Rishi

2.4K posts

Rishi

@athena_ug

Believer of Democratization of knowledge! Beware : Money, Tweets & interpretations are personal here.

Mumbai, India Katılım Şubat 2022

572 Takip Edilen442 Takipçiler

@LearningEleven Terminal value of ICE 2/3/4W is very low because it being a sunset sector (of course not immediately), do you feel sedemac will comand high PE going ahead? Any plans of offerings to EV segment in future sir?

English

Timepass talk on Sunday

1. India’s Maritime Push: A Long-Term Story, Not an Easy Trade

India currently accounts for less than 1% of global ship-owning capacity, and the country pays an estimated $75–90 billion annually to foreign shipping companies as freight. This outflow is significant, broadly comparable in scale to India’s annual defence expenditure.

This imbalance exists because only ~5% of India’s EXIM cargo is carried on Indian-flagged vessels, while the remaining ~95% is handled by foreign fleets.

To address this structural gap, India has set an ambitious target to break into the top five ship-owning nations by 2047, which, as per government estimates, would require investments of around $350–400 billion over time.

As an initial step:

India added ~90 vessels to its fleet in FY26, including both coastal and overseas vessels.

The government is planning to float tenders for ~60+ vessels in FY27, with a portion already initiated.

The Ministry has also aggregated long-term domestic demand of ~400+ vessels by FY42, indicating sustained visibility for the sector.

Policy intent is clearly shifting toward indigenization of shipbuilding:

“Our effort is that these orders should go to domestic players. Currently, large vessels like VLGCs and VLCCs are not manufactured in India. We aim to develop such capabilities domestically and reduce dependence on foreign shipyards.” - Ministry of Ports (senior official)

That said, execution remains the key monitorable, especially in building capabilities for complex vessels (like VLCCs/VLGCs), where India currently has limited presence. We have to rely on MNC JVs.

Bottom line:

The direction is clear, India wants to reduce freight outflows, build domestic capacity, and increase fleet ownership. This creates a multi-year opportunity, though it will likely play out gradually rather than in a straight line.

Key investable buckets:

Shipbuilding yards – e.g., Cochin Shipyard, Mazagon Dock Shipbuilders Limited, Swan could be the wildcard!

Ancillary / repair ecosystem – e.g., Knowledge Marine & Engineering Works

Shipping / fleet operators – e.g., Shipping Corporation of India

Don't forget: Despite strong tailwinds, shipbuilding is a non-linear business, marked by long gestation, lumpy revenues, margin volatility, capacity and execution constraints, policy-to-reality gaps, working capital intensity, and global cyclicality, making timing and expectations critical.

2. Anlon Technology

Imagine a fire emergency on the 32nd floor of a luxury high-rise or a sudden power failure in a crowded mega-mall. In such moments, the reliability of specialized engineering is not just important, it’s critical to life and safety.

That’s where Anlon Technology Solutions comes into play.

A couple of years ago, this was the talk of SME-town, a company transitioning from a commission-based model to manufacturing. As the SME segment went through its rough patch, this company inevitably felt the impact as well.

Anlon provides high-precision firefighting, rescue, and critical infrastructure equipment that keeps India’s increasingly dense urban ecosystems safe and operational. With the commissioning of its Doddaballapur facility, the company is transitioning from a service-led model to a more manufacturing- and assembly-driven business, positioning itself as a meaningful participant in India’s infrastructure and “Make in India” push.

What the company does

Anlon is a niche player manufacturing and assembling:

Advanced runway rubber removal machines

Firefighting and rescue vehicles

Specialized infrastructure equipment

Its clientele includes: Airports (~80% of revenues) and Municipalities, refineries, and others (~20%)

It's a natural beneficiary of: Airport expansion, Urban infrastructure growth and “Make in India” push

Revenue mix

By product - Firefighting equipment: 65–70% Runway rubber removal machines: 25–30%

By business model (evolving) - Direct sales (manufactured/assembled): 40–45% and Spare parts + AMC: 35–45%

Business evolution (clear shift underway)

Mar’24: Commission (5–15%), AMC (30–40%), Spare parts (40–50%)

H1 FY25: Commission (5–15%), AMC (35–40%), Spare parts (35–40%), Direct sales (10–15%)

