Sabitlenmiş Tweet

Portfolio update – April 1, 2026 📊

11 positions – Top 5 cumulated weight = 65%

Bought: $NOW

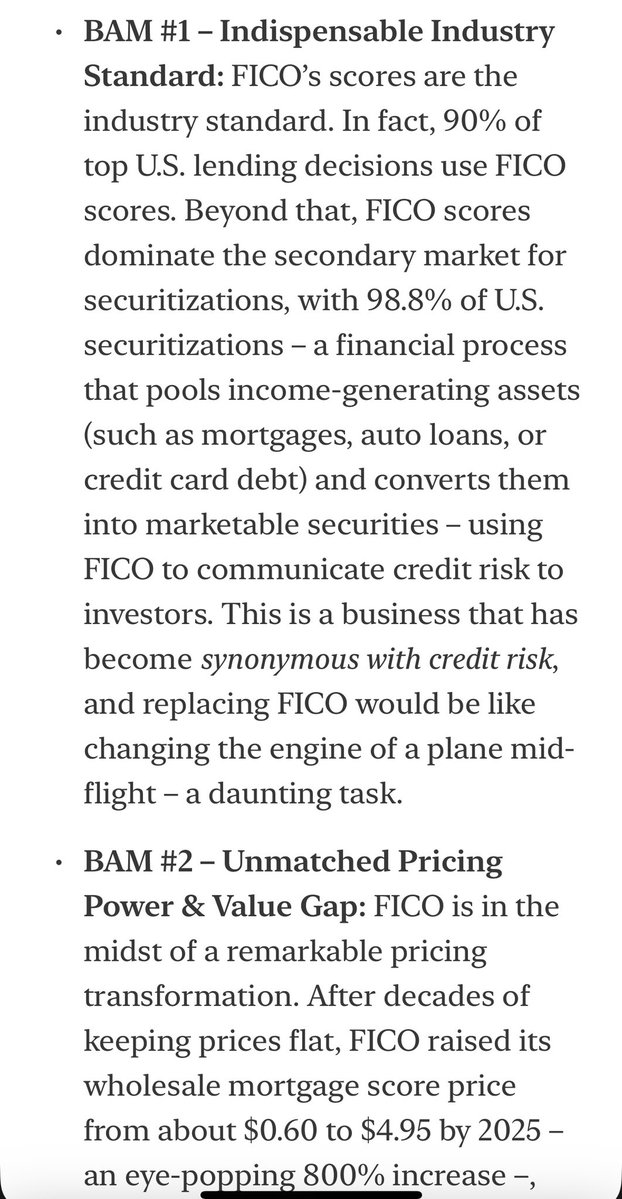

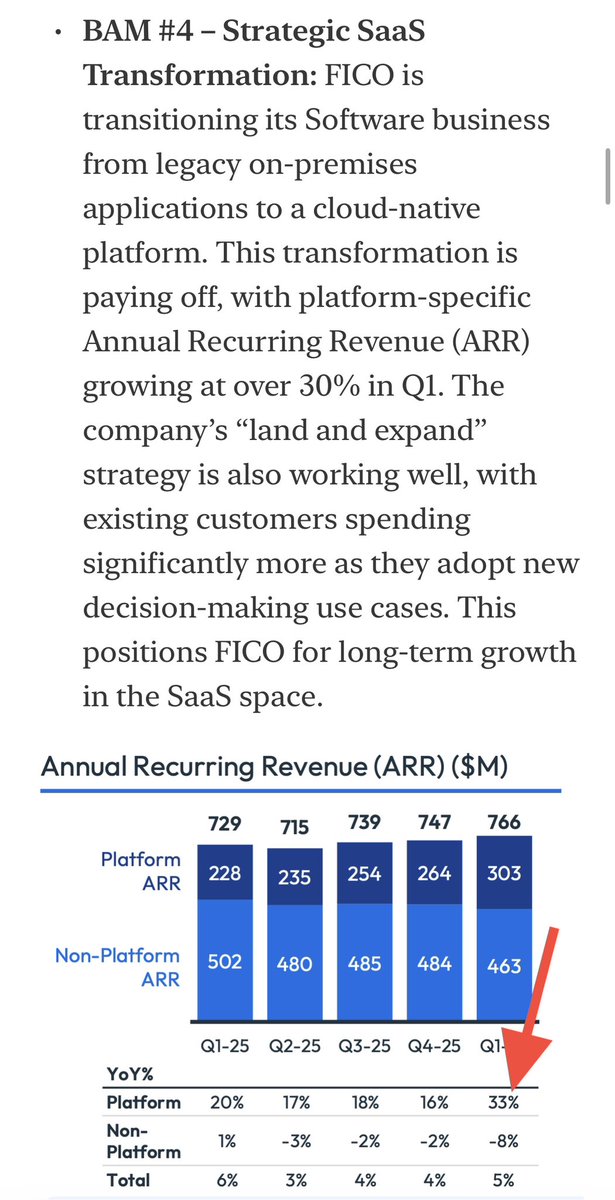

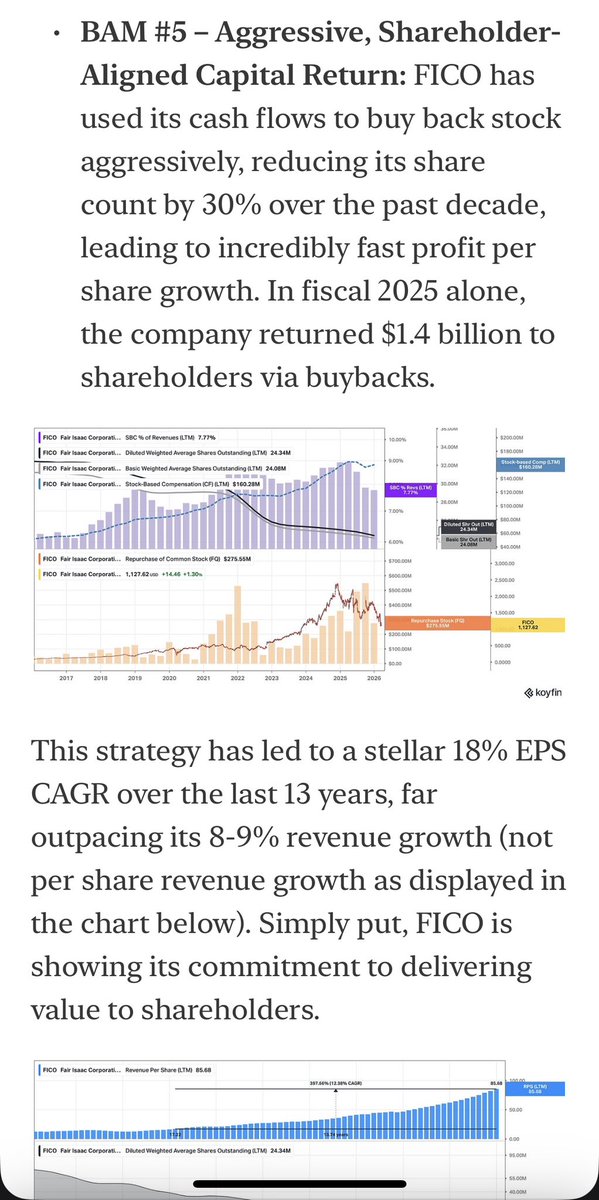

Added: $MA, $SPGI, $FICO, $UBER, $V

Sold: $NVDA

Trimmed: /

A few thoughts ... 🧵👇🏼

English

The Long AJ

5.1K posts

@TheLongAJ

Equity Investor | Collecting Compounding Machines

1/13 $DLO has become one of the more interesting companies in global payments. Since its 2021 IPO, the stock is down -82%, while Revenue & EPS have grown at 35% and 19% CAGR (2022-LTM). Today it trades at 15x earnings and a 6.4% FCF yield. Is this an opportunity or trap?

Ça peut aller dans les deux sens… +4.2 % pour mon portefeuille aujourd’hui !

On se ferait pas un thread des threads par hasard ? 🫣 Ma série complète #SaaSpocalypse : • L'analyse SaaSpocalypse • L'analyse des entreprises : Salesforce, Adobe, UiPath Un Thread🧵 📃 Analyses éducatives uniquement. Pas de conseil d’investissement. ‼️