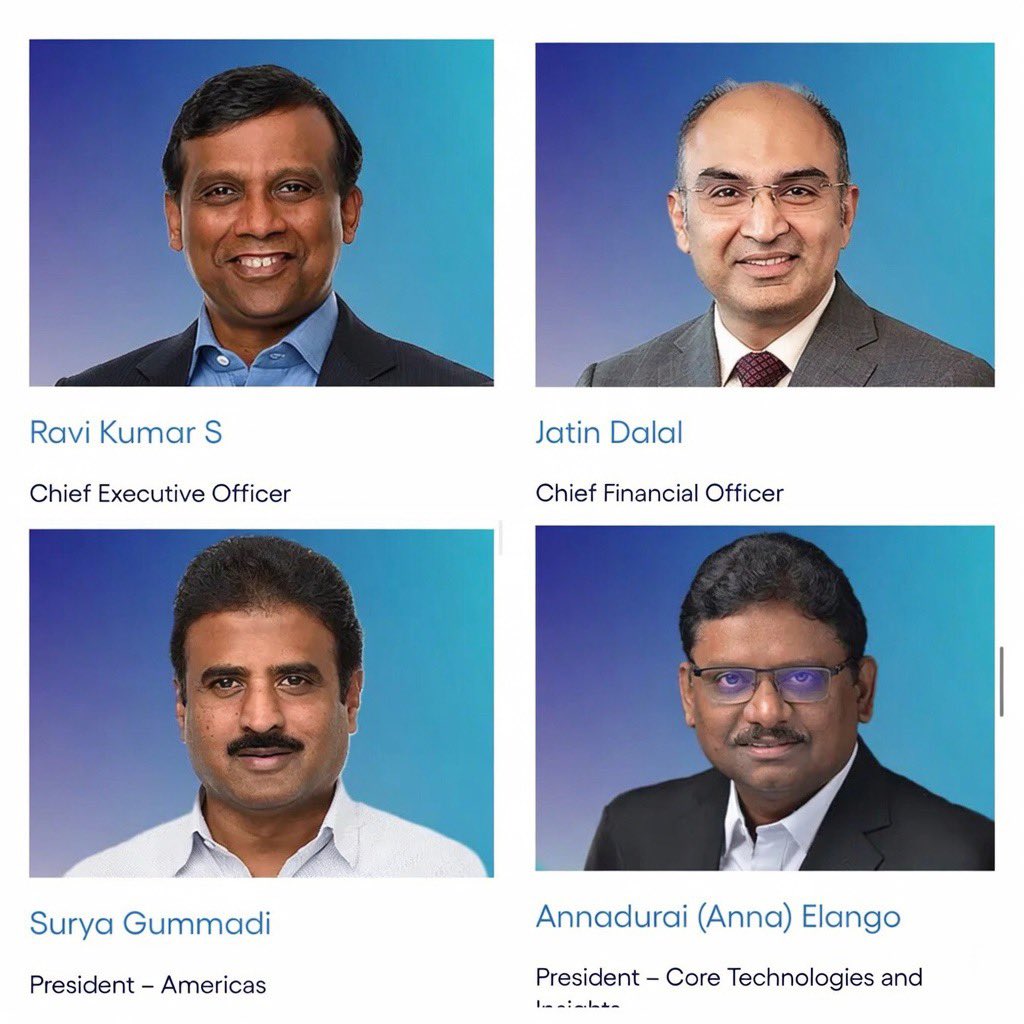

Cognizant's executive leadership team

What do you notice?

English

@ryanvogel odd take unless you know the terms of deal, and if so please share them

English

bro google is fumbling AI so bad that they had to PARTNER WITH AN EXTERNAL SEARCH PROVIDER

Exa@ExaAILabs

We're excited to partner with Google to offer Grounding With Exa inside of Gemini models! Using Exa's agent-first search, Gemini models can now access billions of websites, technical docs, papers, people, companies, and more. 10^18🤝10^100

English

Software will never return to the era when it commanded 50x revenue multiples…

Software companies now have to fight not just for growth, but for survival itself.

This is a truly great piece. You should definitely read it.

