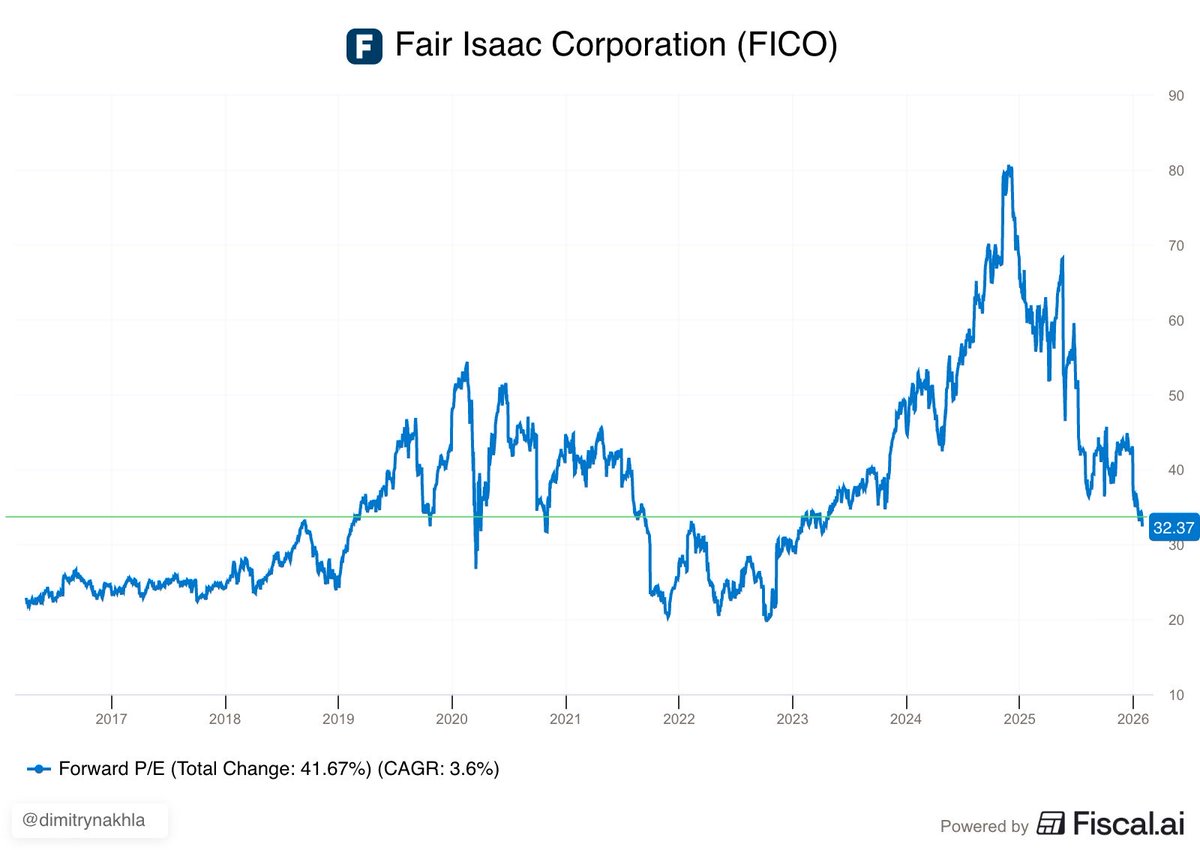

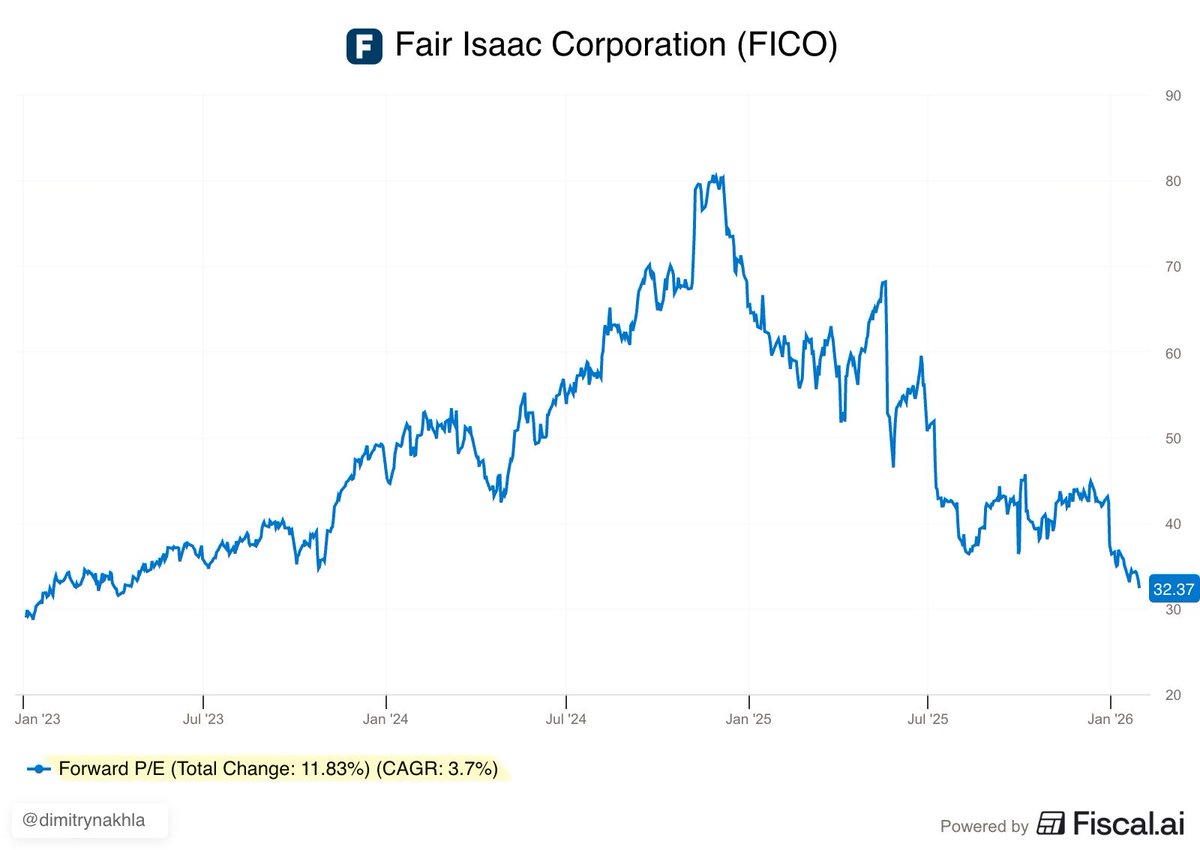

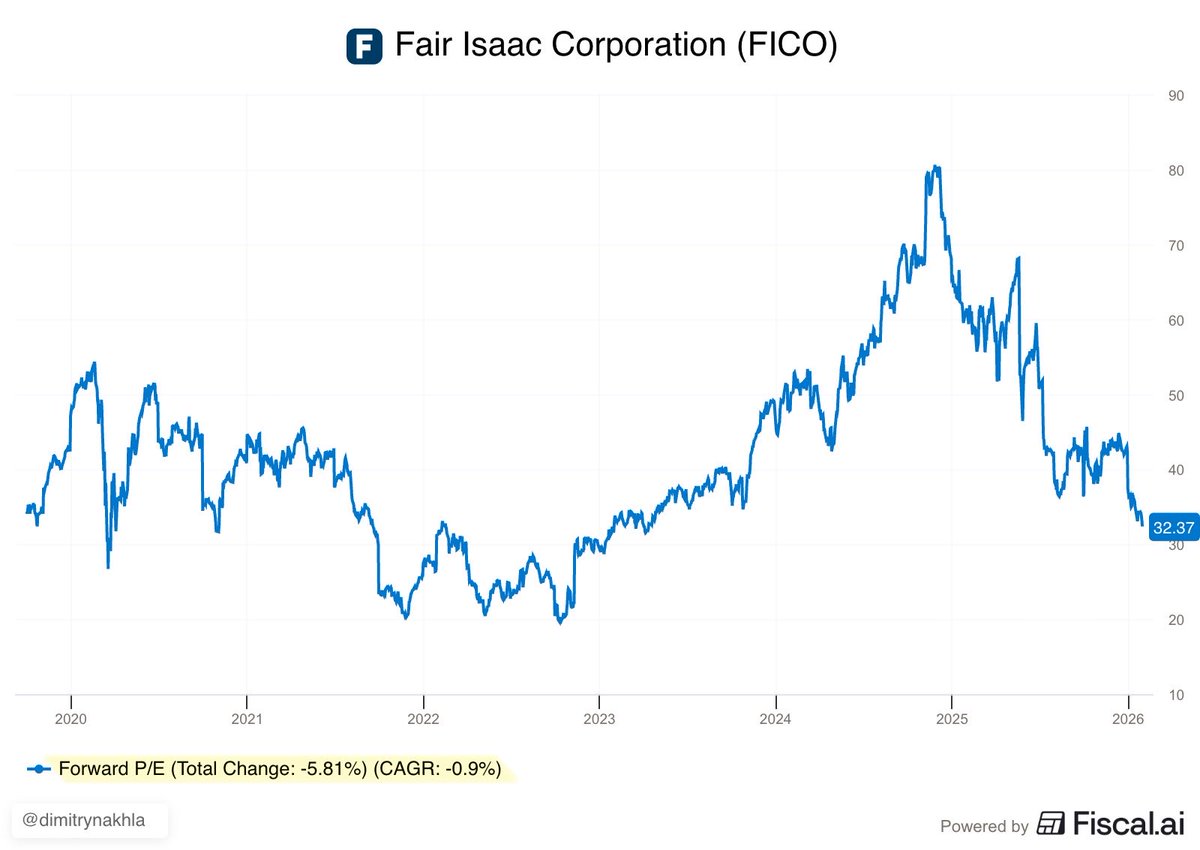

@DimitryNakhla In light of current fallout with FHFA, does FICO fall under same category? Or the leader has been careless?

English

The D 💙

407 posts

@bossD1007

Anaesthesist. Man Utd. Indian.

Had a very pleasant long call with my new friend @DimitryNakhla today. Sharp guy, runs a meaningful amount of money, thinks independently and has a good sense of humor. If you’re not following him, you should. 🌹