@aleabitoreddit Definitely helped a lot! Thanks again for all your research!

English

0xMerlin

1.4K posts

三个月时间我的 IBKR 账户收益率快接近翻倍了。 一个多月之前我关注了 @aleabitoreddit,顺着他的推文思路,我花了几十个小时时间,研究了整个光互连光通信产业链。 整个过程收获实在是太多了: - 了解学习了光模块、外延、衬底、硅光芯片、CPO、激光器这些新知识,享受学习投研的乐趣。 - 把学到的东西对外输出,做了一期光通信产业链拆解视频,Youtube 播放量接近 20k,一期视频给我的新频道涨了 1.5k 订阅。 - 在研究做好功课之后,小资金建仓了 SIVE/TSEM/COHR/AAOI/LITE 这些光通信标的,作为高风险激进持仓,虽然赚的不多,但已经很满意了。 感谢股神 Serenity!

Taiwan $NVDA CPO supply chain ide #1: Shunsin (6451 TWSE) - Photonics Packaging at ~$1.4B MC. It's a subsidiary of Foxconn. And Foxconn is ODM for $NVDA. It's almost like Celestial got listed by $MRVL and got a free piggy back ride? Some personal est. 2027 fwd ~20 P/E, that compresses harder into 2028, 2029. Shunsin's optical division openly lists their markets as "CPO 51.2T/102.4T" and "Pluggable XCVR 800G/1.6T. Markets themselves as "Supported by Foxconn's vertically integrated supply chain for fast project ramp" If you look at $TSM COUPE for $NVDA, they don't assemble final fiber arrays/racks, Foxconn does. So $NVDA's CPO networking gear probably goes through Shunsin's alignment and bonding machines? And $GOOGL, $META optical switches probably end up thorough them too since they scaled Vietnam CPO facilities (speculative). Basically you get a free Foxconn piggy-back ride with this company at low forward multiples. Disclosures: I am personally long.

I started 2 relatively small positions on $LPK and Unitika last week. Why small? 1. $LPK up 17% so far today 2. Unitika down 18% today I am building my positions slowly on both via DCA. (Like with any stock). You're never going to have the best avg. price with this method, but it helps smooth out short term volatities. And it stops me checking my account 72 times a day. Also yes, I did buy more $LPK following my "bear" thesis the other day lol.

Just for the visual learners about CPO: This is what the CPO market growth looks like from GS + $LITE transcript confirmations. There's certain names that are very high-beta correlated to CPO. Maybe... not the best idea to copy firms named after Orange Peels on $AAOI to $SNDK to short names. At the very beginning or middle of supercycles? Especially if you're retail, live in Europe, and only look at last 12 months revenue instead of forward growth.

Just reiterating my disbelief: I have never seen a sector more bullish than CPO. GS reported Optical TAM 9X from $15b in 2026 -> US$154b in 2028 CPO making up $91B of that. Starting from ~$164M (Modor for 2026 / sampling) to $91 Billion (GS 2028) 55,000%+ CPO growth curve starting from today This is exactly why algorithms / analysts mess up because they might look at TTM revenue at these CPO names. But everything happens in the next two years with $SIVE to Shunsin to MSSCorps to $SOI. This is Zero to 100 from a massive architectural shift pushed by $NVDA. I genuinely still don't think retail or markets understand what's coming yet.

@aleabitoreddit Thanks for consistently sharing … must be tough having a lot of people ping you lol You think this causes any delays / issues to you $sive thesis long term given the delay to the celestial roadmap? Looking to position on $sive on market open tomorrow