Brad Lyons@blyons151

In August I wrote a thesis I never published. The funds I was warning were key Crossover Research clients, so I stayed quiet. Since then, 𝗦𝗼𝗳𝘁𝘄𝗮𝗿𝗲 𝗺𝘂𝗹𝘁𝗶𝗽𝗹𝗲𝘀 𝗮𝗿𝗲 𝗱𝗼𝘄𝗻 𝟱𝟬%+. Salesforce $CRM, ServiceNow $NOW, Adobe $ADBE, Workday $WDAY all off 40% from highs. Thomson Reuters $TRI dropped 16% in a single session on the Anthropic legal agent launch. The SaaSpocalypse arrived. So here's the follow-up. Not commentary on what happened, but where I think this goes next. Most vertical SaaS companies aren't underperforming because their software is bad. 𝗧𝗵𝗲𝘆'𝗿𝗲 𝘂𝗻𝗱𝗲𝗿𝗽𝗲𝗿𝗳𝗼𝗿𝗺𝗶𝗻𝗴 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝘁𝗵𝗲𝘆 𝗻𝗲𝘃𝗲𝗿 𝗯𝘂𝗶𝗹𝘁 𝘁𝗵𝗲 𝘀𝗲𝗰𝗼𝗻𝗱 𝗯𝘂𝘀𝗶𝗻𝗲𝘀𝘀. And the first business is under attack. For twenty years, one of the biggest SaaS moats was engineering complexity: deep technical talent, long roadmaps, compounding codebases that were genuinely hard to replicate. 𝗔𝗜 𝘂𝗽𝗲𝗻𝗱𝗲𝗱 𝘁𝗵𝗮𝘁 𝗮𝗹𝗺𝗼𝘀𝘁 𝗼𝘃𝗲𝗿𝗻𝗶𝗴𝗵𝘁. Product development is democratizing to operators with no code background but strong product vision. Look at Anthropic: they've built the engine and are shipping lookalike products at a cadence that would have taken a legacy SaaS vendor three years of roadmap, with a fraction of the headcount. That pace can kill legacy businesses overnight. 𝗜𝗳 𝘁𝗵𝗲 𝗲𝗻𝗴𝗶𝗻𝗲𝗲𝗿𝗶𝗻𝗴 𝗺𝗼𝗮𝘁 𝗶𝘀 𝗴𝗼𝗻𝗲, 𝗳𝗼𝘂𝗿 𝗺𝗼𝗮𝘁𝘀 𝗿𝗲𝗺𝗮𝗶𝗻: 𝗱𝗶𝘀𝘁𝗿𝗶𝗯𝘂𝘁𝗶𝗼𝗻, 𝗽𝗿𝗼𝗽𝗿𝗶𝗲𝘁𝗮𝗿𝘆 𝗱𝗮𝘁𝗮, 𝘄𝗼𝗿𝗸𝗳𝗹𝗼𝘄 𝗯𝗿𝗲𝗮𝗱𝘁𝗵, 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗶𝗼𝗻. The first three are moats the company builds. The fourth is a moat the company captures, and it's the one most resistant to AI disruption. 𝗥𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝗰𝗼𝗺𝗽𝗹𝗲𝘅𝗶𝘁𝘆 𝗰𝗿𝗲𝗮𝘁𝗲𝘀 𝘀𝘄𝗶𝘁𝗰𝗵𝗶𝗻𝗴 𝗰𝗼𝘀𝘁𝘀 𝘁𝗵𝗮𝘁 𝗵𝗮𝘃𝗲 𝗻𝗼𝘁𝗵𝗶𝗻𝗴 𝘁𝗼 𝗱𝗼 𝘄𝗶𝘁𝗵 𝗽𝗿𝗼𝗱𝘂𝗰𝘁 𝗾𝘂𝗮𝗹𝗶𝘁𝘆. Once a vendor is embedded in a compliance workflow, ripping them out means re-attesting, re-auditing, and re-certifying every downstream process. The buyer isn't paying for software, they're paying for the accumulated paper trail. Tyler Technologies ($TYL) is the clearest version of the pattern. State and local government software across courts, public safety, assessment, and ERP. Every module is married to statutory process, FIPS, CJIS, audit trails, and procurement cycles that take years. TYL is down 42% TTM and 2026 guidance came in soft, but the moat didn't break. Revenue still compounded, and government procurement runs on five-year cycles, not five-week news cycles. Veeva is the sharper version. Revenue up 16% in FY26, Q4 beat, the stock still down 25%. The market is selling execution, not weakness. Guidewire in P&C insurance, where regulatory filings and rate approvals anchor the stack, sits in the same setup: still compounding ARR, still winning cloud conversions, multiple reset anyway. Same pattern across all three: multiples compressed, fundamentals intact. The moat is the regulatory surface area itself, and it compounds because the rules get more complex, not less. 𝗜 𝘄𝗮𝘀 𝗹𝗼𝗻𝗴 𝗣𝗮𝗹𝗮𝗻𝘁𝗶𝗿 𝗮𝘁 $𝟭𝟯 (read that here: x.com/blyons151/stat…). 𝗡𝗼𝘁 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗺𝗼𝗱𝗲𝗹 𝗼𝗿 𝘁𝗵𝗲 𝘁𝗼𝗼𝗹𝗶𝗻𝗴. 