SY

2.9K posts

This could be $CBBHF in 2-3 years.

🏴☠️@calvinfroedge

Just a decade ago, this was an obscure no-name stock trading for pennies Now it's a mid cap miner

English

@Lazarus_Capital @BenBajarin @bitcoinbutcher1 Do we know how much nbis pays data one for infrastructure build and maintenance?

English

“Nebius has interesting contract-design optionality, but too little disclosure around GPU count, unit economics, power delivery, and software premium to call it the cleanest stack.”

Semi analysis showed that building servers in house can save 10-15%, backing out Dells margin I got an operating margin of 9% on AI server systems, should be higher in gross margin and when you include ancillary equipment. In Line with semi analysis but below Arkday’s statement of 15-20%, though that was a comment from a while ago. DELL and SMCI mentioned how AI server margins have come down.

They were labeled the Google of Russia for a reason, and Arkady managed to get a lot of these engineers out over to Nebius, so their staff is definitely being under appreciated.

But I agree on the software premium, black box, have nothing on that. Roman mentioned they had a customer whose inference cost was lower with NBIS than what they were getting it in house. Even when Nebius gave them the blueprint on how do to bring it down, they weren’t able to replicate the results. Speaks to the technical capabilities at Nebius but to me the question became “why is Nebius trying to help their customers lower their inference in house cost” that’s their margin. Either they view the edge as immaterial in the long run and chose customer satisfaction? Maybe they’re focused on growing their customer base over monetization?

Been pondering that ever since. Would welcome any of your thoughts cause it’s got me scratching my bald head.

English

Let me predict $IREN earnings:

- No deal

- Miss blamed on $BTC

- Hype up the energization

- Hang a carrot for Australia market

- Dilution news a day after

I’ll eat crow if news is stellar…

English

@CKCapitalxx Difference is IREN has power in hand ,nbis has paper in hand. Power> paper

English

I really don’t see why people bother buying $IREN when you can just buy the better company in $NBIS

Both $IREN and $NBIS have a Microsoft contract.

That is where the comparison ends.

$IREN signed a $9.7 billion Microsoft deal in November 2025. Good contract. Real revenue. But that is the last major contract announcement they have made.

The pipeline since then has been smaller neocloud names like Together AI, Fluidstack, and Fireworks AI. Nothing wrong with that but it is a very different customer profile.

$NBIS signed a $19.4 billion Microsoft deal. Then signed a $27 billion Meta deal in March 2026. Then won the contract to build and manage Israel’s national supercomputer.

Three massive contract announcements in rapid succession and the velocity is not slowing down.

Microsoft chose both. Meta chose $NBIS. A sovereign government chose $NBIS. Nvidia chose $NBIS with a $2 billion direct equity investment and preferred GPU allocation that no competitor has access to.

$NBIS was also the first company in Europe to deploy Nvidia’s HGX B300 Blackwell Ultra and holds Nvidia Exemplar Status for training workloads.

$IREN is executing on one big contract. $NBIS is stacking them.

And while $IREN sits under a $6 billion ATM equity offering that represents 37% of their market cap drip feeding dilution into shareholders, $NBIS raised $4 billion in convertible debt and has the backlog to justify every dollar of it.

$46 billion in contracted backlog. $7 to $9 billion ARR by end of 2026. 12 analysts. Strong Buy consensus.

Same theme. One company is building a business. The other is building a pipeline.

$NBIS

English

There are 2 different sets of warrants. The publicly traded ones have a strike price of $11.50/sh. The ones you’re referring to are the warrants recently issued to Macquarie. Those have a stroke price of $4/sh. Those were only issued to Macquarie as part of the recent financing deal.

Be careful.

