lambda retweetledi

The algorithm made me buy a Biltong dryer, and now I’m a very happy boy 🤤🥩

English

lambda

4.7K posts

Photonics value chain in 5 layers. The companies building AI’s optical backbone. $AXTI – Compound semiconductor substrates. Small, cyclical AI photonics supplier. $AAOI – Optical transceivers for AI data centers. High risk, high upside. $LITE – Diversified photonics. Stable, slower growth than AAOI. $ASML – Only maker of EUV lithography machines. Irreplaceable monopoly. $ONTO – Semiconductor inspection/metrology tools. Smaller KLAC alternative.

NEW: Exclusive Interview with Jaimin Rangwalla, Chief Investment Officer of Public Investments at Coatue In @coatuemgmt's Spring 2026 Investor Update, Jaimin walks through the unexpected winners of the AI cycle: memory, optical, CPUs, & the infrastructure layer quietly outperforming the Mag 7. We cover: - Why Coatue is "following the gigawatts" - Private companies breaking into the global top 25 pre-IPO (OpenAI, Anthropic, SpaceX) - Cash flow transferring from hyperscalers to AI infrastructure - The $12T funding engine behind the AI buildout - Sellers of shortage vs. buyers of shortage - The Token Economy - The CPU/GPU flip reshaping compute demand - Coatue's $6T+ AI market estimate - Agents launching agents / "1,000 analysts working 24/7" Read the full deck & watch the update replay below 𝐓𝐈𝐌𝐄𝐒𝐓𝐀𝐌𝐏𝐒 (00:00) Jaimin Rangwalla, CIO of Public Investments at Coatue (00:56) Inside Coatue HQ (02:48) Investor Update Kickoff (04:36) Mapping the AI Stack (06:02) Why Supply Stays Tight (07:03) How Jaimin's Became CIO (10:43) Private Giants vs Mag 7 (12:40) Market Breadth and Reordering (15:24) Where AI Revenue Comes From (17:04) Tokens and Economy (19:43) Agents Change Everything (21:58) OpenClaw Explained (24:49) Memory Demand Explosion (27:12) Architecture Shifts Ahead (27:24) Agents Gain Memory (27:58) CPU Demand Surge (28:38) CPU GPU Ratio Flip (30:21) Key Chip Players (30:45) Intel Comeback Thesis (31:41) Semis Go Mainstream (33:24) Nvidia Mania and GTC (33:59) Tracking Data Center Buildouts (35:21) Jobs Lost and Created (37:30) Sellers Versus Buyers (40:54) Optical Breakouts (41:27) Bottlenecks Everywhere (44:48) Sentiment Versus Fundamentals (47:10) Handling Volatility (49:17) Finding New Leaders (51:18) Trillion Dollar IPOs (52:48) Risks and Disruptions (55:00) Coatue Growth Story (55:58) Staying Curious to Win