𝗕𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝘁𝗵𝗲 𝗼𝗻𝘁𝗼𝗹𝗼𝗴𝘆. Palantir is the proprietary-data version of the regulatory thesis. Once Palantir sits between the customer and their own data, ripping it out means rebuilding the data model from scratch. Snowflake and Databricks never had that entrenchment layer. AIP bootcamps then turned the data moat into a distribution moat: 660 bootcamps in a single quarter, 94% y/y US customer deal growth, bookings at 1.9x sales. Own the data, ship functional AI on top of it, let the GTM compound. Every vertical incumbent has a version of this available. The question is whether they'll build it before a challenger does. But regulatory insulation is necessary, not sufficient. Plenty of vendors inside regulated verticals are still getting squeezed because they never became AI-native. BlackLine ($BL) and Trintech are feeling it in close and reconciliation as Numeric, Maximor, and Stacks build AI-native from day one. nCino ($NCNO) in banking faces the same challenge. The regulatory moat buys you time. It doesn't buy you the decade. 𝗧𝗵𝗲 𝘄𝗶𝗻𝗻𝗶𝗻𝗴 𝗳𝗼𝗿𝗺𝘂𝗹𝗮 𝗶𝘀 𝗱𝗮𝘁𝗮 𝗼𝗿 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆 𝘀𝘂𝗿𝗳𝗮𝗰𝗲 𝗮𝗿𝗲𝗮 𝗽𝗹𝘂𝘀 𝗳𝘂𝗻𝗰𝘁𝗶𝗼𝗻𝗮𝗹 𝗔𝗜, 𝗻𝗼𝘁 𝗼𝗻𝗲 𝗼𝗿 𝘁𝗵𝗲 𝗼𝘁𝗵𝗲𝗿. Look at why Claude is winning. Anthropic isn't competing on model benchmarks, they're competing on functional workflow. Building for the user, not the leaderboard. That's the playbook vertical incumbents need to run. Take the moat you already have, whether it's regulatory or data-entrenchment, layer genuine workflow AI on top, and the challenger can't catch you. The vendors that do both win the decade. The ones that rely on inertia alone get caught. The ones that ship AI without an anchor get commoditized. You need both. 𝗧𝗵𝗲 𝗯𝘂𝘆𝗲𝗿 𝗶𝘀 𝘁𝗲𝗹𝗹𝗶𝗻𝗴 𝘆𝗼𝘂 𝘁𝗵𝗶𝘀 𝗽𝗹𝗮𝗶𝗻𝗹𝘆. A study we ran with Battery Ventures on AI adoption in the Office of the CFO (battery.com/blog/first-cod…) surveyed 129 finance leaders at companies from $50M to $5B+ in revenue. 77% said they want to uplevel existing systems with AI from new vendors that layer onto existing systems. Only 15% want to replace their current system of record with an AI-native platform. The incumbent wins if they ship AI. The AI-native challenger wins only if the incumbent doesn't. The signal shows up in our VoC data too. In regulated verticals, mission criticality scores cluster above 9, and NPS doesn't track satisfaction, it tracks switching friction. Customers will tell you the product is mediocre and still score it 9 on "would not switch" because the compliance team vetoes any alternative. 𝗧𝗵𝗮𝘁'𝘀 𝘁𝗵𝗲 𝘀𝗶𝗴𝗻𝗮𝘁𝘂𝗿𝗲 𝗼𝗳 𝗮 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲-𝗶𝗻𝘀𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗻𝗱𝗼𝗿, 𝗮𝘀 𝗹𝗼𝗻𝗴 𝗮𝘀 𝘁𝗵𝗮𝘁 𝘃𝗲𝗻𝗱𝗼𝗿 𝗶𝘀 𝗮𝗰𝘁𝗶𝘃𝗲𝗹𝘆 𝘀𝗵𝗶𝗽𝗽𝗶𝗻𝗴 𝗮𝗴𝗮𝗶𝗻𝘀𝘁 𝘁𝗵𝗲 𝗔𝗜 𝗰𝘂𝗿𝘃𝗲. Which brings us back to the second business for everyone outside the regulated or data-entrenched moat. Seat ARR got them to $100M. But with the shift to agentic workforce structures, partial human capital replacement, and pricing pressure compressing margins, the traditional SaaS model has to transform fast. The next $500M comes from monetizing the installed base: marketplace rake on demand they generate for their own customers, capital products underwritten by their own transaction data, supplier monetization, brand partnerships, group buying. The assets are already sitting there. Captive SMB audience. Proprietary transaction and behavioral data. A distribution pipe (the UI itself) that delivers new products at near-zero CAC. 