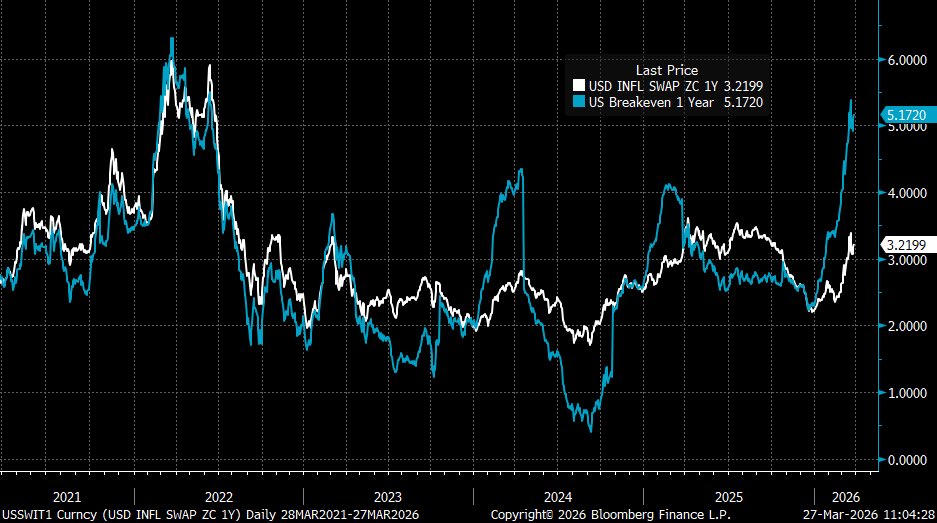

@LizThomasStrat If you use the April 2027 TIP breakeven and compare it to the 1Y inflation swap, the 'dislocation' disappears...

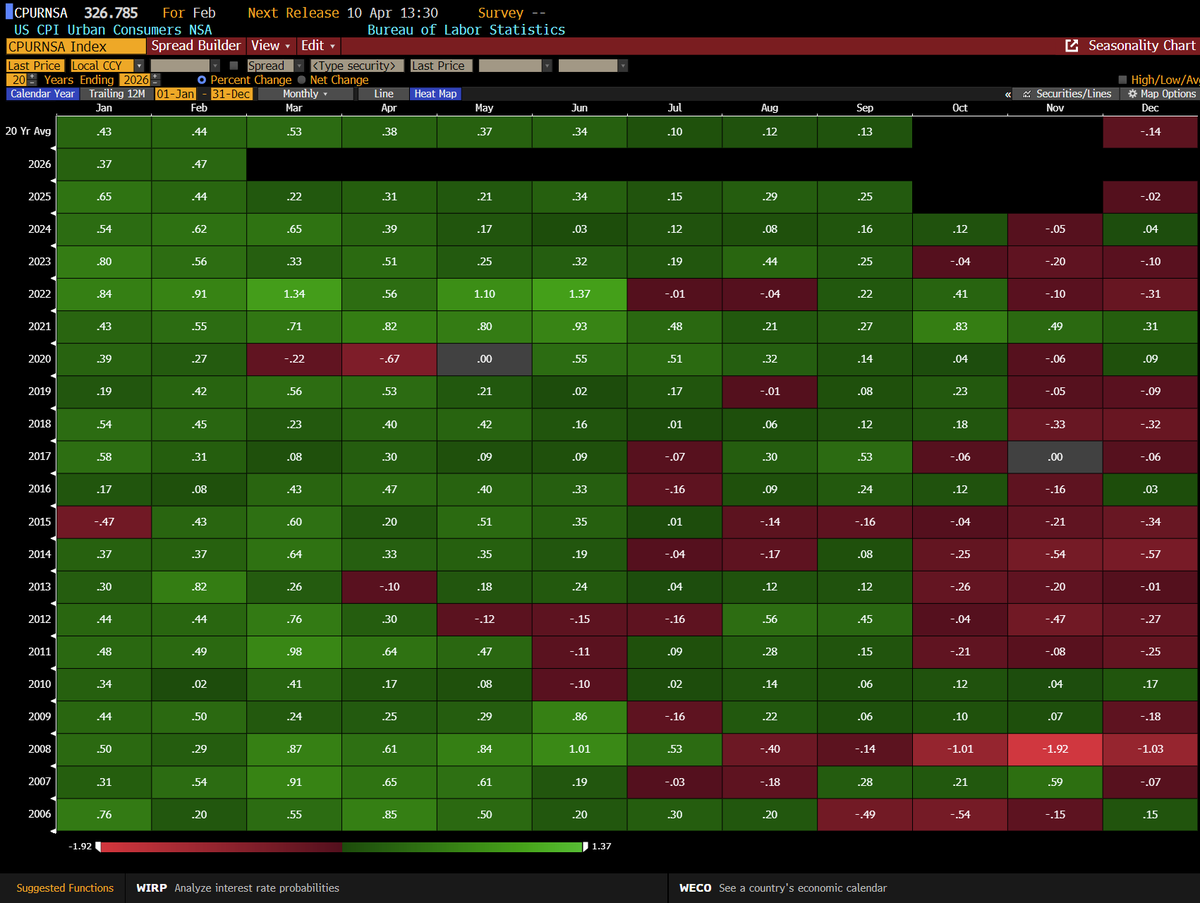

You are comparing apples to oranges, benchmarking a 7 months TIP against a 1y swap in a product where seasonality has a huge impact (see my prior comment above)

English