Sabitlenmiş Tweet

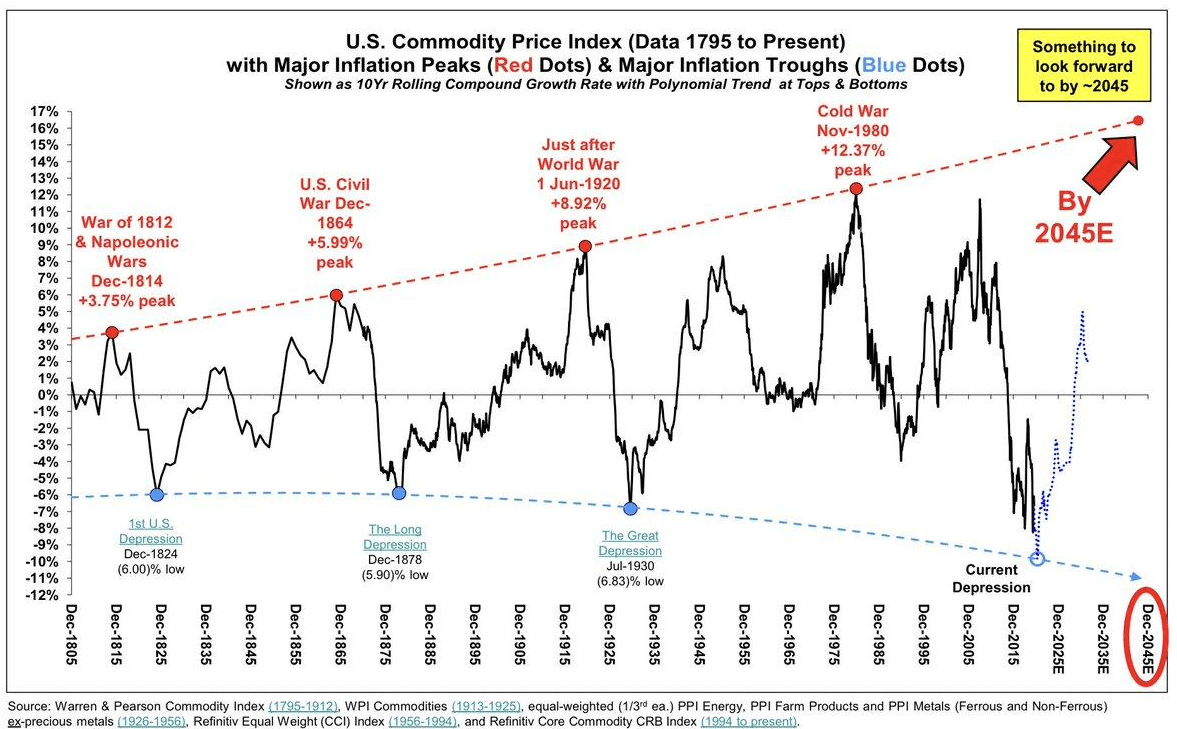

A mega🧵on all the Screeners and Dashboards I have built so far. These will help you pick stocks for short to medium term trading. If you like them then please retweet and help others too.

English

Apurva Sheth, CMT

1.1K posts

@apurvansheth

I help investors and traders by bringing actionable insights and strategies to take the right decisions in market.

#MarketsWithBS | Value of gold imports rose in FY26 even as volumes fell. @apurvansheth of Samco explains why higher #gold duty may not curb demand and why fuel price hikes could better protect #India's fiscal position. mybs.in/2g6BHmF