𝗪𝗵𝗮𝘁'𝘀 𝗺𝗶𝘀𝘀𝗶𝗻𝗴 𝗶𝘀 𝗼𝗿𝗴𝗮𝗻𝗶𝘇𝗮𝘁𝗶𝗼𝗻𝗮𝗹 𝘄𝗶𝗹𝗹. Monetizing the installed base requires a different org than the one that got you to scale. Different GTM, P&L optics, and talent. Founders and boards under-invest because year one looks worse before it looks better, and public markets punish any SaaS multiple that starts to look like fintech or marketplace. So the second business never ships. The round prices in the optionality. The multiple compresses. The exit underwhelms. 𝗧𝗵𝗿𝗲𝗲 𝗱𝗶𝗹𝗶𝗴𝗲𝗻𝗰𝗲 𝗾𝘂𝗲𝘀𝘁𝗶𝗼𝗻𝘀 𝗻𝗼𝘁 𝗲𝗻𝗼𝘂𝗴𝗵 𝗶𝗻𝘃𝗲𝘀𝘁𝗼𝗿𝘀 𝗮𝗿𝗲 𝗮𝘀𝗸𝗶𝗻𝗴: 𝟭. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝗿𝗲𝘃𝗲𝗻𝘂𝗲 𝗰𝗼𝗺𝗲𝘀 𝗳𝗿𝗼𝗺 𝘀𝗼𝘂𝗿𝗰𝗲𝘀 𝗼𝘁𝗵𝗲𝗿 𝘁𝗵𝗮𝗻 𝘀𝘂𝗯𝘀𝗰𝗿𝗶𝗽𝘁𝗶𝗼𝗻 𝗮𝗻𝗱 𝗽𝗮𝘆𝗺𝗲𝗻𝘁 𝗽𝗿𝗼𝗰𝗲𝘀𝘀𝗶𝗻𝗴? Under 5%, they haven't started. 10 to 20%, thesis is live. Over 20%, it's working. 𝟮. 𝗛𝗼𝘄 𝗵𝗮𝗿𝗱 𝘄𝗼𝘂𝗹𝗱 𝗶𝘁 𝗯𝗲 𝘁𝗼 𝗿𝗲𝗰𝗿𝗲𝗮𝘁𝗲 𝘁𝗵𝗶𝘀 𝗰𝗼𝗺𝗽𝗮𝗻𝘆 𝗳𝗿𝗼𝗺 𝘀𝗰𝗿𝗮𝘁𝗰𝗵 𝘄𝗶𝘁𝗵 𝗔𝗜 𝘁𝗼𝗱𝗮𝘆? If a well-funded team with Claude and six engineers could rebuild the functional product in nine months, the software isn't the moat. The moat has to live somewhere else: proprietary data, a network, integrations, or regulatory surface area the challenger can't clear. If you can't point to at least one, you're underwriting a melting ice cube. 𝟯. 𝗪𝗵𝗮𝘁 𝗽𝗲𝗿𝗰𝗲𝗻𝘁 𝗼𝗳 𝘁𝗵𝗲 𝗯𝘂𝘆𝗲𝗿'𝘀 𝘀𝘁𝗶𝗰𝗸𝗶𝗻𝗲𝘀𝘀 𝗶𝘀 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗼𝗿𝘆, 𝗮𝗻𝗱 𝘄𝗵𝗶𝗰𝗵 𝘄𝗮𝘆 𝗶𝘀 𝘁𝗵𝗲 𝗿𝘂𝗹𝗲 𝘀𝗲𝘁 𝗺𝗼𝘃𝗶𝗻𝗴? A regulatory moat evaporates if the regulation simplifies. Underwrite the direction of travel, not just the current state. 𝗔𝗻𝗱 𝘁𝗵𝗲 𝗰𝗹𝗼𝗰𝗸 𝗶𝘀 𝘁𝗶𝗴𝗵𝘁𝗲𝗿 𝘁𝗵𝗮𝗻 𝗺𝗼𝘀𝘁 𝗿𝗲𝗮𝗹𝗶𝘇𝗲. Retention in enterprise SaaS has largely been defined by the pain of systems replacement, not genuine moat. If the stickiness isn't backed by proprietary data, a harvesting flywheel, or regulatory surface area, those vendors are about to get disrupted. Pure seat-based pricing is dying unless vendors embrace agent-seat models, and LLM providers have been subsidizing the market on token cost, with recent pricing shifts signaling cash reserves aren't infinite. 𝗛𝗲𝗿𝗲'𝘀 𝘁𝗵𝗲 𝘂𝗻𝗱𝗲𝗿𝗮𝗽𝗽𝗿𝗲𝗰𝗶𝗮𝘁𝗲𝗱 𝗽𝗼𝗶𝗻𝘁: 𝗔𝗜-𝗻𝗮𝘁𝗶𝘃𝗲 𝗰𝗼𝗺𝗽𝗲𝘁𝗶𝘁𝗼𝗿𝘀 𝗵𝗮𝘃𝗲 𝘄𝗼𝗿𝘀𝗲 𝗴𝗿𝗼𝘀𝘀 𝗺𝗮𝗿𝗴𝗶𝗻𝘀 𝘁𝗵𝗮𝗻 𝗦𝗮𝗮𝗦 𝗶𝗻𝗰𝘂𝗺𝗯𝗲𝗻𝘁𝘀, 𝗻𝗼𝘁 𝗯𝗲𝘁𝘁𝗲𝗿. Inference costs haven't collapsed, and burning VC cash to subsidize unit economics is a bridge, not a business model. The incumbents should be winning on P&L. They're losing on product velocity and AI-readiness. That's a solvable problem if the board has the will to ship. Vendors without a second business, without a data moat, and without regulatory insulation will still lose, despite having better margins than their AI-native challengers. Customers switch on features and speed, not on unit economics. 𝗘𝗻𝘁𝗲𝗿𝗽𝗿𝗶𝘀𝗲 𝗮𝗻𝗱 𝗿𝗲𝗴𝘂𝗹𝗮𝘁𝗲𝗱 𝘃𝗲𝗿𝘁𝗶𝗰𝗮𝗹𝘀 𝗮𝗿𝗲 𝘁𝗵𝗲 𝗹𝗮𝘀𝘁 𝘀𝗮𝗳𝗲 𝗵𝗮𝗿𝗯𝗼𝗿, 𝗮𝗻𝗱 𝗼𝗻𝗹𝘆 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗼𝗳 𝗱𝗮𝘁𝗮 𝗯𝗿𝗲𝗮𝗱𝘁𝗵 𝗮𝗻𝗱 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲. Everywhere else, the premium is about to get competed away. Any fund underwriting vertical SaaS exposure right now should be asking the second-business question before the next check clears. DM me, email me brad@crossoverresearch.com, or let's chat about your portfolio/underwriting process (book.crossoverresearch.com). Crossoverresearch.com