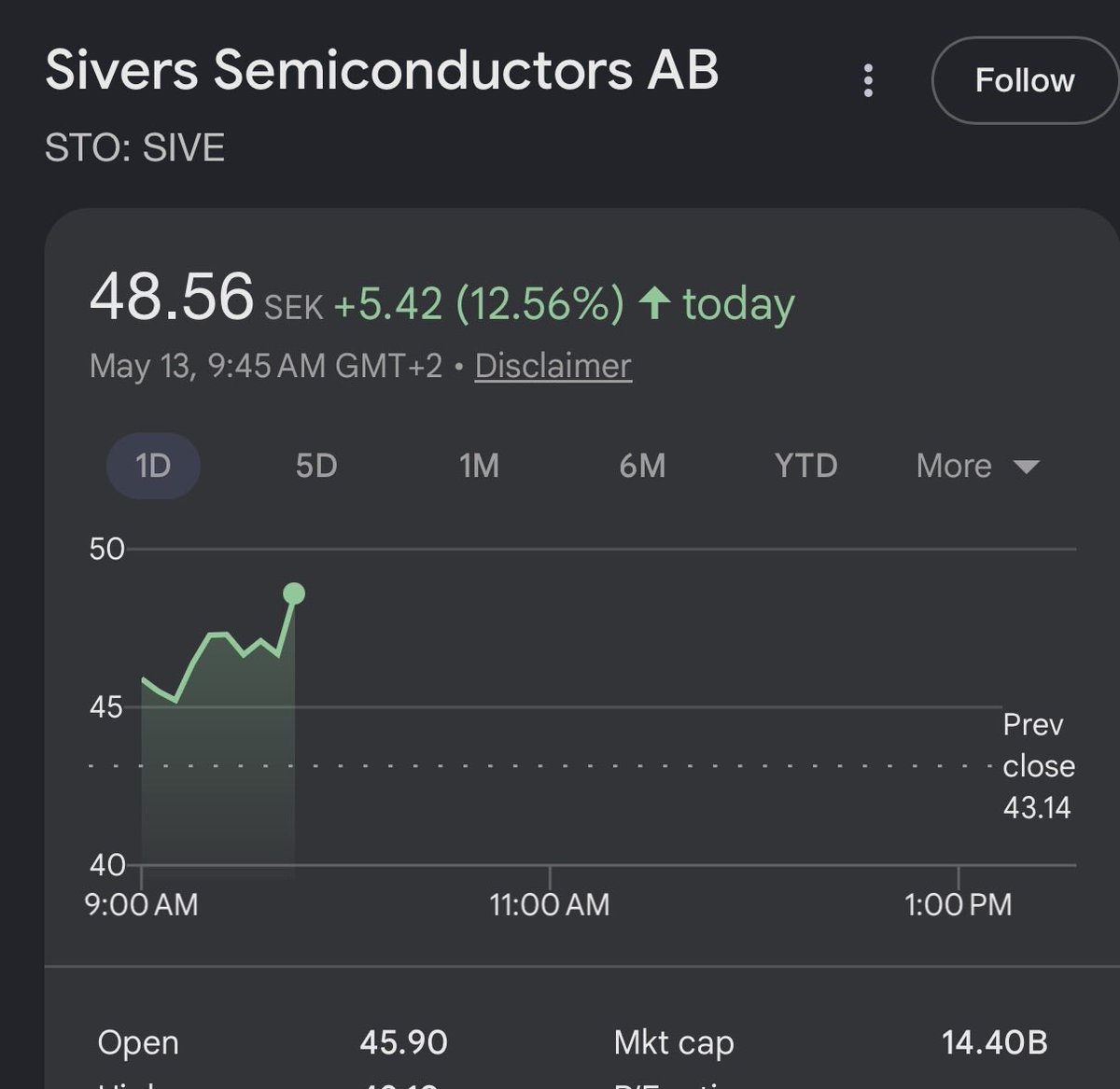

A breakdown of the photonics value chain and best positioned business: Layer 1: Materials & wafers • $GLW • $AXTI • $IQE • $AIXA • $AMS Layer 2: Core photonic devices • $IPGP • $COHR • $LITE • $LASR • $SIVE • Layer 3: Components & modules • $AAOI • $MTSI • $FN • $VIAV • $LPTH Layer 4: Systems & equipment • $ASML • $BESI • $ASM • $LPKF • $MKS Layer 5: Test, metrology & yield • $CAMT • $FORM • $AEHR • $ONTO • $VIAV