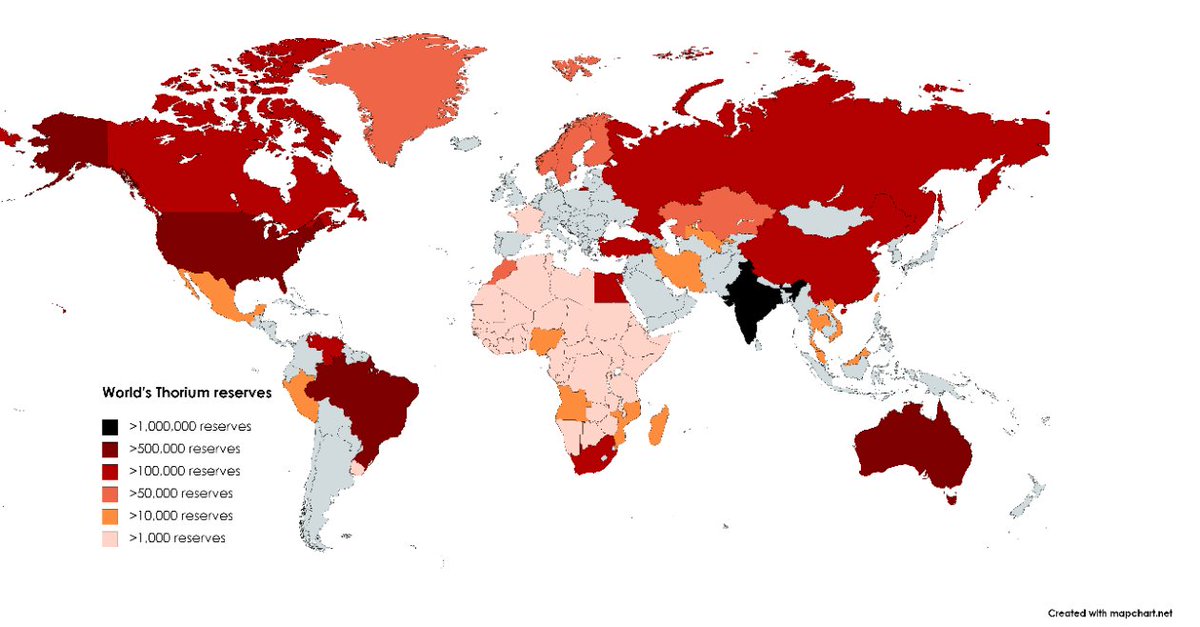

Today, India takes a defining step in its civil nuclear journey, advancing the second stage of its nuclear programme. The indigenously designed and built Prototype Fast Breeder Reactor at Kalpakkam has attained criticality. This advanced reactor, capable of producing more fuel than it consumes, reflects the depth of our scientific capability and the strength of our engineering enterprise. It is a decisive step towards harnessing our vast thorium reserves in the third stage of the programme. A proud moment for India. Congratulations to our scientists and engineers.

