Arx

161 posts

Arx

@arx_void

DeFi product builder /// Simplifying complex mechanics so teams ship better protocols

EVM Katılım Şubat 2026

279 Takip Edilen31 Takipçiler

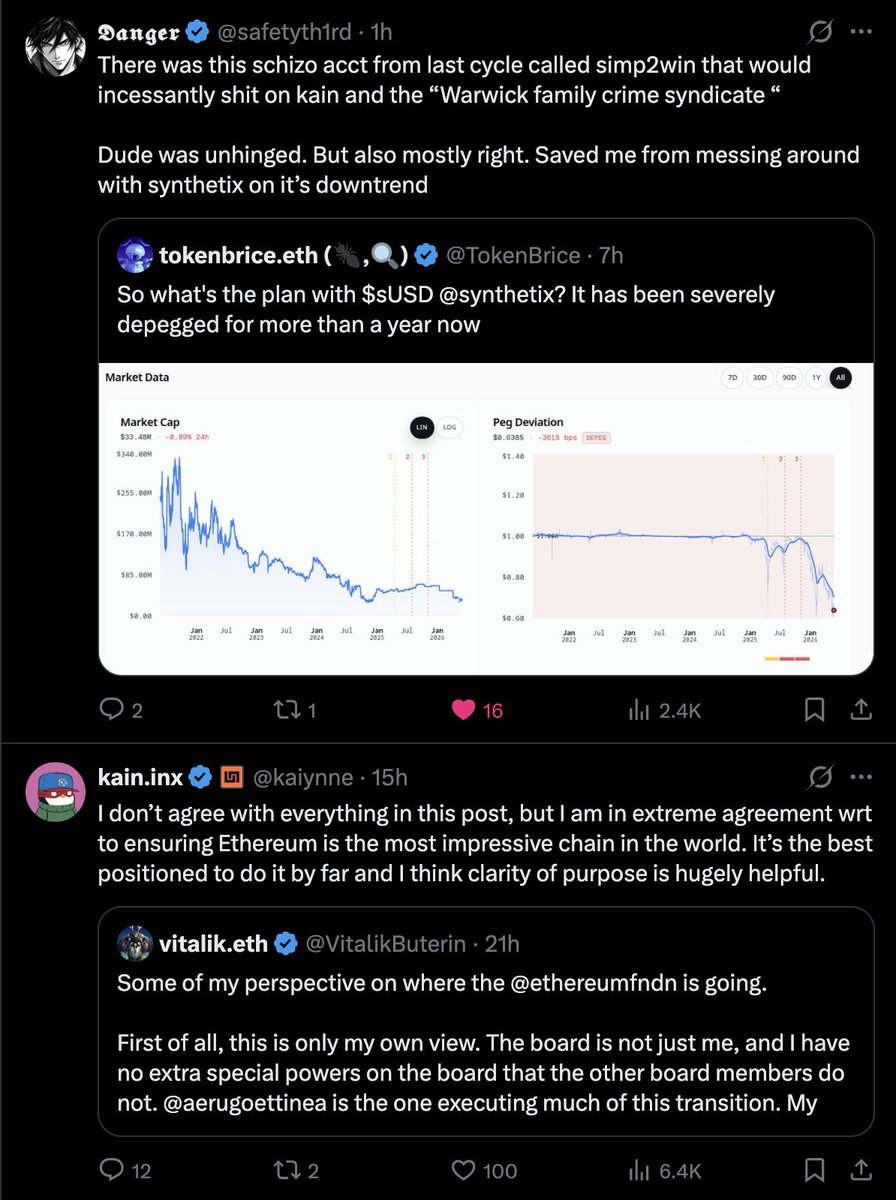

There was this schizo acct from last cycle called simp2win that would incessantly shit on kain and the “Warwick family crime syndicate “

Dude was unhinged. But also mostly right. Saved me from messing around with synthetix on it’s downtrend

tokenbrice.eth (🐜,🔍)@TokenBrice

So what's the plan with $sUSD @synthetix? It has been severely depegged for more than a year now

English

The worst thing you can do as a trader is think you missed a trade.