H2 FY25: Commission (5–10%), AMC (30–35%), Spare parts (25–30%), Direct sales (25–35%)

H1 FY26: Commission (5–10%), AMC (20–25%), Spare parts (15–20%), Direct sales (45–55%)

Debt-free balance sheet, Niche, specialized segment with high technical barriers

Key concerns / risks

Working capital intensive (high inventory + receivable days)

Cash flow conversion needs improvement

Low float (~1,200 shareholders) → potential liquidity concerns

3. SEDEMAC: Powering ISG Intelligence Behind India’s Silent Start Engines

So what exactly is ISG?

ISG stands for Integrated Starter Generator. Traditionally, a petrol engine needs two separate electrical machines to function.

A Starter Motor: Used only for a few seconds to "crank" the engine and get it running.

An Alternator (Generator): Once the engine is running, this spins to charge the battery and power the lights/electronics.

An ISG combines these two into one single unit mounted directly on the engine’s crankshaft. It acts as a motor to start the engine and then seamlessly switches to being a generator once you're moving.

If you’ve noticed newer scooters (like TVS Jupiter) starting instantly without the typical “kr-kr-kr” sound, that’s ISG in action.

To make an ISG work, a computer needs to know the exact position of the motor's internal parts (the rotor) to send electricity at the right micro-second. Most companies (Bosch, Continental) use physical sensors (called Hall sensors) inside the engine to track this.

Sensors are prone to breaking due to engine heat and oil. Sedemac wrote a complex mathematical algorithm that "guesses" the position by reading electrical feedback instead of using a physical sensor.

That's deep tech!

Sedemac Mechatronics is a specialist in the design, manufacture and supply of advanced control‑intensive Electronic Control Units (ECUs) for mobility and industrial applications. Its product portfolio consists of Integrated Starter Generator (ISG) ECU, Electronic Fuel Injection (EFI) ECU, ISG+EFI ECU, EV motor controllers, and Genset Control Units. The company commands 35% market share in India’s ISG ECU segment for 2W/3W vehicles and 75–77% share in the Indian genset controller market for 9MFY26.

Company has 12 granted patents and 11 more in the approval stage. They spend abut 7-10% of their revenues on R&D.

Its key clientele includes TVS Motor, Hero MotoCorp, Bajaj Auto, Mahindra, Kirloskar Oil Engines, and Generac.

Primary risk is, The Top 10 customers contributed 98.7% of revenue in 9MFY26 and TVS Motor alone is responsible for 75-80% of revenues!

Though they have electric vehicle (EV) offerings, it's largely tied to products for ICE vehicles.

While FY26 results are yet to be out, the recent business update indicates that sales of control-intensive ECUs grew ~60% YoY, pointing to a strong Q4 performance.

FY25 PAT was 47cr, so, if I assume 80cr PAT for FY26, it is still at 100 P/E! It will probably remain like that!

4. Acutaas Chemicals - Peakness of margins or middle of an incredible story!?

Acutaas has reported exceptional numbers, with EBITDA margins expanding from 23% in FY25 to 36% in FY26, a jump that few would have anticipated. Even more striking is the recent trajectory: margins over the last three quarters have come in at 31%, 38%, and 42%, highlighting a sharp improvement in operating leverage and business mix.

Driven by strong traction in the CDMO segment, the Advanced Pharmaceutical Intermediates business delivered 44% YoY growth in Q4. While one product is already scaling well, four additional products are in the pipeline, with validation completed and regulatory approvals awaited. These are expected to start contributing from FY27 onwards. Overall, the company appears to be on track to achieve its ambitious ₹1,000 crore CDMO revenue target by FY28.

In the Battery Chemicals segment, Acutaas has already commercialized its first two products, with two more expected to go commercial in FY27. Importantly, the company has secured contracts covering the entire planned volumes for the next couple of years, providing strong demand visibility. As a result, this segment should begin meaningfully contributing from FY27 onwards.

Semiconductor segment has stated to gain traction. This should play well for FY28.

Management is guiding for ~25% growth in FY27, and historically, they have tended to outperform their own guidance. Assuming margins sustain at current levels, FY27 EBITDA could exceed ₹600 crore. At current valuations, this translates to roughly 35x EV/EBITDA, which is by no means inexpensive.

