Sabitlenmiş Tweet

I've been fighting this whole time with my hands tied behind my back. Now I am unleashed.

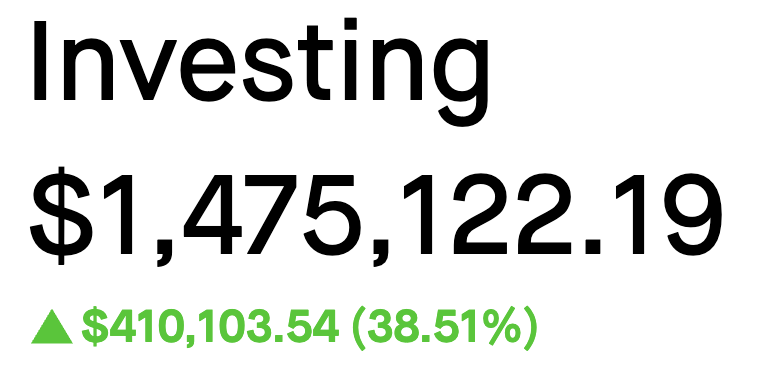

My mind, the very thing they mocked, just built a public portfolio worth $1.475 million with my

company valued over $50 million.

You're not just going to see my brain power. You're going to feel it rumble through the ground

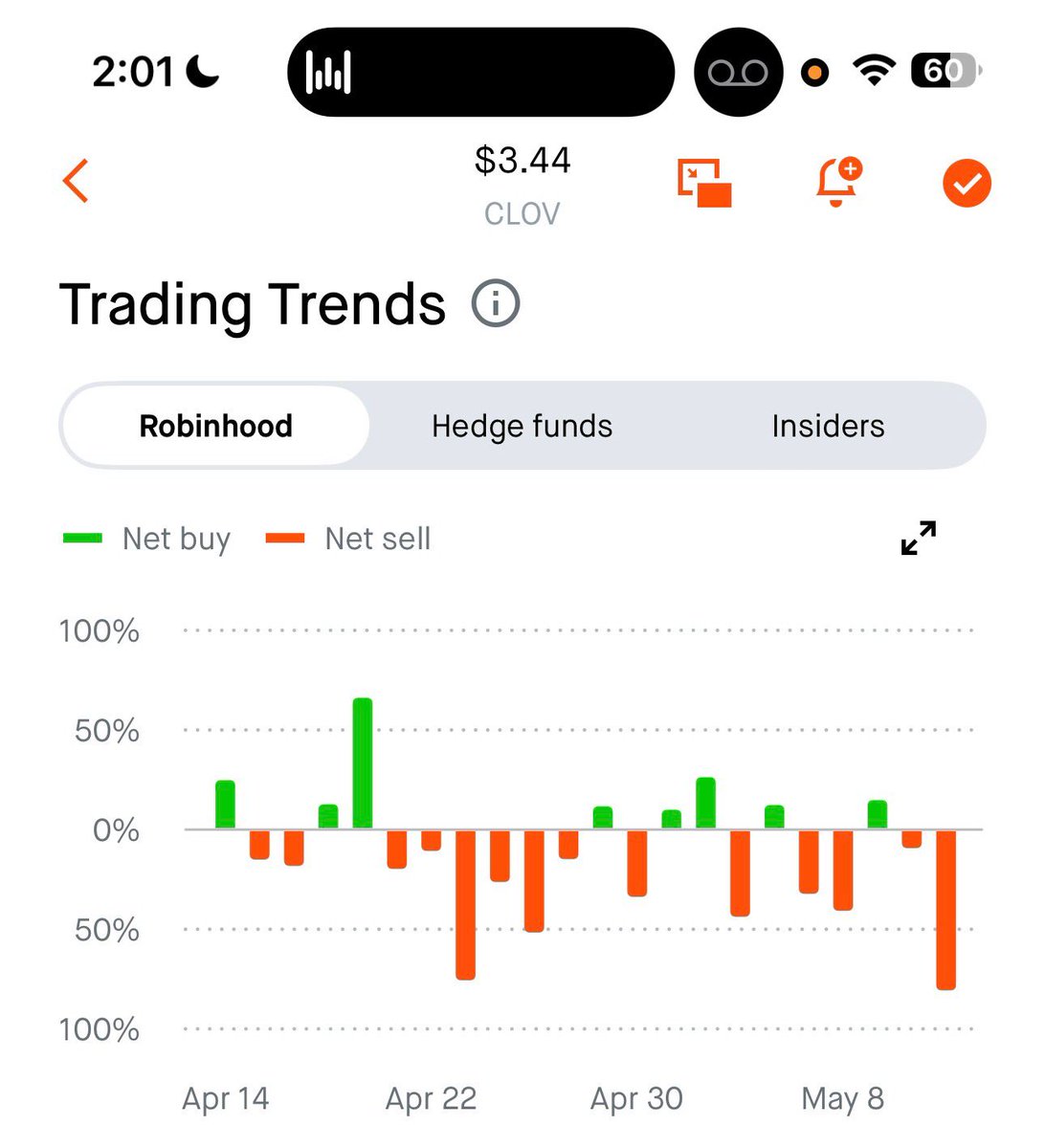

beneath your feet. $CLOV $OPEN $SOFI

English