English

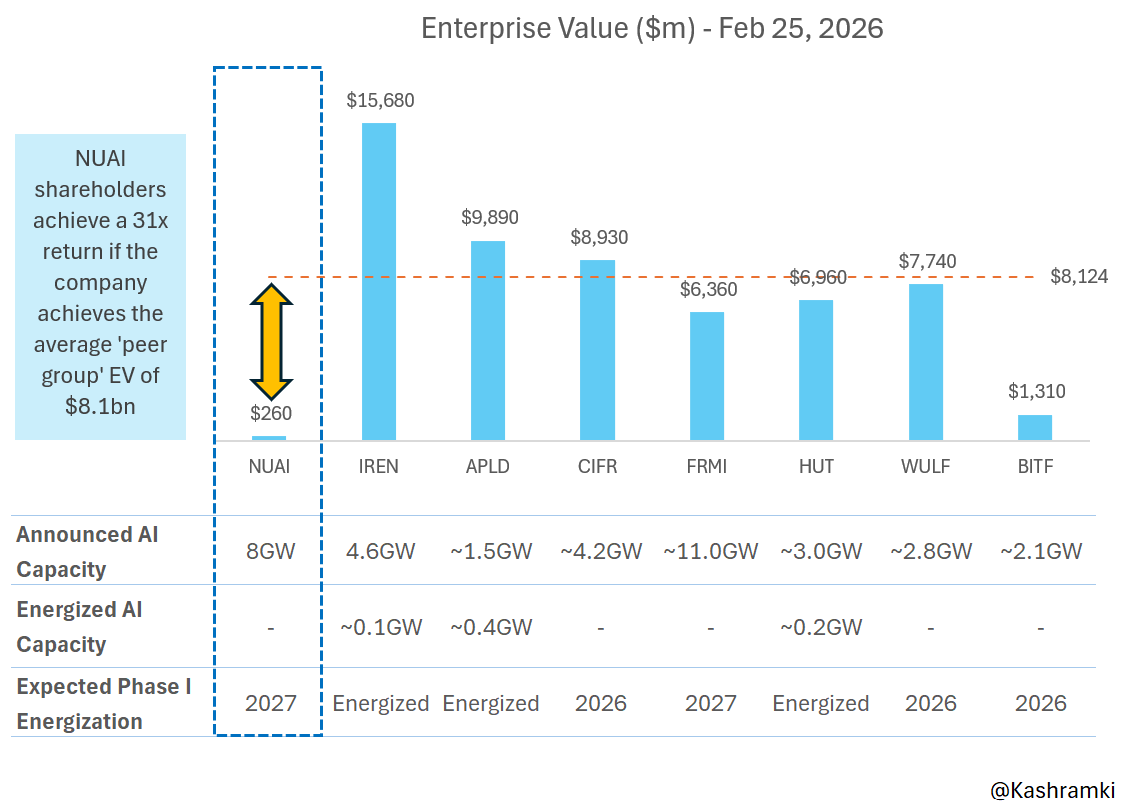

I prepared this chart to illustrate the severe mispricing in $NUAI.

Current EV: ~$260M

Peer average EV: $8.1B

That gap? Massive mispricing for a company with 8GW announced AI capacity - Expected energization of Phase I in 2027 - pure behind-the-meter power buildout, and no grid queue nonsense.

Peers like $IREN ($15.7B EV, 4.6GW), $APLD ($9.9B, ~1.5GW), $CIFR ($8.9B, ~4.2GW), $HUT, $WULF etc. are getting huge credit for announced hyperscaler deals. But reflect on this: Even though they've inked those deals, the vast majority of their capacity remains in construction, with energization timelines mirroring or a year ahead of $NUAI's 2027 expected timeline.

Execution risk cuts both ways—yet the market prices $NUAI for total failure while rewarding peers well before energization.

Downside protected by powered land value alone.

Upside explosive on first hyperscaler deal.

The yellow arrows and the dotted red line tell the story.

