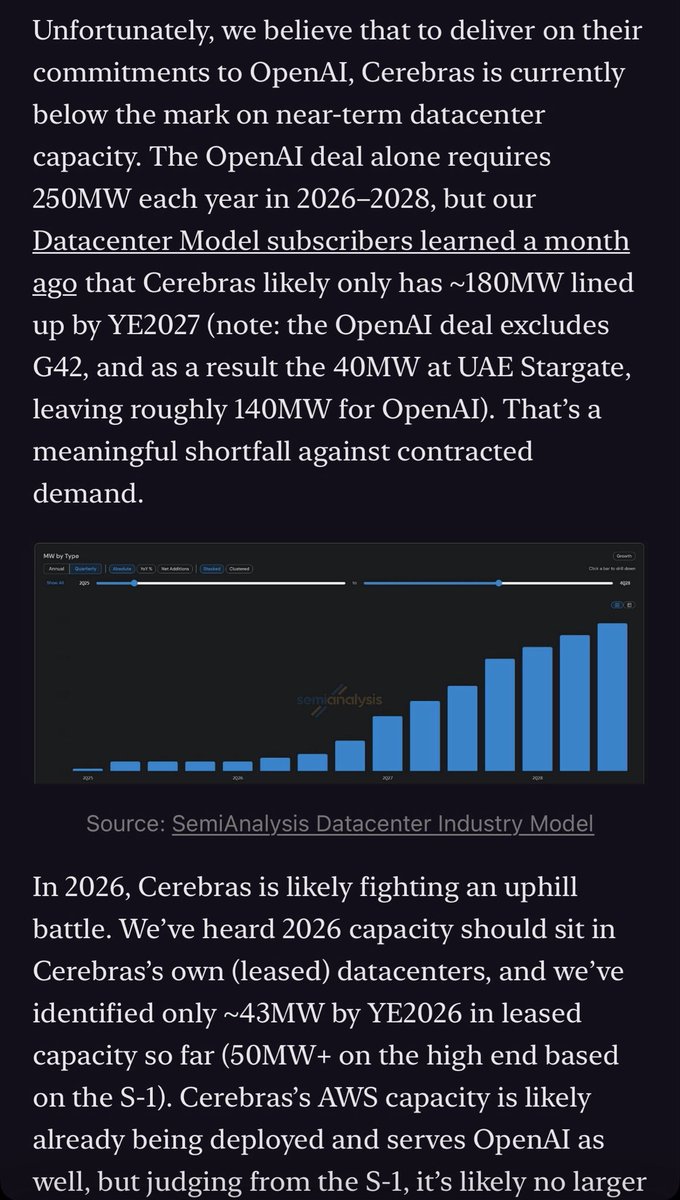

If I’m a smaller miner like $SLNH $BDGE looking to convert my existing capacity to HPC Cerebras feels like a company you have to be targeting aggressively. $DGXX and $WYFI already on board and are in a strong position to be able to have Cerebras take incremental capacity.

English