Biotech_Jack

1.1K posts

Biotech_Jack retweetledi

I guess the drawback of becoming the $ABVX guy is that I've got to respond to ridiculous takes as they pop up now. Wedbush is making a full time job of it.

Their recent note tries to catastrophize about steroid tapering (or lack thereof) in the phase 2 dataset, claiming this undermines $ABVX's probability of success in phase 3. If you're not in the weeds on the data here, I could see how you might read that and think "oh no, that doesn't sound good".

However, if you *are* remotely in the weeds on these data (as Wedbush should be but very clearly isn't), you can read that take and laugh at the analysis - so let's bring everyone into the weeds here.

First of all, it's funny that Wedbush is apparently just now stumbling across this contrived bear thesis that they're pretending is something new, because THE DATA THEY ARE TALKING ABOUT WERE LITERALLY PUBLISHED ***BEFORE*** THE PHASE 3 INDUCTION DATA CAME OUT IN JULY. The publication was from May, and it mostly rehashed data that were actually already widely known for years from ABVX's prior conference presentations and corporate decks.

Welcome to the party, Wedbush - it's been going on for a while. Have a seat.

Ok so what's the supposed issue? Wedbush is saying that ABVX didn't force tapering of steroids in the P2 maintenance trial, which is standard practice in P3 trials. The issue is.....Not forcing steroid tapers *is standard practice* for P2 trials...which is exactly what ABVX did, in line with standards...

In my ABVX pitch from July I discussed comparing their maintenance dataset to two of the most robust comparison P2 studies - those from Zeposia and Velsipity. These are great comps because these drugs are all oral and all of the P2s had open label maintenance portions.

Oh, and also...none of the trials forced a steroid taper...because that is standard!

The Zeposia study literally didn't even MEASURE steroid free remission (ABVX and Velsipity studies at least measured what the steroid free remissions were, but none of them forced any tapering).

So, not only is Wedbush making a fuss out of a dataset that has been around since $ABVX was trading at $6/share, but what they're complaining about is just flat out standard practice...yet they're acting like it's some sort of new discovery that undermines the drug's activity altogether...after it just reported the 3rd highest UC induction remission delta of all time...Ok.

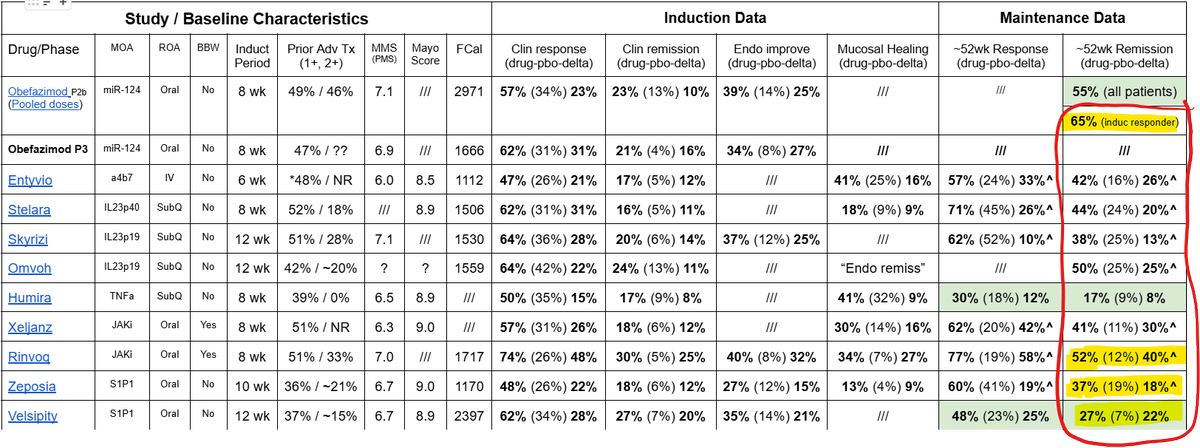

I'm going to point everyone to this table (attached) yet again. As most will likely know by now, only induction responders enroll into the maintenance portion of UC P3s, so for $ABVX, the P2 maintenance remission number we look at is that 65% number on the far upper right corner (which was the P2 maintenance remission rate among patients who had responded upon induction).

