Sabitlenmiş Tweet

Everyone keeps saying 2025 was about US equities and AI.

I disagree.

The real story of the year was the value of money and how misleading it has become to measure everything in dollars.

In 2025, the USD weakened materially:

-0.3% vs JPY

-4% vs CNY

-12% vs EUR

-13% vs CHF

-39% vs gold

Gold, the only major non-fiat monetary asset and arguably the second global reserve currency, returned +65% in USD terms.

The S&P 500 returned +18% in USD.

Measured in gold terms? -28%.

Same asset. Same year. Completely different reality depending on the unit of account.

This is the part most investors still miss:

when your benchmark currency weakens, asset returns look better than they really are.

A US investor saw +18%:

A euro-based investor saw ~+4%.

A CHF-based investor ~+3%.

A gold-based investor lost almost a third of their purchasing power.

That’s not a rounding error, that’s a regime shift.

The same logic applies to bonds.

10Y USTs returned ~+9% in USD, but -34% in gold terms. Cash did even worse. No surprise foreign demand for USD bonds keeps deteriorating unless heavily hedged.

At the same time, capital quietly rotated away from the US:

– European equities outperformed US stocks by ~23%

– China by ~21%

– UK by ~19%

– Japan by ~10%

– EM equities returned ~34%

This wasn’t a global risk-on into the US.

It was diversification away from it.

Yes, US earnings grew (+12%), margins expanded, and multiples went up. But valuations are now stretched, credit spreads are tight, and expected equity returns sit around ~4.7%, barely above bond yields (~4.9%). The equity risk premium is thin.

In other words: a lot of future returns have already been pulled forward.

The Fed will likely keep easing to manage debt dynamics and avoid funding stress, which supports asset prices nominally, buuuut.... it also continues to erode the real value of money. The adjustment isn’t default. It’s dilution.

This is why looking at markets exclusively through a USD lens has become increasingly misleading.

For years now, the dollar has been a convenient benchmark, not a neutral one.

If you measure performance in a weakening unit of account, you confuse nominal gains with real wealth creation.

That’s the macro backdrop we’re in. Not a single bubble waiting to pop... but a slow monetary repricing where the benchmark itself is the problem.

Agus Capdevila@agusscapdevila

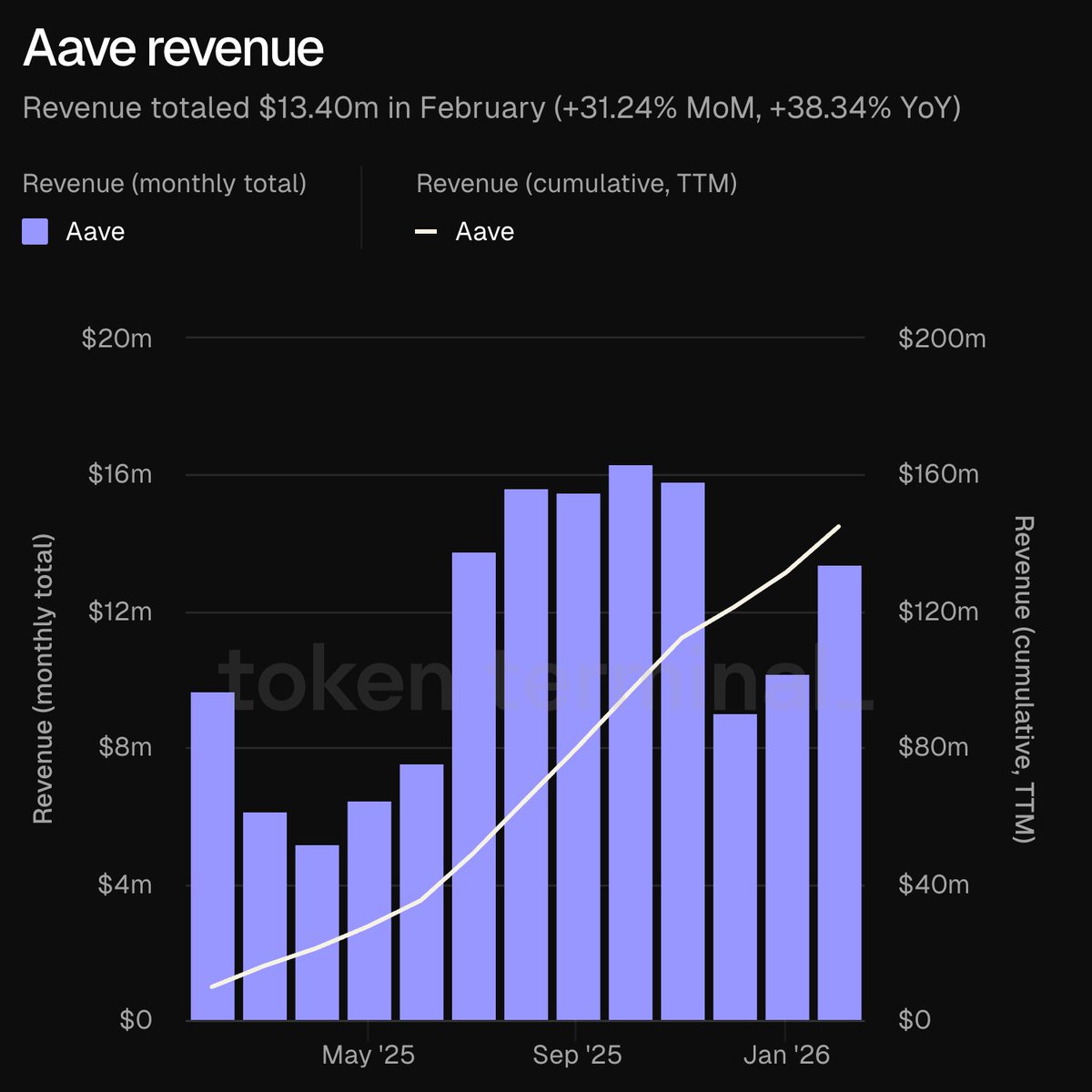

For portfolio managers focused exclusively on crypto: Beyond directional bets (which can work, depending on the asset), anyone running strategies anchored to USD-pegged stablecoins in a declining rate environment should rethink the benchmark. At these levels, USD stablecoin yield will likely underperform emerging markets, FX carry, and global macro opportunities. The opportunity cost is real. And it highlights what crypto still lacks today: a proper on-chain FX market. Who’s actually building it?

English