As a reference point, Divi's Laboratories has historically commanded 40x+ EV/EBITDA multiples, largely due to its ability to sustain consistently high margins.

In comparison, Acutaas today not only matches, or even exceeds, Divi’s current margin profile, but is also delivering far superior growth. While some moderation is inevitable over time, that phase may still be a couple of years away, supported by strong tailwinds from CDMO, Battery Chemicals, and Semiconductor segments.

Given this backdrop, it is reasonable to expect elevated valuation multiples to sustain in the near term.

5. Vimta Labs – A Delayed Story or a Broken One?

Back in Jan’25, @drgsrk2006 presented this idea at the Hyderabad Investing Enthusiasts meet. In less than six months, the stock doubled, rewarding investors.

The core thesis then was - FY26 revenues of ₹450–500 crore with PAT of ₹90–100 crore.

Fast forward to 9M FY26, revenues stand at ₹299 crore with PAT at ₹57 crore, well below market and investor expectations. Unsurprisingly, the stock corrected sharply, slipping below ₹400 in March and now hovering around ₹450.

In hindsight, the stock price had run ahead of fundamentals, only to realign once the earnings trajectory failed to keep pace.

Q3 faced a few transient headwinds, including facility restructuring and a temporary slowdown in clinical research order inflows.

However, Q4 is expected to see a strong rebound, with revenues estimated in the range of ₹100–125 crore, aided by the catch-up of deferred revenues from Q3.

With results around the corner, this becomes a stock worth tracking at current valuations. Here are the key things to watch for in the Q4 results/concall:

Seasonal Tailwinds - The food testing division typically sees its highest numbers in Q4 due to seasonal demand.

Revenue Catch-up: Revenues deferred from Q3 due to operational delays are expected to be realized.

Capacity Utilization: The Electricals & Electronics division recently qualified a second EMI/EMC testing chamber, which will support growth as the existing chamber was already at 80-85% utilization

Biologics Launch: FY27 will be the maiden year for biologics contract research and development services. The facility is on track for commercialization by Q1 FY '27.

That's all for this edition. Have a great Sunday!

Disclaimer: None or buy or sell recommendations. This publicly available information is shared for learning and education purposes

English

@chopra_sumit @samisosa1234 So that sense, websol fits best for next 2 yrs as they are into cells right?

English

@samisosa1234 See value quest interview with Niraj shah - 2 year back profit pools were in module, now in cell and with AlCM II from june 26, may continue for 2 years and Almm III from june 28 for wafer and so on. There is no long term co. here. One who will move up the value chain will win

English

Rishi retweetledi

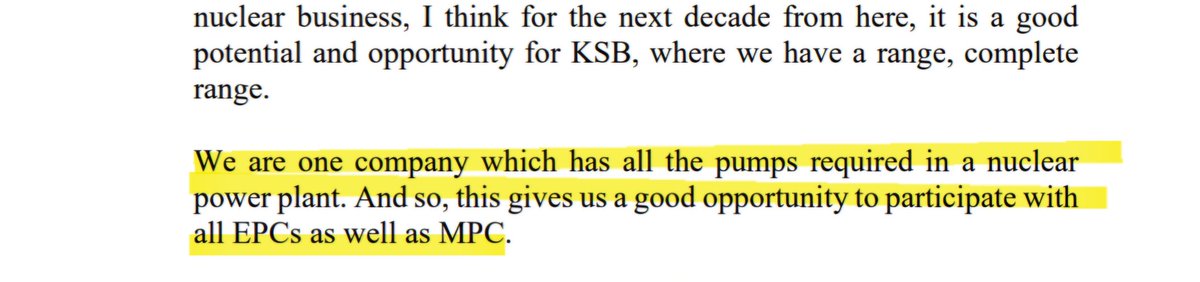

KSB - Nuclear Play 👌

🔶️ Full-scope pump supplier for nuclear plants

Snippet -> “We are one company which has all the pumps required in a nuclear power plant.”