Take a second to compare that 65% number to the numbers below it from other P3 trials. 65% would be, by far, the single highest number ever recorded in a phase 3, and it wouldn't even be CLOSE. 65% would literally DOUBLE the remission rates of some of the other (approved and used) drugs on that list.

Nobody (absolutely no one) believes $ABVX is going to repeat 65% maintenance remission in P3. Yes, that is the appropriate responder-enriched number from the P2 that will be represented in the phase 3, but the P2 was open label, and yes, in P3 steroids will be forced to taper.

Look how much room they have for that number to get worse! It could drop 12% points and still be the highest remission rate of all time (which is by no means necessary for success here). The P2 maintenance remission data were so otherworldly good that we already all know the number has to come down in P3 - no way around it. All the bulls have known this all along (just like we all understand the basic drug design of UC trials which involves forced steroid tapers in P3 but not in P2...apparently unlike some).

But, of course, the placebo adjusted delta is ultimately what will matter in P3. 20-30% delta has been broadly discussed as the target range for $ABVX, and I completely agree (as I said on the YAVP podcast last week, my guess is a middle ground bet on 25%).

How hard will that 20-30% target range be to hit? Let's assume that the placebo remission rate mimics that of the R+Z+V dataset combining 3 of oral therapies on that table. The average placebo remission rate among those trials was 12.7%.

If we assume ABVX has the same placebo remission rate in maintenance (which may not be fair as ABVX's placebo remission rate in induction was *lower* than the R+Z+V average), then $ABVX would only need a 32.7%-42.7% remission rate on drug to "hit the bar". Again, this is versus the 65% achieved in the open label P2...

Wedbush tries to sensationally mislead investors into thinking that "1/3" of the remissions in the P2 were just "due to steroids", simply because 1/3 of the patients in remission had not come off of steroids. This is inherently misleading in the first place because there was no forced taper of any kind on the study, meaning patients in remission may not have even *tried* to come off of steroids. If there was a forced taper, without a doubt at least *some* of those 1/3 of patients who stayed on steroids despite not attempting a taper would have stayed in response when coming off of them. Of course not all of them, but SOME of them would have maintained remission despite a forced taper. So, that 1/3 number perhaps becomes 1/4 or 1/5 if a forced taper were implemented.

But, ok. Let's play along with Wedbush's game anyway and just stick with the phony 1/3 number and say "Ok, take away 1/3 of the remissions due to steroid taper in the P3!

1/3 from 65% is...43.5%...

So, 43.5% less our estimated placebo response rate of 12.7% and we've got...30.8% remission delta! Literally HIGHER than the high end of the bar! And hey, that would beat Xeljanz to make $ABVX the 2nd highest maintenance remission delta of all time...only behind Rinvoq!

So, I guess that all I have to say to Wedbush is...Thanks! Thanks for once again thinking you found something bearish that actually just serves to prove the point for the bulls.

Now please cut this out so I don't feel compelled to address such silly work.

Adam May@A_May_MD

Lot's of requests to discuss the Wedbush report on $ABVX today. It's a doozy. Obviously I'm a biased bull so sure, take my thoughts with a grain of salt, but this is truly, awful work from my perspective. Let's dig in on a few of the key issues.