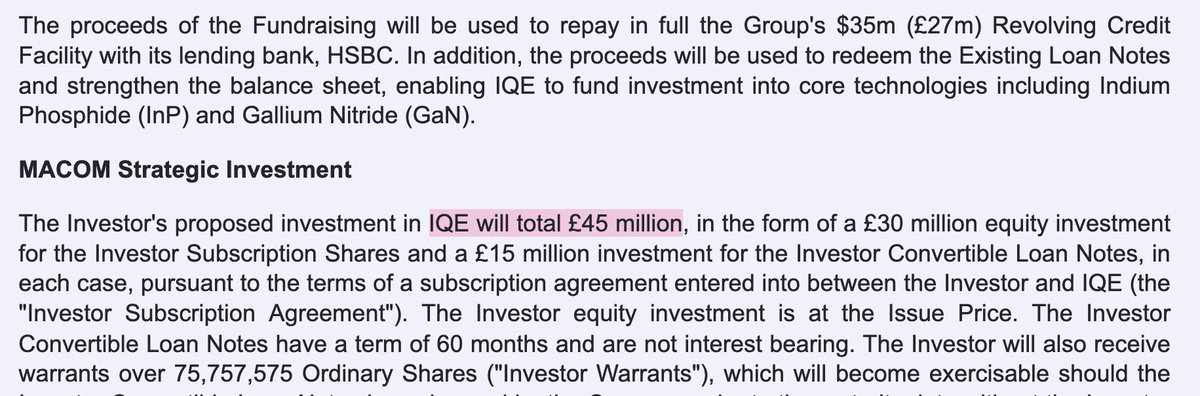

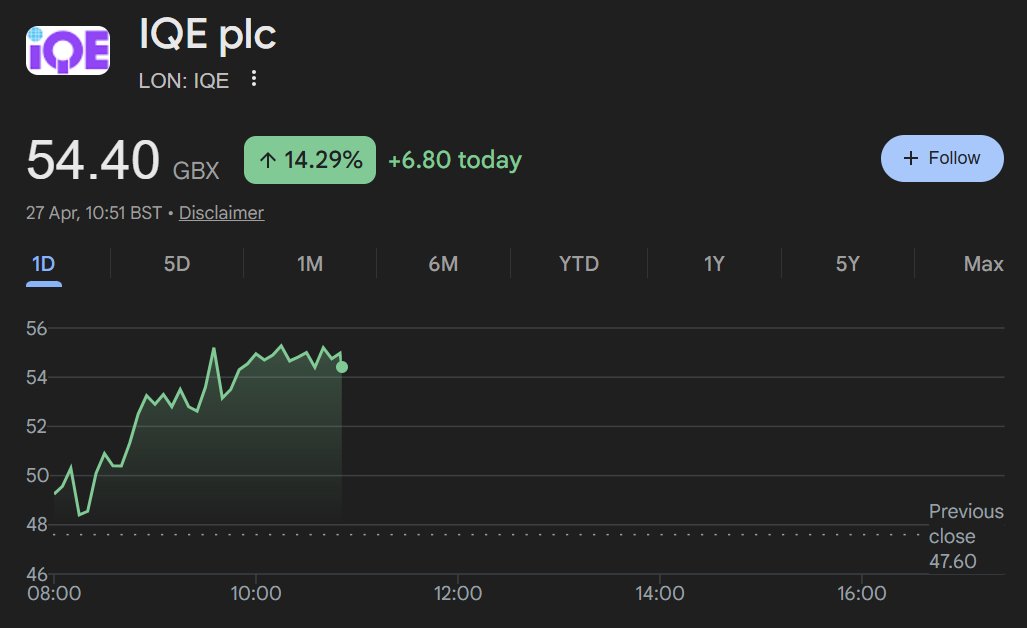

“ $IQE dropped 20%. Shall I sell?! ” No. I added heavily to my position on last week's dip. Summary on why I'm adding to my $IQE position on any dip: 1. Upstream supply chain tailwinds: $IQE's photonics & GaAs segments rely on $AXTI's substrates. $AXTI guided “sequential revenue growth in Q1 2026, driven by growth in InP for the AI infrastructure build-out.” With InP backlog >$60M and plans to 2x capacity in 2026. Since InP substrates are crucial for 1.6T transceivers and CPO: $AXTI's capacity ramp directly removes any chokepoint for $IQE's photonics epi output. And still, $IQE has internal substrate manufacturing capabilities in UK/USA - which produces GaAs, InP, and GaN. 2. Downstream demand sold out: $LITE are $IQE's flagship customer (multi yr VCSEL/EML epi partner): - $LITE has its hyperscaler order book sold out through 2028. - $LITE CEO said “we’re falling further and further behind the demand” - With agreements locking multi yr visibility straight into $IQE's photonics segment. - $NVDA $2B+ investments in $LITE & $COHR signal hyperscalers are locking in capacity yrs ahead, with epi being a huge bottleneck. $LITE's VCSEL & EML epiwafers are exactly what $IQE grows on InP/GaAs. So, locked-in multi-yr volume + sold out book = multi-yr revenue for $IQE's photonics segment. Then you also have $QRVO + $SWKS as $IQE customers for GaAs/GaN epi. It’s less obvious, but $AVGO also source GaAs/GaN epiwafers from $IQE too for its RF business - even while maintaining captive InP epi capabilities for its photonics products. 3. $IQE are an irreplaceable foundry: - patents on epi wafer growth processes (GaAs, InP, GaN) - 35+ years of proprietary tuning for yield/defect control - $IQE Serves everyone ($LITE, $COHR, $AVGO, etc.) without competing downstream - Chinese players face Western export/qualification walls 4. $IQE is different to competitors (and superior): - Substrate specialists (e.g. $AXTI): Sell raw wafers and lack $IQE's IP. - Vertical integrators ( $COHR, $WOLF, Sumitomo): Do some in-house epi but still outsource for flexibility. $IQE is purely neutral foundry - broader access, no channel conflict. - Asian players (e.g. IntelliEPI): Cost-competitive in GaAs but lack Western defence quals + geopolitical risk. $IQE wins on yield, reliability, and secure supply. $IQE's differentiation is pure-play scale + IP + global compliance = “safe” supplier for customers ----- MC forecast: I personally forecast $IQE to >2x until end of 2026 to ~£1.1B MC. Driven by photonics tailwinds materialising + strong execution - $LITE's 2028 sell-out + $AXTI's capacity doubling signal sustained (and accelerating) epi demand. Then any sale of their Taiwan ops would carry a further premium on top (Board are already encouraging bids). Imo, the 20%+ drop last week was just noise r.e. Iran, and nothing to do with fundamentals.