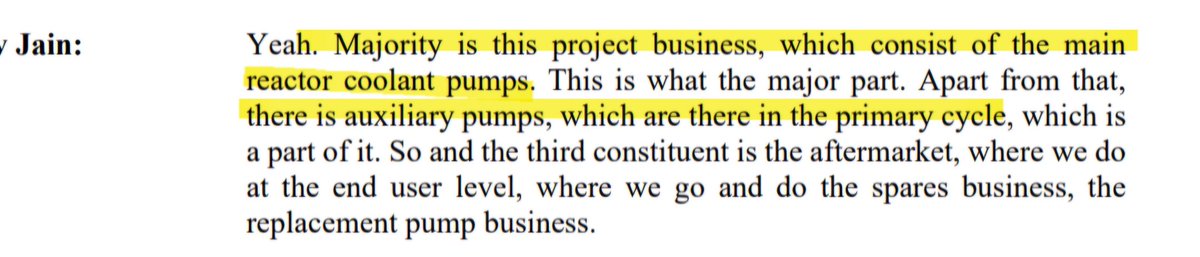

🔶️ Key product: Reactor Coolant Pumps (RCPs) + auxiliary pumps

• High-value, critical, long-gestation equipment

Snippet -> “Majority is this project business, which consist of the main reactor coolant pumps… Apart from that, there is auxiliary pumps…”

🔶️ Strong order book + long execution cycle

• Nuclear is ₹1,280 Cr order book

• Execution spread over FY26–FY28+

Snippet -> “Nuclear is ₹12,816 million… orders on hand.”

🔶️ Key customers / ecosystem

• Works with:

> NPCIL

> EPCs like BHEL / Megha

> International projects (e.g., Kudankulam via group)

Snippet -> “There is a business from NPCIL, there is business from Kudankulam.”

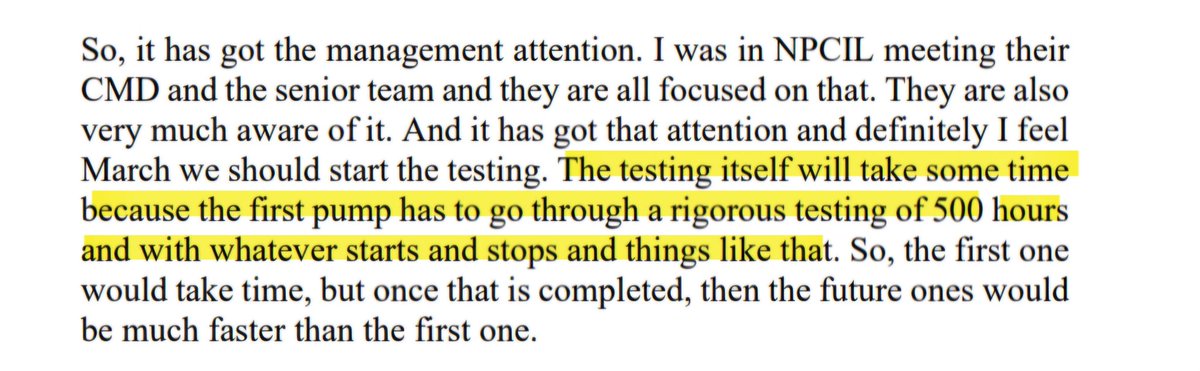

🔶️ High entry barriers (testing + approvals)

• Products require rigorous testing (e.g., 500-hour test cycles)

• Nuclear is long gestation + highly regulated

Snippet -> “The first pump has to go through a rigorous testing of 500 hours…”