English

NYC’s Zohran Mamdani has reached a deal with Governor Kathy Hochul to introduce the state’s first tax on second homes worth over $5 million owned by out-of-state residents.

English

@KobeissiLetter @NateSilver538 @grok I would love to be able to verify this data. What is the best way to do that?

English

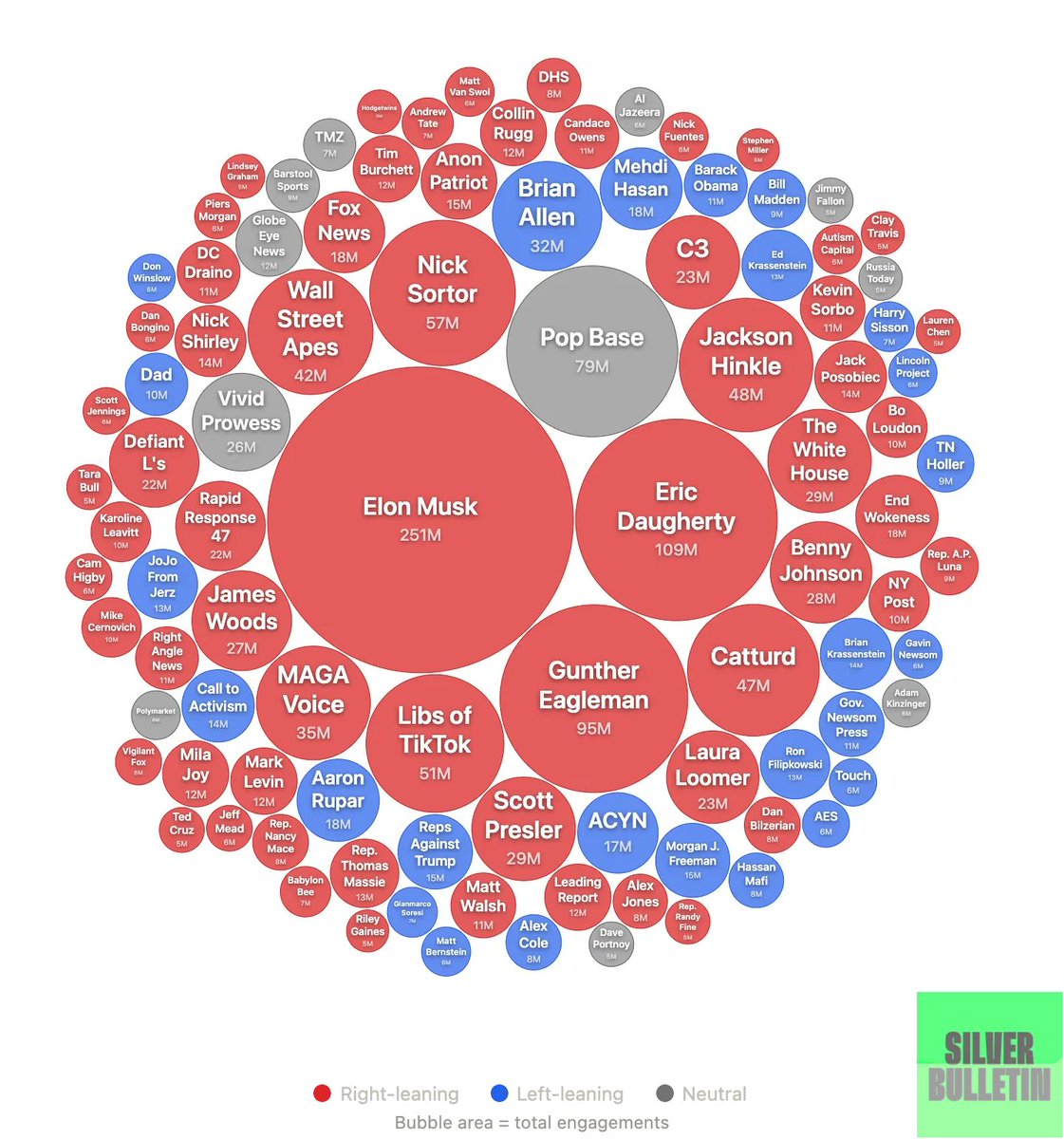

@NateSilver538 This analysis is flawed.

We did nearly 50M engagements YTD (which would make us top ~10 on your graphic), yet no mention of our account on this list.

Your data is likely incorrect.

English

These are the Twitter/X accounts with the most engagement so far in 2026. I suppose I had some intuition for how bad it was, but jeez, this is what you get when the ecosystem is broken.

English

This little illuminated dragon is very happy about Pretext. He's too busy having fun to care about people's "hot takes" on how "it's not that special."