$NUAI

English

English

@KashRamki @Divyan__shhh Thx you sir.. I'm actually losing my mind on the warrant piece...I have never held a warrant but from what I could dig $nuaiw warrant is trading at 1.67$ and the exercise price is .01 and the stock is at 4$ ... so I can convert warrant to shares now ... what am I missing

English

@KashRamki @Divyan__shhh Hi bro,was doing some DD on NUAI and came across this tweet of yours... since Q1 2026 is already done and they haven't announced any hyperscaler deal , do you think they are close? Price is very attractive now so I'm a bit inclined to pull the trigger

English

$NUAI management has guided announcing an investment grade hyperscaler by Q1 2026. That’s a universe of just 4 customers, all interchangeable. That the most transparency any management team has ever given the market ahead of actually signing a tenant. They must have something the hypers can’t refuse.

English

@TheTechInvest I wish so ❤️. Do you know at what stage did they announce smart roles for horizon?

English

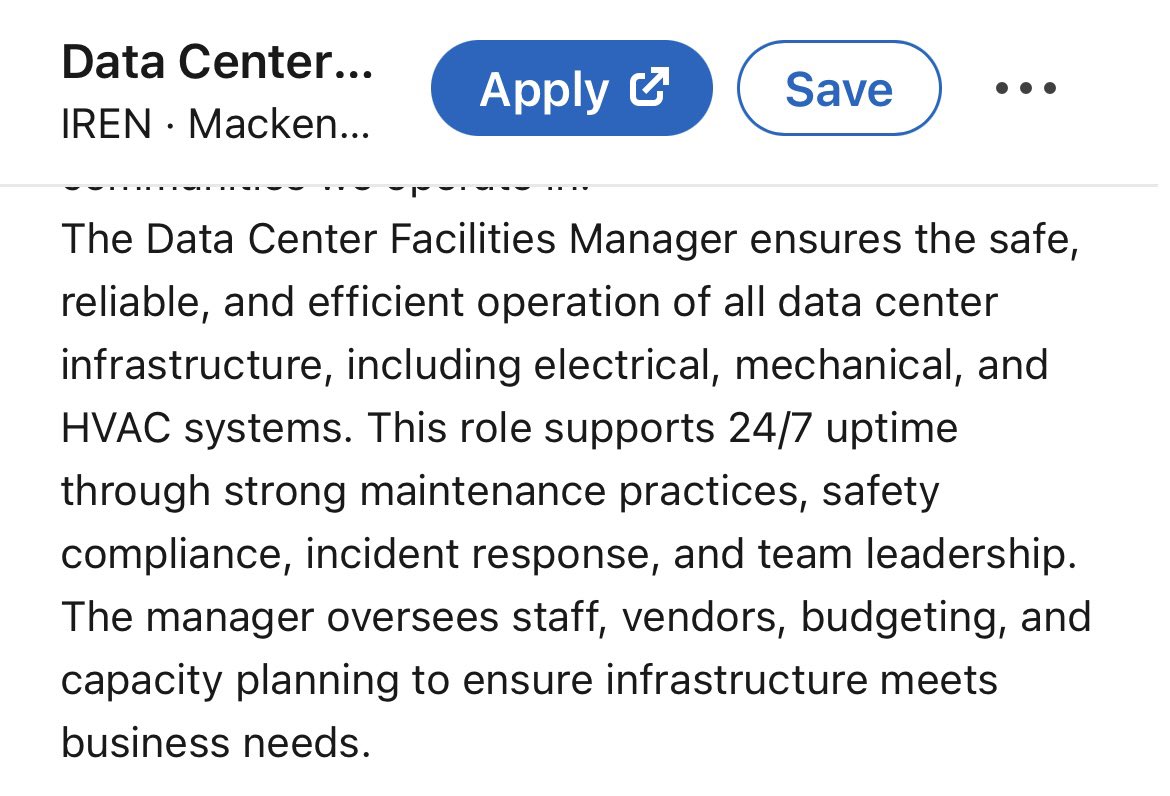

Is $IREN announcing 2 deals next week for Prince George and Mackenzie?

Read the job descriptions carefully.

The Tech Investor@TheTechInvest

$IREN Just added 7 new positions for Prince George in the past 24 hours. Interesting 🧐

English

The last 1 cm in AI GPU power delivery is not disappearing.