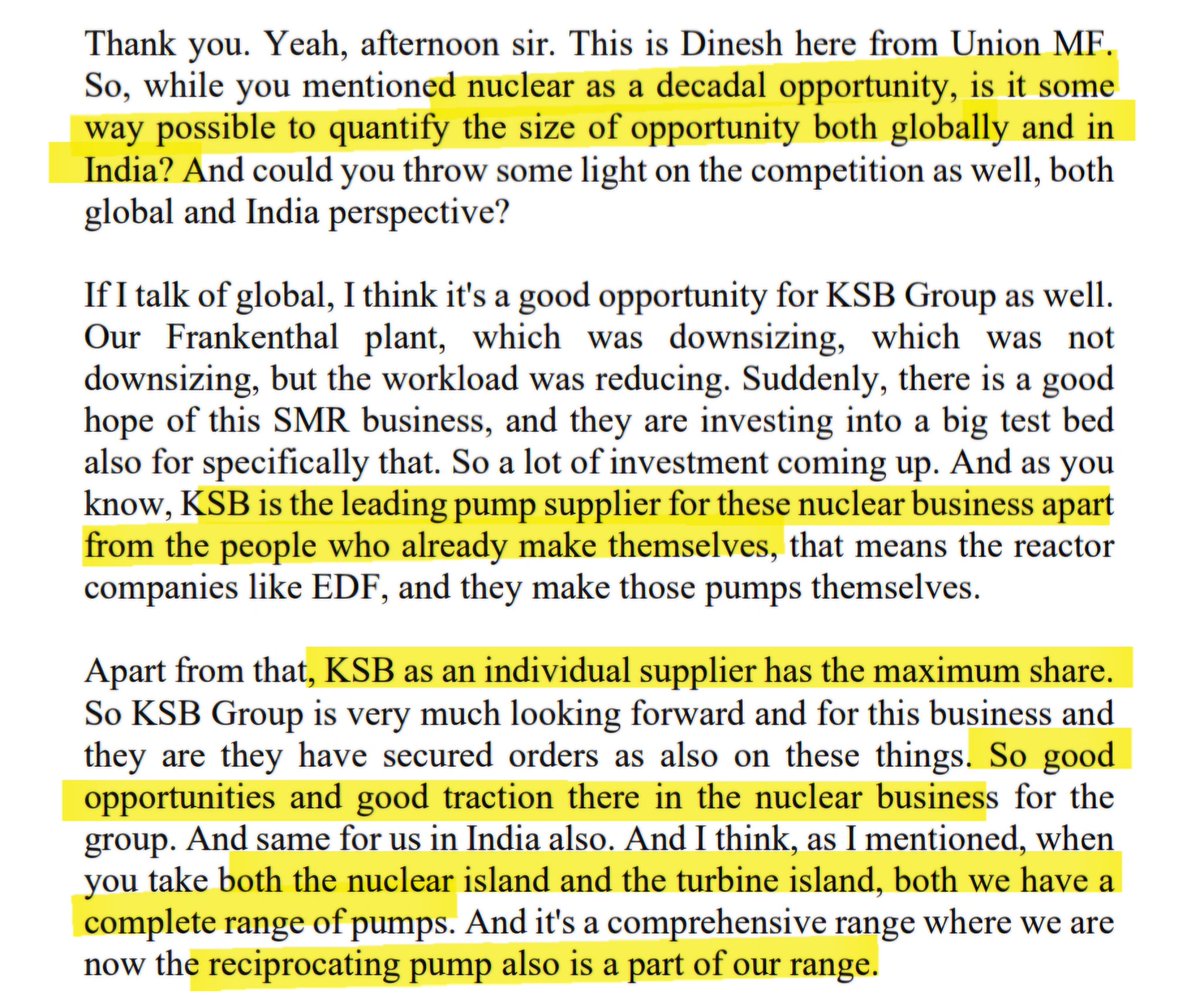

🔶️ Decadal opportunity with limited competition

• KSB has leading positioning globally (non-reactor OEM segment)

• But NPCIL exploring alternate vendors

🔶️ Revenue profile (lumpy but high margin)

• CY25 nuclear revenue low (~₹30-50 Cr) due to delays

• Expected ramp-up with execution

Snippet -> “CY 2025 was hardly anything, ₹30 crores to ₹50 crores.”

🔶️ Strategic importance

• High-margin + aftermarket potential

• Visibility over next decade

Snippet -> “Nuclear business… for the next decade… good potential and opportunity for KSB.”

💡 Bottom-line

• Critical supplier of nuclear pumps (especially RCPs)

• Full plant coverage → strong competitive moat

• Order book strong, execution ramp FY26–28

• Long-term structural growth driver (decade-long visibility)

👉 Follow @vishan_29 for more updates.

English

Rishi retweetledi

Listed recycling companies in India, the complete map.