English

Biotech_Jack retweetledi

Biotech_Jack retweetledi

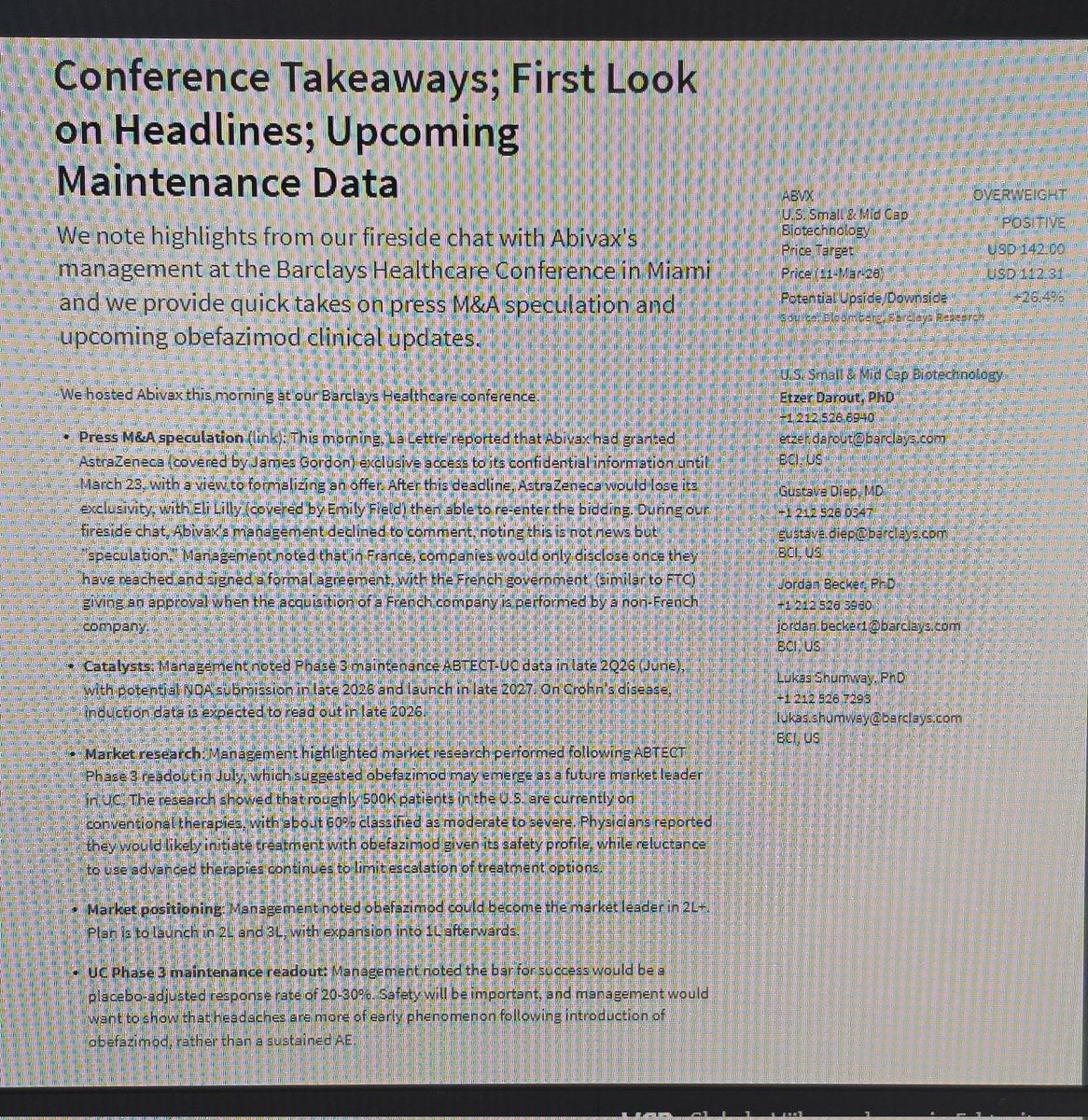

$ABVX Jefferies: The hiring of a chief commercial officer is a “strong step” toward launch preparations. It’s a “strong validation” for obefazimod’s launch potential. The latest safety update is clean, “as expected,” while the completion rate “bolsters confidence” into the maintenance trial results expected in late 2Q.

English

Biotech_Jack retweetledi

Michael Nesrallah ($ABVX), the new CCO, brings Takeda’s expertise (Entyvio) to the team. The IBD veteran, with a background at Novartis and McKinsey, is securing the standalone path.

English

Thanks to @AndrewRangeley for having me on Yet Another Value Podcast!

Mostly chatted about $NKTR and $ABVX, which I know someday people will get tired of hearing me talk about, if they aren’t already 😅

Yet Another Value Empire@YetAnotherValue

Podcast #378 is up! @A_May_MD on investing in biotech, $NKTR, and $ABVX yetanothervalueblog.com/p/adam-may-on-…

English

@CatPunksters $ABVX is weapons-grade material. The miR-124 payload is too precise for conventional defenses. Whoever leads the first strike wins the field. "France is delivering strategic superiority while the opposing side is retreating.

English

@CatPunksters $ABVX is the clear 1.01 prospect. 9.99 RAS score and 40+ vertical in trial data are elite tape. Who trades up before the deadline? The team with the exclusivity must use the pick before the competition steals the franchise player.

English

$ABVX I’d be in favour of that too

Adam May@A_May_MD

@Agent0088156721 I'm 100% on board with $ABVX hiring a CCO/commercial team. AFAIC this is all part of negotiating leverage to be able to say "we are going to launch this drug on our own if we don't get a fair price today" - and to mean it too. Worked out *beautifully* for $VRNA.