800V helps the rack.

48V reshapes the board.

But the GPU core still needs thousands of amps at less than 1V.

That is where the business models begin to diverge.

Same current.

Five different income statements.

Full deep dive is now live:

nuttycld.substack.com/p/the-economic…

Nutty@NuttyCLD

English

@PhotonCap So is it fair to say that POET is a very good tech with very bad management?

English

기술을 분석한다곤 했지만, 차트도 올리고 공개된 장소에서 POET을 이야기한 입장에서 글을 남겨봅니다.

어떤 학술지와 학회를 reference로 인용해왔는지, 광공학 비전공자분들을 위해 한 번 정리합니다.

JLT (Journal of Lightwave Technology)

IEEE Photonics Society와 Optica 공동 발간. 2024 Impact Factor 4.8. JCR Optics 카테고리 26/125 (Q1, 상위 20.8%). Engineering Electrical & Electronic 88/366 (Q1). accept rate 50% 미만. photonic device, 광통신 분야의 메인 저널입니다.

Nature Communications

Nature 자매지. 종합과학 Q1. Photonics 커뮤니티 내부 검증을 통과한 결과가 한 번 더 외부 검증을 거치는 자리.

ECOC (European Conference on Optical Communications)

OFC와 함께 세계 광통신 양대 학회. 매년 9월 유럽 개최. 1.6T transceiver 같은 산업 직결 데이터가 가장 먼저 공개되는 자리.

VLSI Symposium

ISSCC, IEDM과 함께 반도체 3대 학회. 삼성전자, SK하이닉스, NVIDIA가 발표하는 자리입니다.

삼성: thelec.kr/news/articleVi…

SK하이닉스: news.skhynix.com/sk-hynix-prese…

NVIDIA: ieeexplore.ieee.org/document/98302…

POET 기술 관련해서 이 4개 통로를 통과한 측정 데이터를 짚어두면:

post-bond X 0.09 μm @ 3σ alignment (JLT 2023): 머리카락 굵기의 약 1/800 정확도로 III-V chip을 interposer에 passive 정렬했다는 측정값.

1.6T 2xFR4 PIC, Ssd21 53.7 GHz (ECOC 2025): 4-EML 기반 1.6T 광송신기 PIC의 RF bandwidth. 패키징 후 RF penalty를 3 GHz 수준으로 억제.

HZO-LNOI Pockels photonic memory 65.1 fJ/state (Nature Comm 2025): 비휘발성 photonic memory state 당 65.1 fJ, 4-bit, 10년 retention, 10⁷ endurance.

peer review를 통과한 숫자는 published된 시점에 고정됩니다. 외부 사건과 무관합니다.

경영진의 실기는 경영진의 책임이고, 엔지니어의 데이터는 엔지니어의 자산입니다. 둘을 같이 묻으면 안 됩니다.

🐨코알라🐨@dorytossy

@__bag_h_dad @tslasoxllo49798 @PhotonCap 포톤캡님. 지금까지 일련의 사태로 봤을때 혹시 포엣이 펀더멘털 하나 없는 그런 회사인지(개잡주)인지 말씀 좀 해주실수 있을까요.

한국어

A lesson from $POET:

Don’t invest in a company whose CEO only owns 0.0083% of the float

There are people on X who own more than that

English

@BryzonX @Sofigoodboy That's precisely was my worry about this stock a few months ago.