> Battery Recycling (Lead)

Gravita India

Pondy Oxide

Jain Resource

POCL Enterprise

NILE

> End of Life Tyre

Tinna Rubber

GRP

Sampann Utpadan

Hi-Green Carbon

> Plastics

Ganesha Ecosphere

Rudra Ecovation

Avro India

Resgen

> E-Waste

Eco Recycling

Namo Ewaste

> Aluminium

Nupur Recyclers

Baheti Recycling

> Brass

Siyaram Recycling

> Copper

Bhagyanagar India

Sunlite Recycling

Parmeshwar Metal

Rajputana Industries

> Solid Waste

Antony Waste

Urban Enviro

Nikita Greentech

Organic Recycling

Sanmit Infra

> Coal Ash

Refex Industries

— END —

English

Critical Mineral Recycling - 1,500 Cr outlay for Lithium Ion batteries, E-waste and industrial scrap

Companies set to benefit 👌

1. Gravita India

2. POCL

3. Jain Resource Recycling

4. Baheti Recycling

5. Amaraja

6. Exide

No reco.

Investment Veda@InvestmentVeda

India's Critical Mineral Strategy just took a serious step forward. Govt approved 58 companies under the ₹1,500 Cr Critical Mineral Recycling Scheme. Key highlights: • Focus: Lithium-ion batteries, e-waste, industrial scrap • ~₹5,000 Cr private investment committed • ~850 KTPA recycling capacity planned Why this matters: This is not just recycling, it is also supply chain strategy. India is: → Reducing import dependence → Building EV & energy storage backbone → Moving toward a circular economy Companies likely to benefit: • Exide Industries, Amara Raja Energy • Gravita India, Pondy Oxides • MSTC • Hindalco, Vedanta, Tata Chemicals • Indirect: Tata Motors, Reliance Recycling = the cheapest source of lithium, cobalt, nickel. #India #Investing #EV #EnergyTransition #Metals #CircularEconomy

English

@rohantantia Sunlite, baheti etc gave phenomenal returns!!

which companies are you bullish on Rohan bhai?

English

Rishi retweetledi

India’s recycling sector is no longer a niche - it’s evolving into a full circular economy supercycle driven by policy, consumption & commodities!!

👉What looks like “waste” is actually a multi-layered industry stack?

1. Rubber:

🔹GRP Ltd.

🔹Tinna Rubber and Infrastructure Ltd.

🔹Hi-Green Carbon Ltd.

2. Metals:

🔹Gravita India Ltd.

🔹Pondy Oxides & Chemicals Ltd.

🔹Baheti Recycling Industries Ltd.

🔹Sunlite Recycling Industries Ltd.

3. E-waste:

🔹Eco Recycling Ltd.

🔹Namo eWaste Management Ltd.

4. Plastics:

🔹Ganesha Ecosphere Ltd.

🔹Race Eco Chain Ltd.

5. Scrap:

🔹MSTC Ltd.

🔹Antony Waste Handling Cell Ltd.

🔹Urban Enviro Waste Management Ltd.

6. Biogas:

🔹Organic Recycling Systems Ltd.

7. Water:

🔹Z-Tech (India) Ltd.

🔹Effwa Infra and Research Ltd.

🔹Greenleaf Envirotech Ltd.

🔹EP Biocomposites Ltd.

🔹EMS Ltd.

🔹Ion Exchange (India) Ltd.

🔹VA Tech Wabag Ltd.

🔹Concord Enviro Systems Ltd.

🔹Denta Water and Infra Solutions Ltd.

8. EPR:

🔹GEM Enviro Management Ltd.

👉Why this theme is structurally strong:

🔹EPR norms tightening → recycling demand is mandated

🔹E-waste explosion → electronics adoption + shorter cycles

🔹Metal price tailwinds → better realizations

🔹Government push → formalisation + compliance

🔹Organised players gaining share → shift from informal sector

👉Key Insight: This is not just a demand story - it’s a market share transfer story, from informal recyclers to organised, tech-driven companies

👉Where real value lies?

