Which public sector bank has smooth online banking experience relatively? I am looking to open a savings account. I am interested in PNB, BOB, Canara banks currently, what is everyone's experience?

#BankSystem

English

Market Mentor

3K posts

@stockastician

Permanent Bull || Microcap Enthusiast || Long Term Investing || Techno Funda Analysis || Enterpreneur || Not SEBI Registered || Multibagger Hunter 🚀 || DM Open

New entry in the portfolio: SKP Bearings At current levels, if we write off the bleeding French subsidiary, then the Indian business itself is seeing spectacular cash flow. The Zamar plant is operating at 23% capacity currently and operating leverage is bound to play here if we get increased utilisation. Even at 15 standalone p/e, we get a market cap of 230-250 cr. This is the bear case scenario if the French acquisition doesn't pay off. Now consider the bull case where the management is saying that the French subsidiary will break even in this calendar year itself. And if it can go to its previous annual revenue rate of around 70-80 cr with PAT margins of 10%, that adds 7-8 cr to the bottomline. A sme business with an international acquisition generating annual 70-80 cr will be instantly rerated to 25-30 p/e by the market. So combine the cash flow and operating leverage playing out in the Indian business and the international subsidiary generating profits, we might see a market cap of around 600-700 cr. This is at least a 2x-3x story on medium term. The consolidated p/e looks optically high because the cash generated by the Indian business is being burnt at the French side. But in microcaps, always look for solvable problems which are giving you prices at distressed valuations. This one perfectly plays that out. In terms of quality, the business has a micro moat because precision engineering is growing at a unprecedented rate currently. They supply to international OEMs like SKF, Timken, FAG and that alone proves their quality. The promoters have high skin in the game where they put money out of their own pocket into the business and they have been buying shares as much as legally possible since the last year. This signifies extreme bullishness and conviction in their company. There are multiple triggers at play here one of which is the QCO against Chinese dumping. That is yet to play out but the Hormuz crisis may act as artificial QCO because sourcing from China via sea might get expensive for many end customers. That will force many Indian OEMs to look within the country and who is better positioned than SKP with their capacity and prowess? This company was first brought to my attention by @Manojeet_Das but I was hesitant due to the cash burn of the French acquisition. Many times, the ego of the management gets in the way and they bleed the profitable, cash flowing side of a business to burn cash on the acquisition side. However, at current levels as I said earlier, the market is already discounting the French cash burn. The liquidation of that asset in dire cases will even be seen as a bullish signal by the market. However, if the French acquisition becomes profitable, that is the most bullish case scenario and there is a large chance of that to happen because in such business, changing your supply side is not so easy. It's taking time because Eruope has strict labour laws, carbon footprint controls and a thousand other legal things when an entity changes ownership. But overall, I think there is a good opportunity here.