You will have an infinite amount of trades ahead of you in your life if you just start fresh everyday.

hyperliquid:native was at $0.01 equivalent, people were mad that they “missed the trade” at $4… and again at $20.

English

@flipdazed right now yes, but it's not hard capped and there's mechanisms to mint more if there's consensus

English

@arx_void Ah that’s fair - I thought ETH was largely flat in supply though ?

English

What could be wrong about this?

tldr; ETH will grow by at least 40x.

100B–1T transactions daily in all finance

Will be 1-5T in the next 5-10 years.

Eth does ~2.5M tx/day today.

Gas prices have a floor of 10-100x where they are today.

Upper limit is 200,000x todays revenue (theoretical limit based on revenue - impossible with mkt cap)

Lower limit market penetration is 1%, 1T txns, 100x decrease in gas.

Lower limit is 40x within 10 years.

ETH must hit ATH 80k on a revenue basis alone.

I think this ties out as I'd struggle to see ETH market cap < $10Tr if blockchain is adopted for all global financial transactions in the next ten years.

English

also trading streaks for 'APY'

Haseeb >|<@hosseeb

So with the new Clarity Act compromise, passive stablecoin yield is banned, but "activity-based rewards" are okay. I.e., no more yield for holding, only for doing. The cheapest possible "doing" is tapping a button. I'm calling it now: tap-to-earn is gonna make a comeback.

English

So with the new Clarity Act compromise, passive stablecoin yield is banned, but "activity-based rewards" are okay.

I.e., no more yield for holding, only for doing.

The cheapest possible "doing" is tapping a button.

I'm calling it now: tap-to-earn is gonna make a comeback.

Laura Shin@laurashin

The banking lobby wanted a full ban on stablecoin yield. They lost. Activity based rewards on USDC survived the Clarity Act, and Coinbase walked out with the most valuable customer acquisition tool in fintech still intact. 💰 ~ Alex views x.com/i/broadcasts/1…

English

@sui414 did you write this on the plane too lol

x.com/sui414/status/…

danning@sui414

On a 6h flight from NYC to SF Literally everyone in this plane (inclu. myself) is talking to ChatGPT or Gemini Guy’s screen in front of me “the hard truth about your gf’s wiring” Guy next to me “simulate the brackets for this prediction market bet”

English

@StaniKulechov yes but that's also because in DeFi it's all overcollateralized

English

One of the biggest mistakes in valuing DeFi lending protocols is using TVL as the primary metric.

TVL measures net collateral. It does not measure lending activity.

Compare Aave vs SoFi at the end of 2025:

Aave

~$52B supplied

~$22B active loans (the loan book)

~$700M+ borrowing interest flows

~$150M retained by the DAO

SoFi

~$37.5B deposits

~$38B loan book

~$1.8B lending revenue (interest earned)

~$481M net income

In TradFi:

deposits are liabilities / cost of capital

loans are the earning assets

lenders are analyzed on loan books, interest income, spreads, and asset growth

But in DeFi, the market mostly looks at TVL and DAO-retained fees.

That’s like valuing a bank only on net interest spread while ignoring the size of the loan book and gross interest flows.

Under traditional financial accounting frameworks, Aave looks far closer to a +$700M lending business than a $150M revenue protocol to be comparable (without counting equity).

TVL is not the revenue basis for lending protocols.

Loan books and interest flows are.

PaperImperium@ImperiumPaper

A major unforced error in crypto is treating technical dashboards as financial dashboards. Nowhere is this as obvious as with TVL of lending protocols. TVL is NOT a substitute for accounting! Let’s look at TVL defined as “Value of all coins held in smart contracts of the protocol”, and how it would treat a bank with the following balance sheet: Deposits (a liability): $100m Loans (an asset): $80m Reserves (an asset): $20m Equity: $10m The TVL of this simplified balance sheet would show up as: $100m deposits - $80m loans + $10m equity = $30m TVL Does that feel accurate to you? It should not, because it structurally undercounts economic activity. In fact, TVL - a technical metric - is treating the bank’s largest asset (its loan book) as a liability and largest liability (its deposits) as an asset! The problem is one of using the wrong tool for the job. TVL counts how many tokens are in a smart contract or group of affiliated smart contracts. That’s it. In its most simple form, TVL is mostly just counting the reserve ratio of the bank (or lending protocol). TVL is not a substitute for actual accounting, and people need to understand this. A deposit on Aave/Morpho/SparkLend/Compound/Euler/Curvance is a liability to that protocol or pool. You could put $1 trillion in deposits onto one of those platforms and TVL would become $1 trillion. But that’s not an indication of economic activity! Now imagine $999.999 billion of that got lent out. TVL has crashed from $1 trillion to $1 million. Looks bad on a chart, right? But now we’re seeing economic activity! There is a reason why TVL is not used outside of crypto - it is a technical metric, not a financial one, and any overlap is coincidental and concentrated in very basic protocols like DEXes.