🔹Commodity recycling → volume-driven, cyclical

High-value segments:

🔹E-waste (precious metals recovery)

🔹Battery recycling (future multi-decade theme)

🔹Specialty materials

👉Recycling sits at the intersection of Consumption (electronics) + Commodities (metals) + Policy (EPR). Few sectors have this powerful combination

👉Recycling is becoming the hidden supply-side engine for metals & materials

👉India is moving from: Waste disposal → urban mining economy

👉Follow @rohantantia for more deep dives!! Bookmark it for future reference!!

Disclaimer: Do not consider it as a buy/sell recommendation, just for information!! Do your own due diligence.

#StocksToWatch #StocksInFocus #StockMarketIndia @TrendSpark420 @DhawalDoshi5 @swingcrafthq @finvibe @sustainme_in @Sky16akash @Kj_techtrades @Dynamicinvstr @Prabinmen @GingerInvest44 @Prouspering @SmartInvest92

English

Rishi retweetledi

Dynamatic Technologies haven't shown any earnings growth yet stock has gone 11x in last 5 years due to Aerospace Tailwinds & collaborations.

Walchandnagar Industries is another unique co playing in Aerospace & Nuclear.

After showing losses in many quarters finally showed profit last quarter.

Walchandnagar in today's interview 👇

Q4 Performance Will Be Similar Like Q3

FY27 Onwards Performance Will Be Positive (QoQ)

Plan To Raise Funds In 3-4 Months (75% For Nuclear and 25% For Defense/Working Capital)

Co Is In 12-13 Missile Programmes

Will Continue To Remain in Core Nuclear Mfg.

Expect To Have Large Order Booking This Year.

Can this co ride the Nuclear Wave only time will tell.

tushar@tushar9590

Aerospace theme in India is taking off in the most visible way. Sansera Engineering ADS(Aerospace Def & Semiconductor) order book grew from 200 Cr and of FY24 to 3900Cr today. Dynamatic Technologies MOU with france based Hutchinson in composites, & Collab with Germany based Dynauton systems to develop MALE UAV platform. Hyderabad based Sigma Advanced secures ₹3800 Cr order from Rolls Royce to supply Aerospace parts. Can add more to this.

English

While Vikas Khemani bought the largest stake in PTC Industries.

In August 2020 Porinju & Pankaj Prasoon also bought in bulk deal when mcap of the co was in triple digits.

Ashish Kacholia and Mukul Agarwal both joined the party when PTC Industries was valued at 9000 Cr.

Pankaj Prasoon holds over 1 percent in the co.

tushar@tushar9590

Vikas Khemani known for picking ideas much ahead of others. Invested 15-20Cr in PTC Industries(in Aerospace theme) in 2020 for nearly 5% stake. Today He still holds 2.6% stake in the co which is worth 633 Cr. Nearly 900-1000Cr returns on investment of 15-20Cr. Started watching him back in 2020 when he identified Praj Industries.

English

Power demand is structurally rising due to:

AI + data centers

Electrification

Renewable integration

Every unit of power needs:

→ cables

→ transformers

→ switchgear

→ insulators

Added one insulators company today .

Will post in detail ..

English

Rishi retweetledi

If you want to understand businesses like

Welspun corp

Venus

APL apollo

Sambhv etc etc

Best to watch this video from an industry expert @saket1974

youtu.be/2o-FV9b-yJw?si…

YouTube

English

A ₹4,171 Cr SmallCap defense stock just delivered ~4X in one yr

And it's not done.

While Business channel plays war drums, crude charts, and Trump's Truth Social feed on loop —

The real money was being made quietly. As always.

Its always Stock picker's market

English

Bangalore meet tomorrow Sunday

Place indiranagar

Time 3pm

If interested, let me know

English

Rishi retweetledi

Rishi retweetledi

New entry in the portfolio:

SKP Bearings

At current levels, if we write off the bleeding French subsidiary, then the Indian business itself is seeing spectacular cash flow. The Zamar plant is operating at 23% capacity currently and operating leverage is bound to play here if we get increased utilisation. Even at 15 standalone p/e, we get a market cap of 230-250 cr. This is the bear case scenario if the French acquisition doesn't pay off.