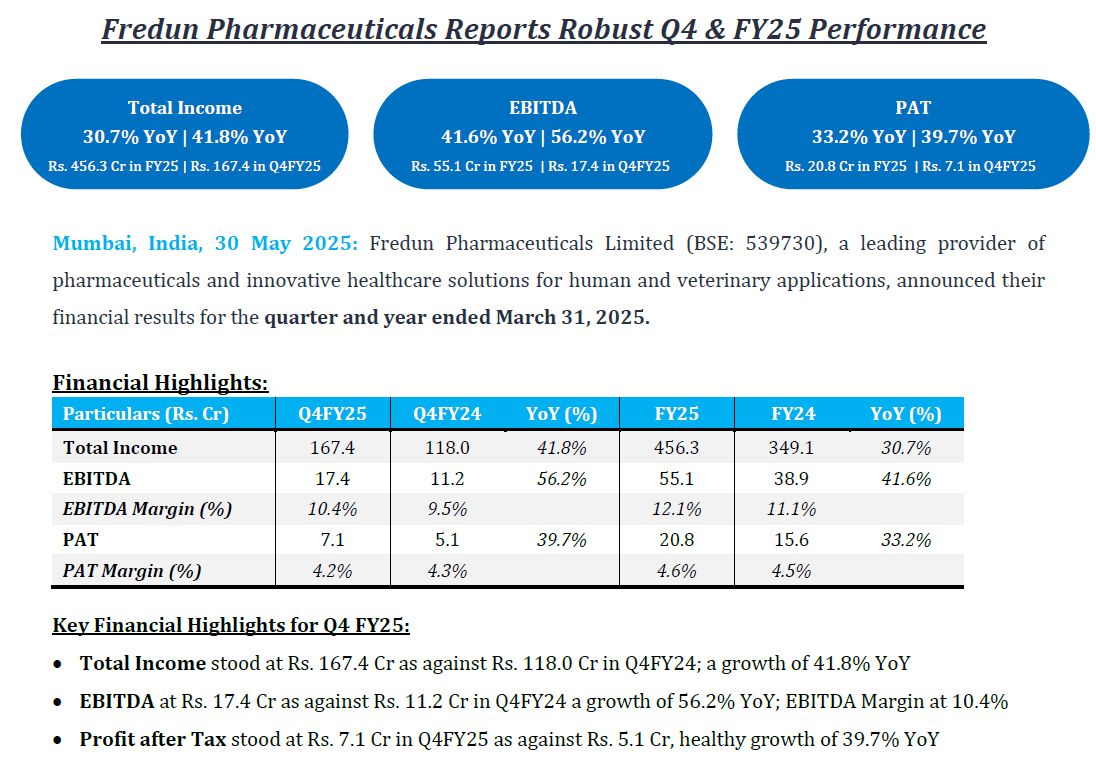

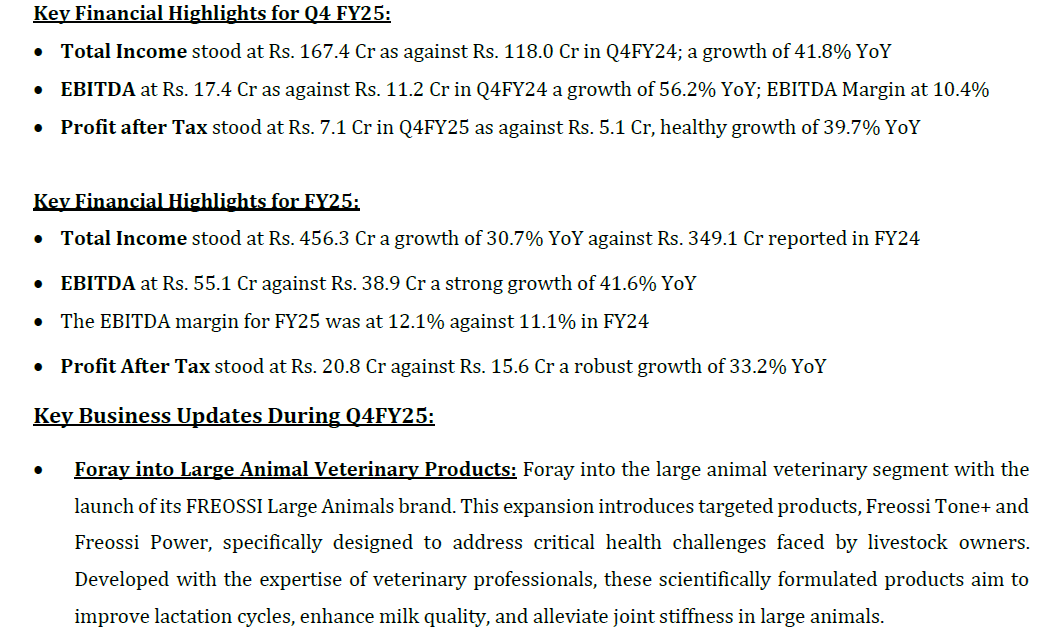

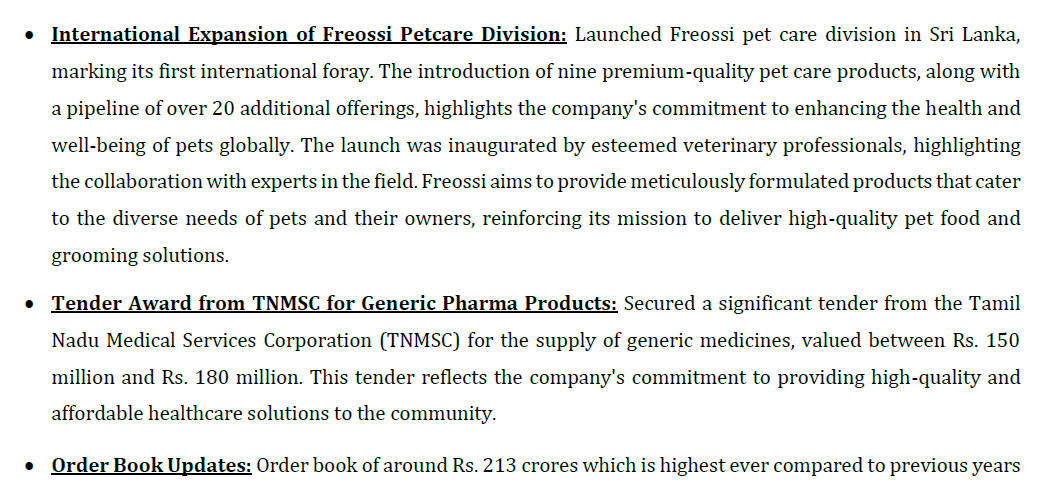

Fredun Pharmaceuticals 💊 Getting too undervalued imo. Seems like big players want to accumulate before it goes up with a large volume. Multiple triggers: - Remarkable consistent growth - Expanding capacity - Niche pet care segment - Beneficiary to consumption theme of India - Range bound price for 3 years - Cheap valuations #stockmarketscrash

I am the only one who has correctly predicted almost every move of the Stock Market in last 2 years. You can ask grok to verify the same. Some examples - In March 2024, I predicted about correction coming from September/October 24 . It actually happened. It takes a lot of guts to predict about a correction 4 months before it actually happens and in raging bull market. In September 24, I posted I booked all profits and cash moved to Gold, Silver , other asset class. I gave Gold and Silver as Diwali picks in 2024 when everyone was giving stock names. What happened in Gold and Silver after that is known to all. Recent tale of timing market - Cautioned about sharper fall after 17300(#CNXSmallcap) - which came Then posted 'did some buying' around 16700-800 - #CNXSmallcap recovered 600 points after that Posted sold trading positions - market again fell after that Then posted topped up many holdings- 1000 points rally after that Then around 18000 posted -sold all trading positions and trimmed some holdings - Market fell exactly after that and still falling. Did 'Brace Yourself' post- market saw the carnage after that . Again did 'Brace Yourself' post at 17500 and #CNXSmallcap touched 14986 . Posted about support of #CNXSmallcap 14900 and decent bounce to 15900. Market reversed from 14986 and made high of 15980. I had given 3 scenarios of market bottom case in January . We are done with Scenario 1. Scenario 2 also is highly likely to happen. Check my timeline to find or ask grok for that specific post. Before you come trolling please read my previous posts. This may sound as self bragging post but sometimes it is good to flaunt it if you have it. #Investing #StockMarket