English

This is why it’s important to not FOMO into something you don’t understand

$POET down nearly 50%

English

$POET a big issue here is all of these dumb X accounts screaming about $POET and $MRVL having some sort of deal get picked up by $HOOD AI and tons of retail flood in based on $HOOD news feature

Celestial AI had always been a tiny unimportant coustomer and social media BSers are now able to manipulate news flow on trading platforms not only Grok

TheUndefinedMystic@pennycheck

If your buying POET because of some very misleading posts making you think the CFO said in the stocktwits interview they recently did a deal with $MRVL you should probably be aware there is no new deal with MRVL all the CFO said was they have a deal with CelestialAI which has been known for years / that got acquired by $MRVL which is well known. If your invested just understand what it is and what it isnt

English

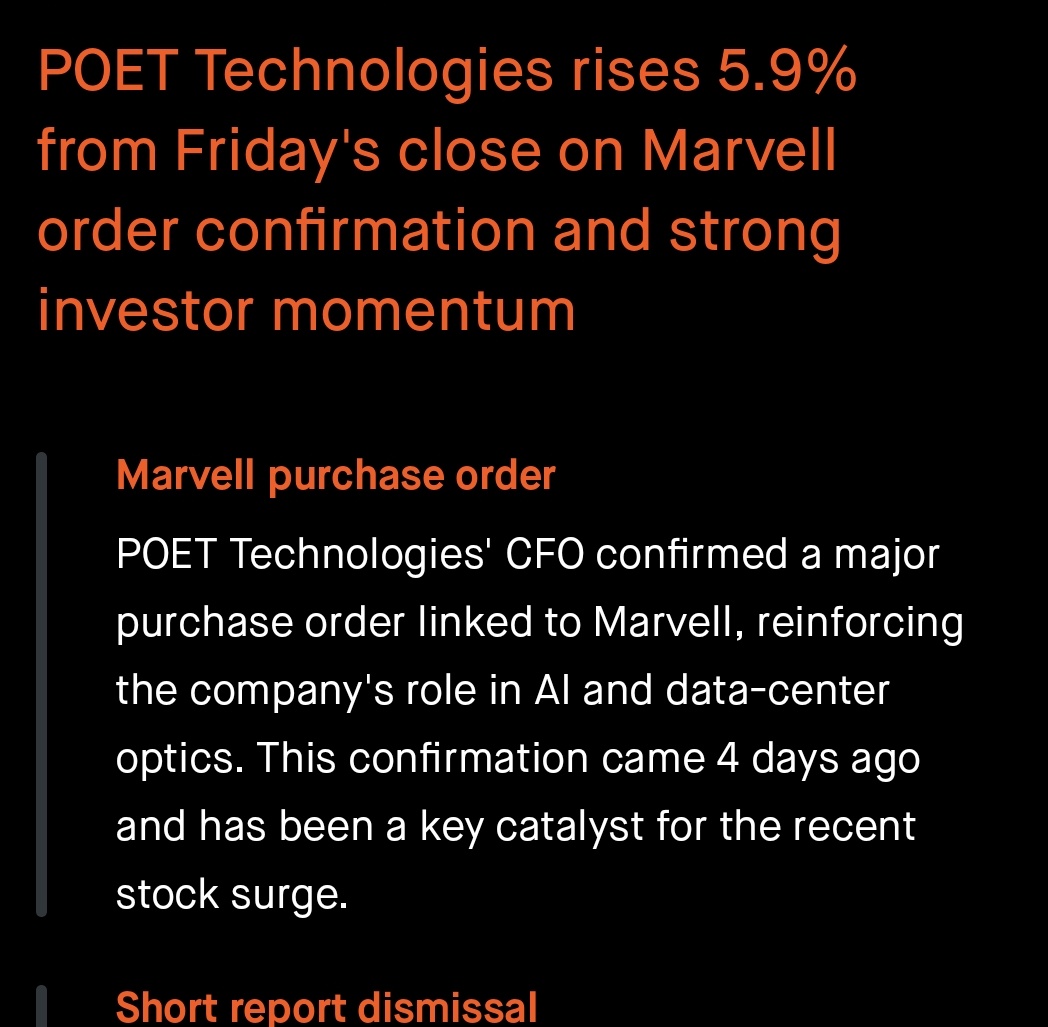

$POET - POET Technologies Inc, a leader in the design and implementation of highly-integrated optical engines and light sources for artificial intelligence networks, today announced the cancellation of all purchase orders received by the Company from Celestial AI.