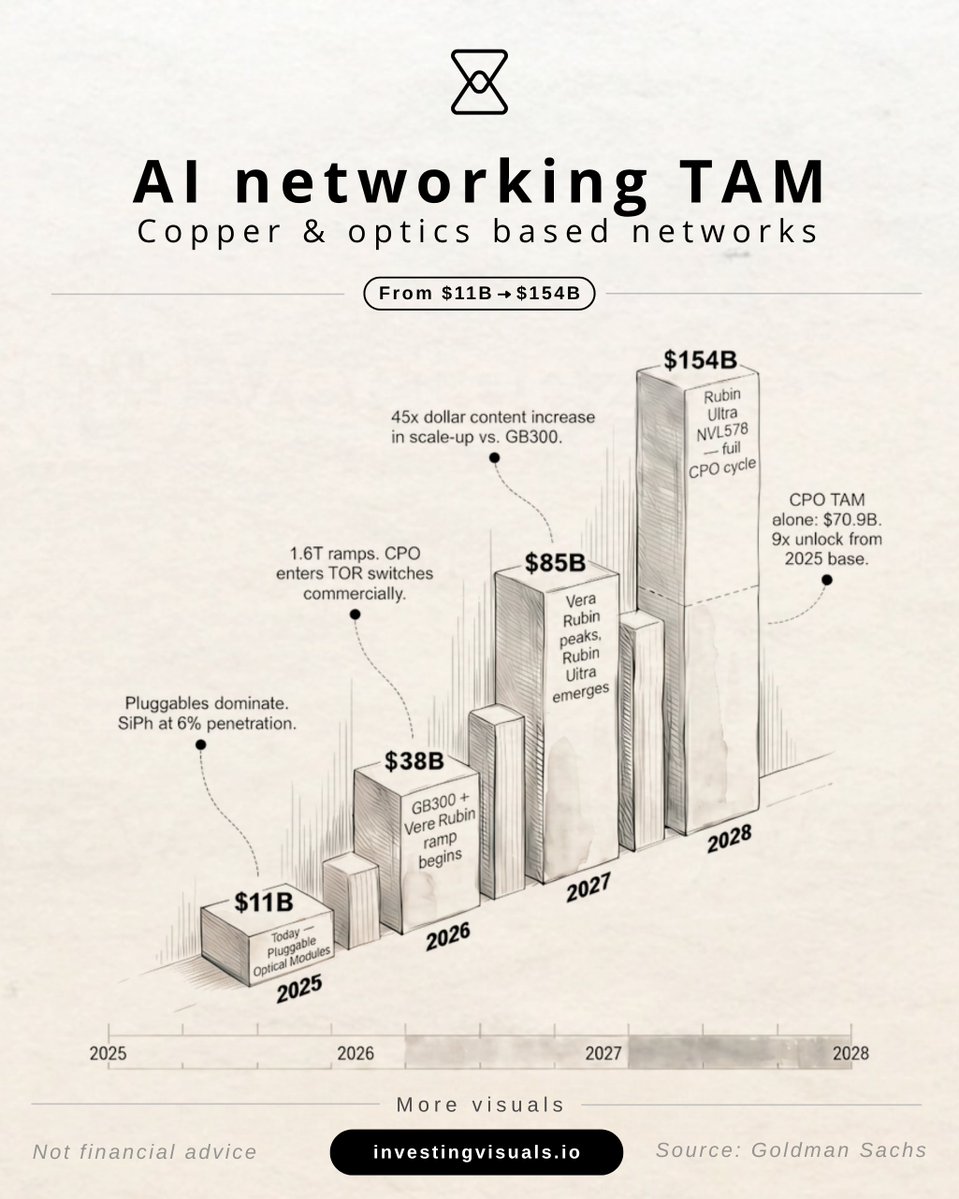

People wonder why I'm focusing on non-US markets recently. Why? CPO is my #1 thematic long. Markets don't know yet, the sudden paradigm shift in photonics... I was one of the only to frontrun the current supercycle in 2025 w/ $AAOI @ ~$30, $LITE ~$300s, and $AXTI at ~$13 on X.... With the actual receipts and thesis that others can't show. CPO goes from ~$0. To $91 Billion TAM opportunity. In the next 1 1/2 years from GS research. While overall optical market reaches $154B. Many players that had little exposure to the current photonics cycle at all: -> In Europe with high-end lasers design like $SIVE or $SOI with substrates. -> In Taiwan with Foci (3363), Nextronics (8147), Shunsin (6451) and others for optical components and foundries. -> In Japan with laser mass production, substrates, and chemicals. Are suddenly the new dominant players for CPO. As for US players, there's not much exposure. But the existing ones like $LITE, $COHR still get upside from CPO as that's their new growth vector. My contrarian thought process on current players: Is that most of their valuation is priced in huge legacy pluggable revenue that will inevitably face cannibalization over time, so re-rating potential is less unless someone uses leverage. A lot of these new purer play CPO names go from 0 to 100 extremely quickly one mass production starts H2 2026 for scale out (as a revenue bridge) into H2 2027 for scale up (massive growth driver). Markets usually price things in 8-12 months ahead of time too... I have high conviction thematically in my supply chain research despite any market volatility leading up until then.

Inside an AI server today, the GPUs talk to each other through copper cables and small pluggable optical modules. Starting in the second half of 2026, that wiring gets replaced by lasers built directly into the chip package (CPO). Goldman thinks the market for that goes from roughly 0 to $91 billion inside 18 months. That part the Serenity has right. What I’d slightly diverge on is who actually captures it. He says US names like Lumentum and Coherent are capped because they have to outgrow their own pluggable revenue getting cannibalized. True. The usual response is to buy the pure plays i Taiwan, Europe, and Japan that have no legacy book. The cleaner version of that argument is to keep going one layer up. The laser is the visible part. The wafer the laser sits on is the invisible part, and it has zero legacy revenue. CPO needs meaningfully more of that substrate per socket than plug-ins did. $SOI, which has the near-monopoly on silicon-on-insulator wafers for silicon photonics, still trades at a low multiple (attractive book value) while photonics peers trade at 5-8x sales. $AXT and $IQE are the same setup on the indium phosphide side. There is also the supply question. Nvidia spent roughly $4 billion between Coherent and Lumentum, which effectively locks up their laser capacity. Everybody else (AMD, Meta, Ayar, POET, Lightmatter) has to source elsewhere. Sivers is the small independent that catches that overflow. And the layer nobody talks about is the assembly itself. Co-packaging an optical engine onto a chip is hybrid bonding. BESI just printed a record order quarter at €269.7 million with hybrid-bonding unit orders more than doubled sequentially. The bottleneck for H2 2026 isn’t whether the optics work, it’s whether anyone in Taiwan can bond them onto the package fast enough. The date I would put on the calendar is November 27, 2026. That’s when China’s export-control suspension on gallium, germanium, and antimony expires, about 6 weeks before the H2 2027 scale-up window. If it gets re-imposed, the substrate names re-rate first, before anybody downstream sees a dollar of CPO revenue. Right gold rush. The interesting trade is one layer further up, where there is nothing to cannibalize and there is a date on the wall.

@aleabitoreddit So is $SIVE the best play for CPO