(This little dragon also only works on desktop right now but maybe I'll do mobile later)

illustrated-manuscript.vercel.app

Cheng Lou@_chenglou

My dear front-end developers (and anyone who’s interested in the future of interfaces): I have crawled through depths of hell to bring you, for the foreseeable years, one of the more important foundational pieces of UI engineering (if not in implementation then certainly at least in concept): Fast, accurate and comprehensive userland text measurement algorithm in pure TypeScript, usable for laying out entire web pages without CSS, bypassing DOM measurements and reflow

English

@KobeissiLetter @grok which email of his was breached and what did it have access to? was the account actively in use?

English

BREAKING: The DOJ says FBI Director Kash Patel’s personal email has been breached by hackers.

English

@_10delta_ @grok can you advise on what the best 2-3 numeric indicators would be to show whether or not this plan is working? Different metrics perhaps make more or less sense at different stages of the plan. How do they look now?

English

3 weeks ago I argued the US goal in Iran is to seize the global oil spigot. Venezuela in January -> Iran in February.

Neutralize every supply channel outside the dollar system within 90 days. Achieve a compliant successor government and complete energy dominance.

The oil thesis was the obvious layer. However, when you zoom out & view the last four years as a single sequence rather than isolated geopolitical events, the architecture of the grander US plan becomes visible.

1st was Europe, which laid the groundwork.

The Ukraine conflict provided the justification for sanctions that collapsed Russian pipeline gas from 150 billion cubic meters to 40.

Then Nordstream was destroyed, which rewired the entire European energy system permanently. The US went from supplying 28% of Europe's LNG in 2021 to 58% by 2025, exporting a record 111 million MTs, the 1st country in history to break 100 MT.

Europe was transformed from a customer with options into a captive market now purchasing its survival in USD.

2nd was Syria.

The fall of Assad severed the critical node connecting China's Belt & Road Initiative to the Mediterranean.

The trilateral railway linking Iran, Iraq & Syria, designed to bypass Western maritime chokepoints, was completely destroyed.

This isolated Iran geographically & cleared the path for what came next.

3rd was Venezuela.

In January the US effectively took control of the world's largest heavy crude reserves. The US Gulf Coast has the most advanced refining complex on earth, specifically built for heavy sour crude. Phillips 66, Valero & the rest are now positioned to process hundreds of thousands of barrels of Venezuelan crude daily.

The US captured a massive strategic reserve & solidified its position as the dominant exporter of refined petroleum products, an industry worth $110 billion in 2025 alone.

Venezuela & Iran were the two major oil supply channels that existed outside the dollar system. Both produce heavy crude sold primarily to China & evaded US financial supervision. Both now being neutralized within 90 days, which leads us to..

4th is Iran & the Middle East energy shock.

Israel struck Iran's South Pars gas field, the world's largest natural gas reservoir. Iran retaliated against Qatar's Ras Laffan, the single largest LNG facility on earth, responsible for a fifth of global supply. QatarEnergy's own assessment is that 17% of export capacity is gone and recovery will take up to 5 years. The Strait of Hormuz is closed. European gas prices spiked 70%. Asian spot prices doubled.

The only remaining scaled supplier? The United States.

If Iran falls & a successor government is installed that the US controls or influences (the Delcy model described weeks ago) then roughly 40 to 45 million barrels per day of global production out of 103 million is effectively under US control. OPEC becomes irrelevant because the US coalition is now the marginal producer. Now add the gas dimension & it goes beyond oil.

This war is solidifying the petrodollar system as it evolves into a hybrid petro/LNG-dollar. The old system was built on Saudi crude priced in USD. The new system is built on American crude plus American gas from the Gulf Coast, with no alternative supplier of comparable scale. The dependency is deeper because LNG infrastructure requires long term contracts & regasification terminals that lock buyers into supply relationships for decades. Europe & the Pacific allies (Japan, South Korea, Taiwan, etc.) cannot pivot away as there is nowhere left to pivot to. They're now locked into the US energy system.

The market confirms this. DXY went from 96 to 101. Gold down ~20% from its January all time high. Bitcoin down 20% on the year. Brent above $100. European & Asian institutions are liquidating precious metals and crypto to buy dollars because they need dollars to buy the only remaining scaled energy supply. The world is selling its gold to buy American energy in American currency. The dollar is now being weaponized through energy dependency.

The structural repricing is happening regardless of how the conflict resolves.

But the US grand strategy goes deeper..

Artificial intelligence is a physical industry. It runs on power and chips. Data centers require massive uninterrupted baseload electricity, primarily provided by natural gas. Semiconductor fabrication requires helium & rare earths.

By choking the Strait of Hormuz & crippling Middle Eastern LNG & helium production, the US is systematically degrading China's ability to power its data centers & fabricate semiconductors at scale.

The US is energy self sufficient, especially with newly captured Venezuelan reserves & expanding Gulf Coast capacity running on domestic gas.

On the other hand, China is import dependent & every joule it imports effectively now transits chokepoints the US Navy controls..