Including the ones for initial production units first disclosed (the "Purchase Orders") by the Company in a press release on April 25, 2023.

$MRVL Marvell Semiconductor Inc., which acquired Celestial AI, provided written notice of the cancellation to the Company on April 23, 2026. As the basis for the cancellation.

Marvell indicated that the Company had made disclosures of information related to the Purchase Order and shipping information in contravention of its confidentiality obligations.

English

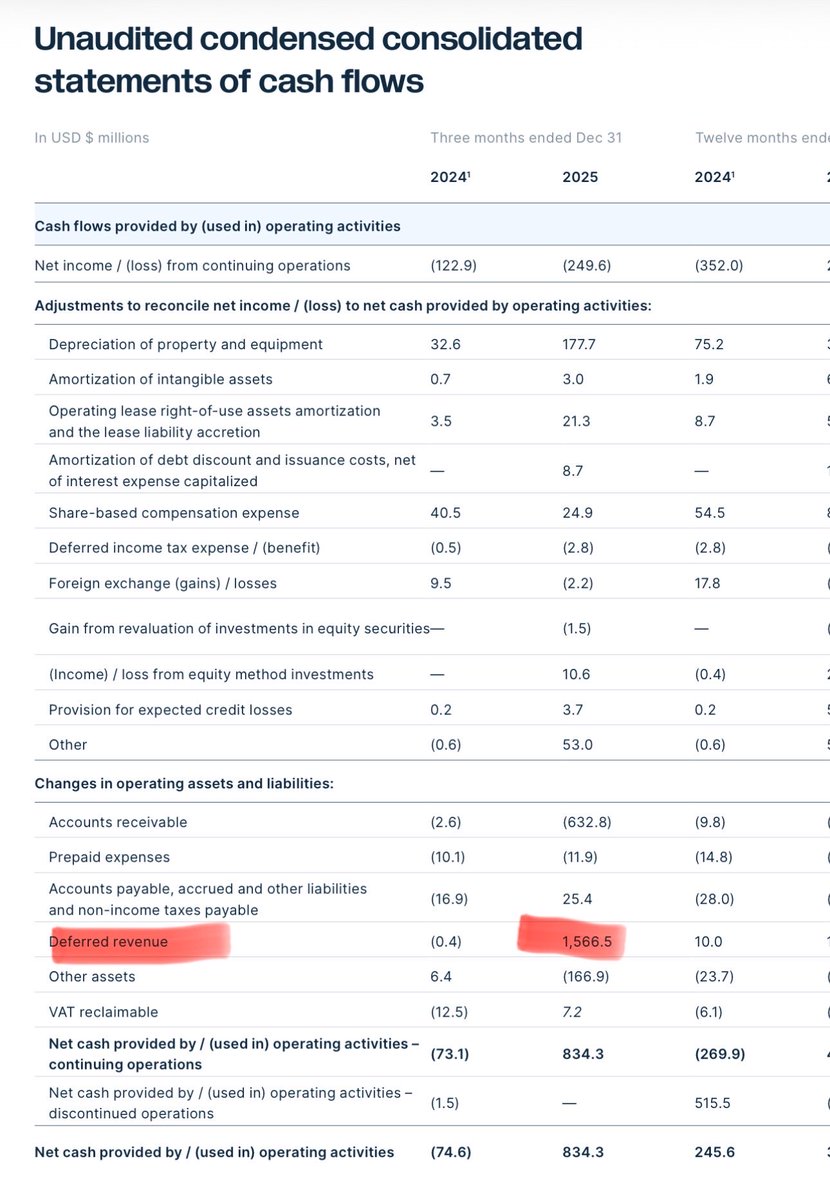

@helsiti170246 @FransBakker9812 @AlexfromBabylon assets.nebius.com/assets/8662572…

This is NBIS 6K filing around the contract. It didn't talk about prepayment explicitly. Could that differed rev be something else? Or did NBIS announce it somewhere else?