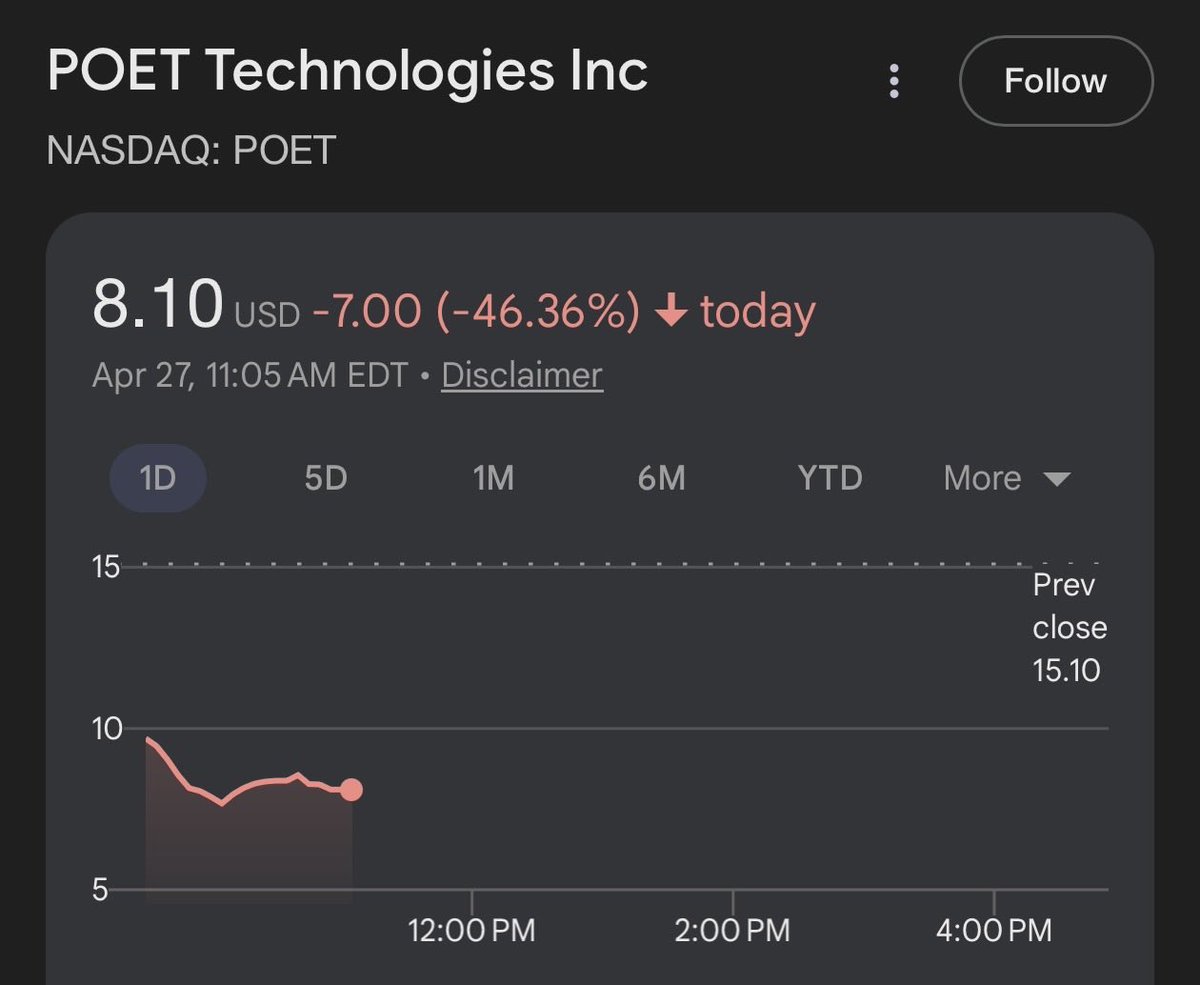

THE 7 LAYERS OF PHOTONICS 1. Materials & Wafers (substrate layer) $AXTI, $IQE $WOLF, $COHR, $LWLG 2. Tools (fabrication layer) $ASML, $AMAT, $LRCX 3. Lasers (light generation layer) $LITE, $COHR, $LASR, $SMTC 4. Foundries (manufacturing layer) $TSM, $TSEM, $GFS, $UMC, $INTC 5. Test, Inspection & Packaging (reliability layer) $AEHR, $VIAV, $ONTO, $AMKR, $FN 6. Optics (module layer) $AAOI, $POET, $GLW 7. Networking (connectivity layer) $CRDO, $MRVL, $AVGO, $ANET, $CIEN

@aleabitoreddit Missed the opportunity to make money by investing in photonics. Do you think there is 50% upside from here?