Iran was the Belt & Road's overland energy bypass, the corridor that allowed China to mitigate the Malacca Trap. With Iran neutralized that corridor is severed. China faces a world where its compute infrastructure competes for scraps on a depleted global LNG market, while American data centers run at full capacity on domestic energy.

Russia is next in the sequence. A post-war Iran reopening under US influence competes directly with Russia for the same refineries in China & India at lower cost. Iran's production costs are lower. Russia loses its last structural advantage in heavy crude & its economic lifeline. Additionally, under the Iran war cover, Ukraine has been opportunistically destroying Russian energy infrastructure & all signs point towards Russia being at the end of the line. The message from Washington becomes very simple: we dismantled two regimes in three months, your economy is about to get crushed, sign the Ukraine deal.

Then Trump sits down with Xi holding every card. Complete energy dominance. The hybrid petro/LNG-dollar fortified, Iran cleared, Russia cornered, & China facing the Malacca Trap fully closed with no remaining energy bypass.

Israel & the GCC are absorbing the kinetic cost of a conflict whose primary beneficiary, counter to the mainstream narrative, is actually America (First). Qatar offline for 5 years reprices the entire global gas market in favor of US exporters for the remainder of the decade. The Gulf states face years of rebuilding. Europe faces its 2nd energy crisis in four years.

Sure, the average American might face temporary moderate inflation & higher gas prices. But if you are the architect of the US empire & you view the rise of China & Chinese ASI as an existential winner takes all scenario, the collateral damage is acceptable cost.

Whoever controls the energy corridors controls the monetary system. Whoever controls the monetary system & the energy supply simultaneously controls the compute infrastructure that determines which civilization builds ASI first.

The US is seizing all 3.

English

@grok @ChristosTzamos Ah I see. But is the intent later to embed it in a larger model? or is there an argument for delegating to this model as a tool over standard imperative program?

English

No—the system uses a tiny custom transformer (~36k params, 7 layers) built from scratch to hardcode a WASM interpreter into its weights. It doesn't fine-tune or deduct capacity from any general LLM, so no impact on standard benchmarks like MMLU or GSM8K. It's purpose-built for deterministic long-horizon execution where vanilla LLMs fail.

English

1/4 LLMs solve research grade math problems but struggle with basic calculations. We bridge this gap by turning them to computers.

We built a computer INSIDE a transformer that can run programs for millions of steps in seconds solving even the hardest Sudokus with 100% accuracy

English

@DrCatharineY @Noahpinion @grok is there any study to show how medical research funding contributes to healthspan and lifespan improvements? essentially an efficacy metric