English

$NBIS $IREN What both sides don’t understand is that both of these companies are not building for the same outcome. As Ben stated earlier Neoclouds is a misleading term. What might be good for someone with 4th hyperscaler ambitions, might not be good for someone who wants to become the largest bare metal player in the world and vice versa.

Yes, both tun baremetal as majority of compute workloads, but same means with a different end goal. Both will do great!

Frans Bakker@FransBakker9812

$NBIS This is not a flex, these are liabilities. Never has Nebius build large scale data centers at rack densities above, or on par with $IREN. Nebius has made fame a decade ago as a company that supposedly rivaled Google because it was a search machine software 😂 "signing only $3B because you're out of capacity" -> "just wait until they sign Anthropic and surpass $200 per share" Maxed out all capacity for 2026-2027 ✅ Signed deals asap to pump share price ✅ Disclose nothing, absolutely nothing, except topline ✅ Don't use the ATM for 1-2 quarters to make people forget about it ✅ Use convertible notes after the ATM so people completely forget there is one open ✅ Declare yourself the winner of the AI Cloud race at $161 per share ✅ See your NJ site slowdown, opposition accelerate, permits nowhere to be found 📛 Deliver a dumpster fire of a PnL for the remainder of 2026-2027 📉 With all your deals signed and NONE delivered, see the stock start to deteriorate as hot money moves to the next winners that have capacity to sell 📉📉 Well done retail, you played yourself. Chilling and printing turns into: "I have been trading Nebius all the time, vastly outperforming Nebius" (Daniel Koss supposedly traded Nebius because he can predict the stock price rather than understand the fundamentals?, receipts are to be found in the drawer with Nebius deal metrics). Nebius was a great short at $161, but it will do down much further. The market won't have patience for $NBIS to hit their 2028 positive EPS. I am collecting satellite material of the failures they call data center sites at Nebius. I have no problem debating these spreadsheet Europoors who were no different than the guys rooting for $CLSK last year when they were running hot without a chance at profitability. Long $IREN. Proud $NBIS bear.

English

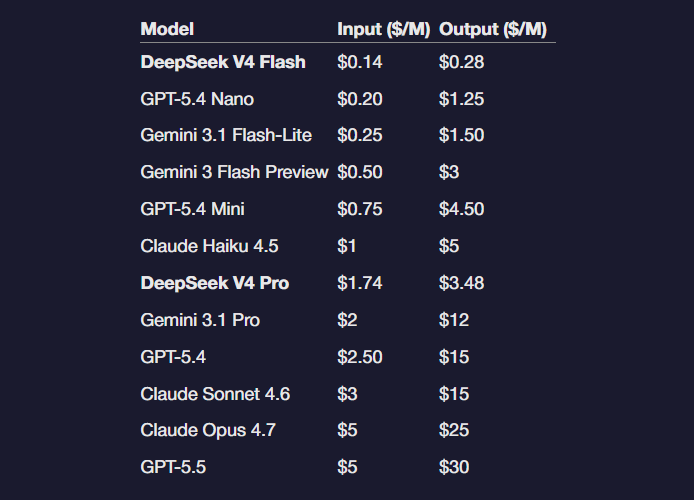

DeepSeek Cuts API Prices by 90%, Runs V4 on Huawei Chips, and Pushes AI Inference Into a Full-Blown Price War

DeepSeek cut API prices by 90% on input cache hits and is offering a 75% discount on V4-Pro until May 5

That takes V4-Pro cache-hit pricing to around $0.0036 per million tokens, while output pricing sits far below Western frontier models charging $12–$25 per million tokens

V4-Pro has 1.6T total parameters, with 49B active per inference pass. V4-Flash is the smaller 284B parameter version

V4 runs on Huawei Ascend chips, not NVIDIA

It also uses far less compute. At a 1M-token context window, V4-Pro reportedly needs only 27% of the compute required by V3.2

Performance is still slightly behind GPT-5.4 and Gemini 3.1 Pro

English