Sabitlenmiş Tweet

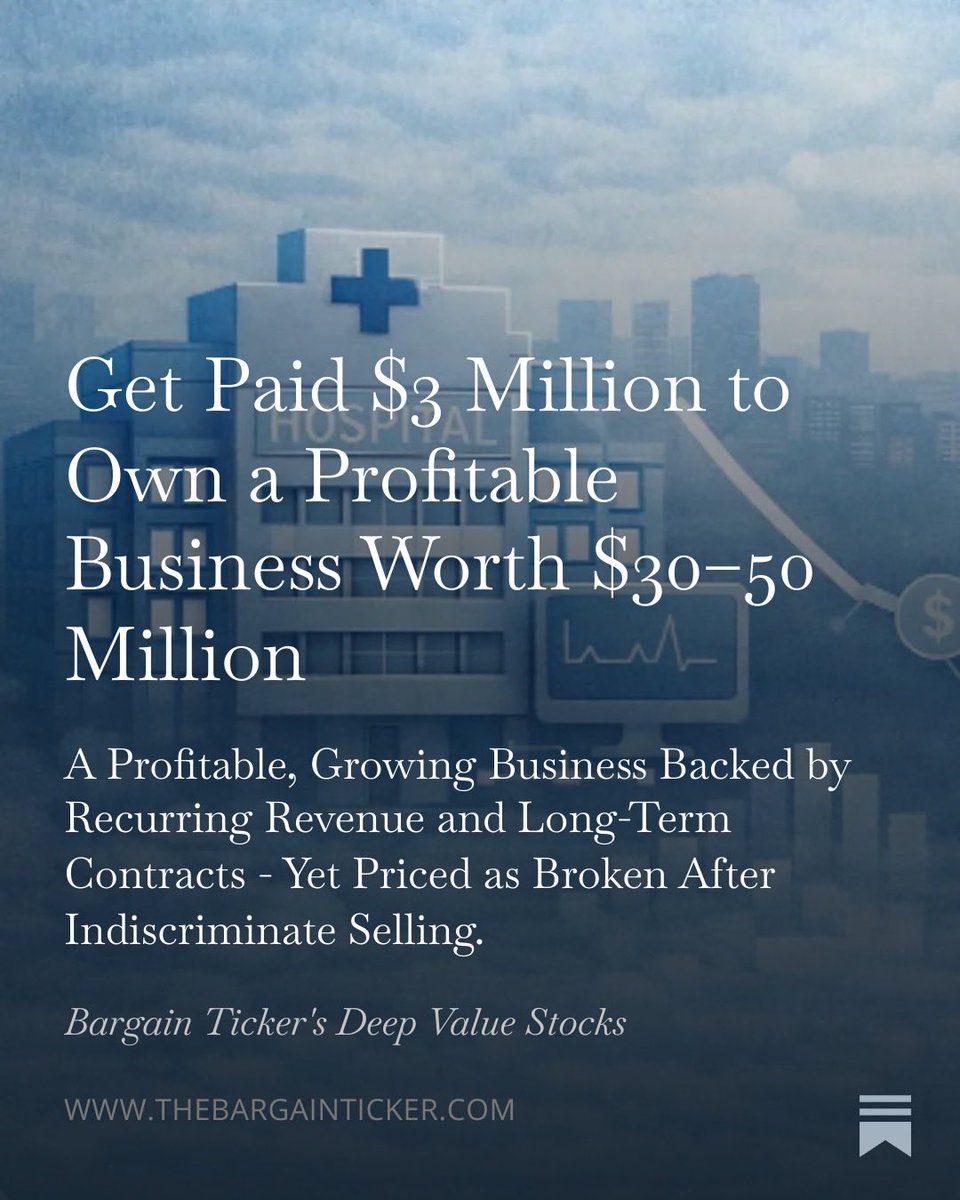

2.3x EV/FCF for a digitally inflecting deep-value security group with recurring cybersecurity growth and substantial underlying real-property value:

- Cost optimized

- Billionaire shareholder

- Unique cross-selling opportunity

My first Substack writeup:

bargainticker.substack.com/p/2x-evfcf-unc…

English