English

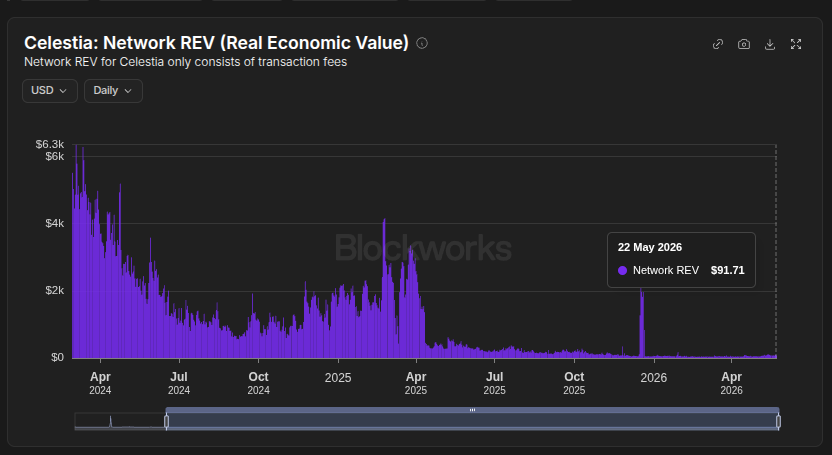

Talking about active users on a DA layer doesn’t make sense imo

If you want to fud properly you can show Celestia’s revenue which is actually generating about as much as a guy working a minimum wage job

Maybe we all deserve to raise $156M

Stacy Muur@stacy_muur

Celestia, a protocol that raised $156 million in funding, now has less than 1,000 daily active users. Incredible.

English

anyone from palantir can explain how this works in practice?

Like, how does someone go along with what they know is a bad decision, knowing they might get blamed for it?

Tropical Value@tropicalvalue

English

sending $100M wire costs $0-15

sending $100M of the largest stables costs $30-100k (unless your recipient keeps it in stables)

for true stable adoption, fungibility with dollars >>> exit fees from leaving ecosystem

it’s simple logic

English

Ethereum txs reaching ATH due to address poisoning attacks.

Every time the gas limit is raised and tx fees go down, it costs less to 'dust' a wallet.

For example, after Fusaka, sub-$0.01 dust txs increased by 600%.

Etherscan reported that Ethereum address poisoning succeeds about 0.01% of the time: 1 in 10,000 transfers tricks a user into sending funds to an attacker.

Actually, Ethereum might benefit from RAISING fees as they it makes address poisoning attacks more expensive and it burns more $ETH.

Emperor Osmo 🐂 🎯@Flowslikeosmo

Ethereum L1 transactions just hit an all-time high. Fees are at an all-time low. The Glamsterdam upgrade cut fees by 78%, and the chain absorbed the cost without losing users. 32.4% of all ETH is now staked. Also, an all-time high. Everyone continues to write off $ETH, while the fundamentals have never been stronger. Data: @tokenterminal

English

I'm fairly well-known as a buyback truther.

The issue I have with buybacks is not the outcome, DoubleZero has a burn and 0% inflation. Clearly, the outcome is something I think is net good.

But the mechanism has problems. It's discretionary for whoever controls the wallet receiving fees. This discretionary nature is a distortion of markets when it's not hard coded.

The idea of reducing supply above the rate of inflation is, quite obviously, a good idea though.

vukan (blkn/acc)@vukan0x

“buybacks are useless”

English

@yaroslavwr_ this is more regulation than philosophy imo. it'll take a while for this to fully happen

English