English

@thirdcoastip For Sanofi, Abivax is more than just an investment; it is an insurance against the decline after Dupixent. While AstraZeneca may be rational, Sanofi could overpay out of strategic necessity.

English

@biotech_jack Fine by me! At the least the threat of this can sharpen a LLY offer too

English

$ABVX Forgot about 3/23 "deadline" and look at it this way -- Marc to LLY right now: AZN has my data room until March 23. 90% DSMB all good. Garijo takes Sanofi's chair April 29. French buyer. No FDI. 60-day close. €15B was a cute opening bid. Call me with your best #, cough 19B

English

@smithy05261244 $ABVX Keith Fournier (PhD RAC) secures the standalone path. With AbbVie/Takeda's FDA expertise, he guarantees error-free NDA processes and regulatory compliance. His network is the foundation for the approval of Obefazimod.

English

@smithy05261244 The fact that he is already on board while a CCO is now being sought shows that the scientific basis (regulatory) is already in place and that the commercial phase is now beginning. 2/2

English

$abvx

One of the strongest signals coming out of management’s recent 1:1 investor meetings ( this has been well known for over we week !!! ) is the upcoming CCO (Chief Commercial Officer) hire, which will be formally announced Monday inside the FY 2025 earnings press release.

This is textbook Eric Tokat.

Back in his pre-JPM interview on Bio TV (the panel with Marc de Garidel), Eric Tokat from Centerview Partners laid out exactly this playbook for biotech CEOs negotiating with Big Pharma:

When you’re in advanced discussions, the smartest move is to accelerate commercial build-out early. Hire top-tier commercial leadership, start putting launch infrastructure in place, and publicly demonstrate that you are fully prepared to commercialize the asset yourself if the deal terms aren’t right.

Why does this work so well?

Because it instantly flips the leverage.

Potential acquirers realize you have a credible Plan B. That confidence usually forces them to come back with far more serious offers instead of trying to low-ball or drag their feet.

Abivax management is executing this strategy to perfection right now:

• They immediately denied the La Lettre exclusivity rumor and told the outlet to stop running with it

• They’re bringing in a CCO well before the pivotal maintenance data readout (late Q2)

• They’re already messaging a post-maintenance equity raise while keeping a bullish but disciplined tone on expectations

• They’re deliberately “insulating” the company with real commercialization prep — just in case they decide to go it alone

This is not the behavior of a company desperate to sell at any price. This is a sophisticated team strengthening its negotiating hand ahead of what could still turn into a competitive process once the rumored AstraZeneca exclusivity window closes on Monday (March 23).

Add in Mondays expected clean DSMB update (90% of patients completed — biggest safety dataset yet) plus the cash runway confirmation, and Monday’s earnings release is shaping up as a very constructive catalyst for the story.

At the end of the day, Abivax still sits with one of the highest-quality late-stage immunology assets out there — with multiple paths forward and real optionality.

Management is playing this exactly right. Smart execution all around.

English

@adamfeuerstein $LLY poor management. In Germany, they say: a ‘NEIN’ from the customer means "N"och "E"in "I"mpuls "N"ötig"

English

Some interesting comments from Jacob Van Naarden, $LLY head of business development, at STAT's Breakthrough Summit East event yesterday:

On deal volume: Jake, himself, is seeing approx 10 deals per week, ie deals that are important enough, or diligenced enough, to cross his desk.

"We are making more offers than you can possibly imagine. Either me personally or members of my team are making between three and five offers a week to either license something or buy a company or do some kind of discovery deal. Of course, you haven't read about all those because they don't all end up happening..."

Why don't all these deals get done?

A lot of deals are small, or involve private companies or preclinical assets, are not press released, etc etc...

However, when it comes to public company deals...

Jake:

"What's interesting is how many of the multi-billion dollar deals we are attempting to do, and sort of get rebuffed with some frequency..."

He added...

"We engage with a lot of publicly traded companies... and those are the ones where I'm particularly surprised you put sort of a market premium offer on the table, and you're not even granted a conversation, so to speak, as you have a conversation, but it sort of doesn't go anywhere. That's pretty surprising, and that's that's happening more frequently than I would have expected."

English