Now consider the bull case where the management is saying that the French subsidiary will break even in this calendar year itself. And if it can go to its previous annual revenue rate of around 70-80 cr with PAT margins of 10%, that adds 7-8 cr to the bottomline. A sme business with an international acquisition generating annual 70-80 cr will be instantly rerated to 25-30 p/e by the market. So combine the cash flow and operating leverage playing out in the Indian business and the international subsidiary generating profits, we might see a market cap of around 600-700 cr. This is at least a 2x-3x story on medium term. The consolidated p/e looks optically high because the cash generated by the Indian business is being burnt at the French side. But in microcaps, always look for solvable problems which are giving you prices at distressed valuations. This one perfectly plays that out.

In terms of quality, the business has a micro moat because precision engineering is growing at a unprecedented rate currently. They supply to international OEMs like SKF, Timken, FAG and that alone proves their quality. The promoters have high skin in the game where they put money out of their own pocket into the business and they have been buying shares as much as legally possible since the last year. This signifies extreme bullishness and conviction in their company.

There are multiple triggers at play here one of which is the QCO against Chinese dumping. That is yet to play out but the Hormuz crisis may act as artificial QCO because sourcing from China via sea might get expensive for many end customers. That will force many Indian OEMs to look within the country and who is better positioned than SKP with their capacity and prowess?

This company was first brought to my attention by @Manojeet_Das but I was hesitant due to the cash burn of the French acquisition. Many times, the ego of the management gets in the way and they bleed the profitable, cash flowing side of a business to burn cash on the acquisition side. However, at current levels as I said earlier, the market is already discounting the French cash burn. The liquidation of that asset in dire cases will even be seen as a bullish signal by the market. However, if the French acquisition becomes profitable, that is the most bullish case scenario and there is a large chance of that to happen because in such business, changing your supply side is not so easy. It's taking time because Eruope has strict labour laws, carbon footprint controls and a thousand other legal things when an entity changes ownership. But overall, I think there is a good opportunity here.

English

Rishi retweetledi

Manorama Industries

The market is still sleeping on the potential revenue surge that could happen in Manorama Industries in the next 5 years.

The company is moving from being mainly a niche processor of exotic fats and cocoa butter equivalent into a much larger, more integrated specialty fats platform. Management has explicitly said the current capex of 460 crores gives them growth visibility for the next 4–5 years.

The increase in capacity from 40,000 MTPA ---> 52,000 MTPA through debottlenecking in its fractionation plant will drive growth in FY27 and FY28. After that, the CAPEX related asset- turnover will come into play.

The mgmt has explicitly said that the turnover will be more than 5x. That could be north of 2000 crores additional revenue from FY28 onwards (subject to utilization levels).

A big reason this growth can be durable is that Manorama is emphasizing value-added products rather than low-value output. Value-added products already form about 75% of sales, and they said they want that to move toward 90–95% over time. That matters because it supports margins and customer stickiness.

On a 1300 cr revenue base for FY26, and the management said they will do upwards of 30% growth in FY27, it will translate to ~1700 crores in FY27.

Considering a less- aggressive asset turnover of 1600 crores that will be added to topline after FY28, it gives me somewhere around 3500 crores of revenue by FY30. With 17.5% PAT margins, it will be around 615 crores of PAT. That is more than 5x increase over FY25 levels.

However, we need to watch out for depreciation costs, any ramp-up inefficiencies, and how fast the new CAPEX goes to full utilization.

English

For India, what's a reasonable minimum liquid net worth to achieve financial independence?

Of course it depends, but any ballpark?

English

@gurjota @drpps Absolutely agree with you sir - "greed has no end"

But it's worth contemplating that your 10cr might be someone's greed,and his ,say 1cr, might be someone else's greed.This too has no end.

I feel, starting point of the journey of 10cr or 1cr should be gratitude for today's wealth

English

@drpps "Greed has no end"

Already mentioned in my post above.

English

After 8-10 crore, your own home and a nice car, there is not much difference in the quality of life between you and billionaire investors like RK Damani.

Time is the currency of life. Money is not.

Both of you have limited amount of time on earth; infact you may have twice or more time than RK Damani, so you are richer than him.

Dal roti is dal roti whether a billionaire eats or you do.

Become financially independent, which is around 8-10cr.

Have good food. Workout. Sleep well.

Meet your parents and friends.

That’s all there is to life.

Greed has no end.

Sooner you figure this out, happier you will be.

English