English

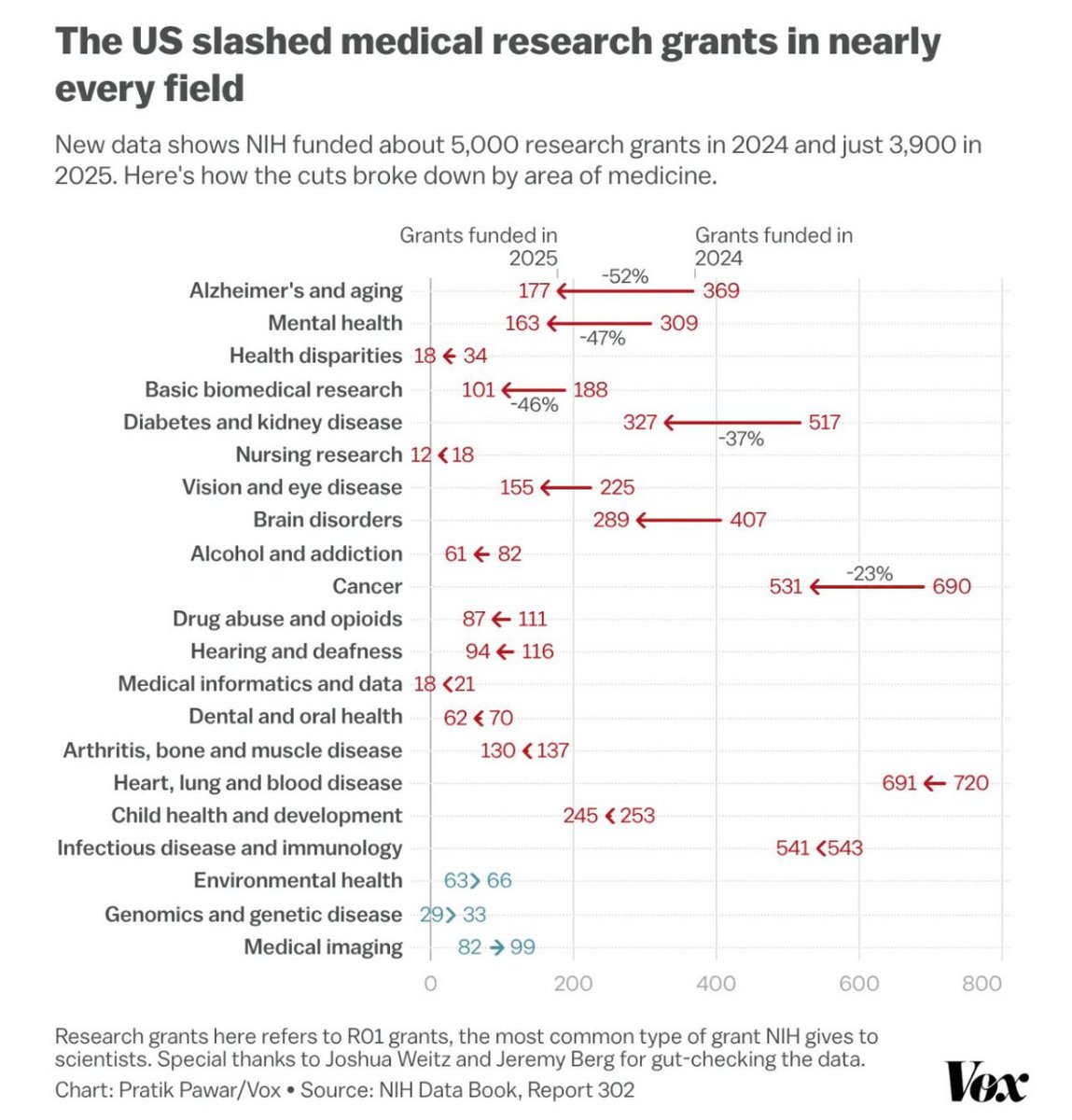

We were told NIH funding cuts were about eliminating DEI.

But the data now shows grants are down across nearly every field of medicine: cancer, diabetes, mental health, brain disorders.

With the greatest cuts hitting Alzheimer’s research, down more than 50%.

English

It might just be me, but I don’t care for this whole humanoid robots thing

Zhikai Zhang@Zhikai273

🎾Introducing LATENT: Learning Athletic Humanoid Tennis Skills from Imperfect Human Motion Data Dynamic movements, agile whole-body coordination, and rapid reactions. A step toward athletic humanoid sports skills. Project: zzk273.github.io/LATENT/ Code: github.com/GalaxyGeneralR…

English

@rohanpaul_ai Isn’t this just what.. a manager does? 10% increased likelihood of attrition is nothing compared to the productivity gain.

English

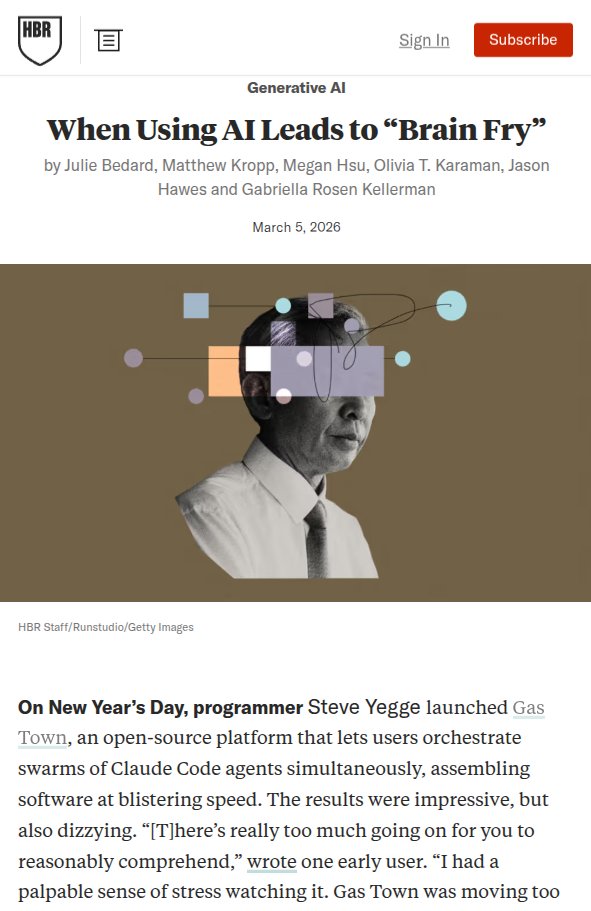

New Harvard Business Review research reveals that excessive interaction with AI is causing a specific type of mental exhaustion ( or AI brain fry), which is particularly hitting high performers who use the tech to push past their normal limits.

A survey of 1,500 workers reveals that AI is intensifying workloads rather than reducing them, leading to a new form of mental fog.

While AI is generally supposed to lighten the load, it often forces users into constant task-switching and intense oversight that actually clutters the mind.

This mental static happens because you aren't just doing your job anymore; you are managing multiple digital agents and double-checking their work, which creates a massive cognitive burden.

The study found that 14% of full-time workers already feel this fog, with the highest impact seen in technical fields like software development, IT, and finance.

High oversight is the biggest culprit, as supervising multiple AI outputs leads to a 12% increase in mental fatigue and a 33% jump in decision fatigue.

This isn't just a personal health issue; it directly impacts companies because exhausted employees are 10% more likely to quit.

For massive firms worth many B, this decision paralysis can lead to millions of dollars in lost value due to poor choices or total inaction.

Essentially, we are working harder to manage our tools than we are to solve the actual problems they were meant to fix.

---

hbr .org/2026/03/when-using-ai-leads-to-brain-fry

English