The Iran War Isn’t About Nuclear Weapons—It’s About Saving America’s Collapsing Empire 🐇The Rabbit Hole goes much deeper; the war with Iran isn’t about “terrorism” or “nukes.” It’s about securing a trade corridor — IMEC — that was designed to reroute global supply chains around China, choke China of energy, install India as the new workshop, and lock the Middle East into a US-Israel controlled infrastructure network The article archive.is/2026.03.20-191… exposes the geopolitical plumbing, mapping the "Big Picture" that most Western analysts miss because they’re too busy counting missiles, troop deployments or chasing news cycles👇 The bombs falling on Iran are not about nuclear weapons. They are about a trade corridor called IMEC—the India‑Middle East‑Europe Economic Corridor—and the infrastructure that will determine who controls global energy, data, and supply chains for the next generation IMEC as Imperial Infrastructure—and Why It Needs War The India-Middle East-Europe Economic Corridor is not merely an alternative to China's Belt and Road Initiative (BRI). It is a replacement architecture designed to intercept the natural geography of Eurasian trade and force flows through Western-controlled chokepoints Consider the geography: Iran sits at the intersection of the International North-South Transport Corridor (linking Russia to India), the Middle Corridor (China-Central Asia-Turkey-EU), and direct China-Iran rail and energy links. These routes threaten to bypass both the dollar system and American military oversight IMEC solves this by creating a parallel network running through Israeli ports, UAE logistics hubs, and Indian manufacturing—each node controlled by US allies or dependent on American security guarantees. Jared Kushner's $4.6 billion Affinity Partners fund exemplifies the financialization of this strategy: Gulf capital flows through Israeli tech and Indian labor into European markets, generating returns while cementing political alignment The "Abraham Accords" that enabled this were never peace deals; they were investment-grade risk instruments that transformed occupied territories into viable assets for international capital. The "technocratic reconstruction" of Gaza fits this model. A genocidal war creates the vacancy; "development" fills it with investor-controlled zones where Palestinian sovereignty is replaced by special economic areas governed by technocratic mandates. This is not reconstruction—it is real estate colonialism with ESG branding But IMEC has a fatal vulnerability: its eastern sea lane runs through the Strait of Hormuz, a 33‑km bottleneck that Iran can close at will. Without neutralizing Iran, the corridor cannot function The Sequence: Abraham Accords → Iran War → Hormuz crisis → Gaza Reconstruction Operation 'Epstein Fury', launched February 28, 2026, was not a spontaneous act of aggression. It was the military clearance phase of a pre‑designed infrastructure plan. The Abraham Accords (brokered by Jared Kushner in 2020) — between Israel and the Gulf states — created the political coalition. The war on Iran is an attempt to clear the military chokepoint. IMEC is the commercial payoff. These are not separate events. They are a sequenced strategy. Kushner has already planned the reconstruction through Trump's "Board of Peace": his “technocratic administration” for Gaza—a Dubai‑like enclave with a new port and airport—turns that territory into a Mediterranean extension of IMEC. He designed the diplomatic framework, raised $3.5 billion from Gulf sovereign wealth funds for his own firm, and now oversees the governance of the corridor’s key node. Policy, finance, and war in one seamless loop. India’s Role—and Its Trap Indian Prime Minister Narendra Modi's February 2026 address to the Israeli Knesset—where he termed Israel the "fatherland" and India the "motherland"—occurred mere days before coordinated strikes on Iran. The familial metaphor reveals the emerging hierarchy: Israel provides the security umbrella and Western-approved gateway; India provides the labor pool and low-cost manufacturing India is IMEC’s eastern anchor. Adani Ports owns Haifa (Israel) and is developing Vadhavan on India’s west coast. New Delhi is being positioned as the low‑cost manufacturing hub to replace China in Western supply chains. But the US has signaled it will not grant India the same trade and technology access it once gave China. Washington views its post‑Cold War engagement with Beijing as a mistake that created a rival. So India gets the geopolitical risk—alignment with Israel, proximity to a war zone—without the structural economic lift that built China’s middle class What if the Israeli-U.S. led coalition wins its war of aggression? From Washington’s viewpoint, “winning” the war against Iran and locking in IMEC would tick several boxes at once. It would weaken a key energy supplier to China, constrain a major BRICS‑aligned player, and reroute Gulf exports through U.S.-aligned infrastructure where financing, insurance, and standards are dollar‑denominated. That helps preserve the petrodollar, fragments rivals’ energy sovereignty, and deepens allied dependence by turning energy security into a corridor privilege the U.S. can price and police In that world, BRICS+ finds it harder to build a parallel, yuan‑ or local‑currency energy system because the key pipes and ports are wired into Western banks and rules. Europe, already cut off from cheap Russian gas, becomes even more locked into U.S.-approved Middle Eastern routes—paying monopoly rents in an environment of engineered scarcity and permanent “security risk.” China faces higher energy costs, rising production costs, and more fragile Gulf supply lines just as it battles domestic economic headwinds and tries to fund its own tech and industrial upgrades If that’s the “U.S. wins” scenario, the “U.S. loses” version looks very different The obvious consequences of a US loss are immediate and transformative: First, IMEC dies overnight. A resilient Iran that keeps enough military and political capacity to threaten shipping or strike regional infrastructure turns IMEC from an instrument of control into an instrument of risk. Investors see a corridor sitting inside a permanent war zone. Insurance premiums spike, ships reroute, and the picture of a clean, secure alternative to China‑linked routes starts to look like another over‑militarized promise that never delivers, rendering the project uninvestable and commercially irrelevant. Second, the petrodollar’s collapse will accelerate dramatically: a US military defeat will prove it can no longer guarantee security for Gulf states, which will double down on de-dollarization, trade oil in yuan and other non-dollar currencies, and deepen ties with BRICS+ For BRICS and the wider Global South, that outcome—costly in the short run—actually strengthens the long‑term case for multipolarity. It accelerates efforts to diversify away from U.S. chokepoints: more Russian pipelines and seaborne flows to Asia, deeper China–Iran and China–Gulf energy deals, more experimentation with non‑dollar settlements and payment systems. IMEC’s failure to become a stable empire‑corridor becomes exhibit A in why over‑reliance on U.S.-controlled infrastructure is a strategic risk, not an insurance policy Europe, meanwhile, gets squeezed either way A decisive U.S. victory binds it deeper into a U.S.-centric system where energy and sanctions policy are made in Washington—Europe pays the bill. A messy stalemate or visible U.S. failure forces European capitals to confront an awkward question: keep doubling down on U.S. corridor bets that can’t be secured, or cautiously reopen the door to diversified connectivity—including selective engagement with BRI and BRICS energy diplomacy For China, a failed U.S. attempt to use Iran and IMEC as twin levers is painful but survivable. Beijing’s diversification—Russian oil and gas, African and Latin American supplies, strategic reserves, domestic renewables—was built precisely for this kind of shock. It would still face higher prices and tighter margins, but it would not be structurally cut off. And every barrel that ends up traded outside the dollar, every workaround built under pressure, chips away at the very monetary power Washington is trying to defend Put simply: if Washington wins big, IMEC becomes the hardware of a renewed, harder U.S. empire—petrodollar cemented, BRICS fragmented, China squeezed. If it doesn’t, the war over Iran and the corridor won’t just expose U.S. limits; it will push the Global South faster toward a world where no single power can redraw the energy map alone For the rest of us, the immediate question is whose infrastructure will survive it and whether Israel or the U.S. will escalate to the use of nuclear weapons

Blue collar is the new white collar… but I also know that you will waste 4 yours of your life to do that useless degree which is good for hanging on the wall only.. of course you will also be $250000 in student debt by the time you get out of college.