The Analyst@the_analyst_24

📡 AmpliTech Group $AMPG: The "Silent Engine" of 5G & Quantum is Revving Up! 🚀

AmpliTech Group isn't just a component maker; it’s becoming the backbone of US-made 5G infrastructure.

After a deep dive into their tech and market position, here is why $AMPG is a key player to watch in 2026. 🧵👇

1. Company Profile 🏢

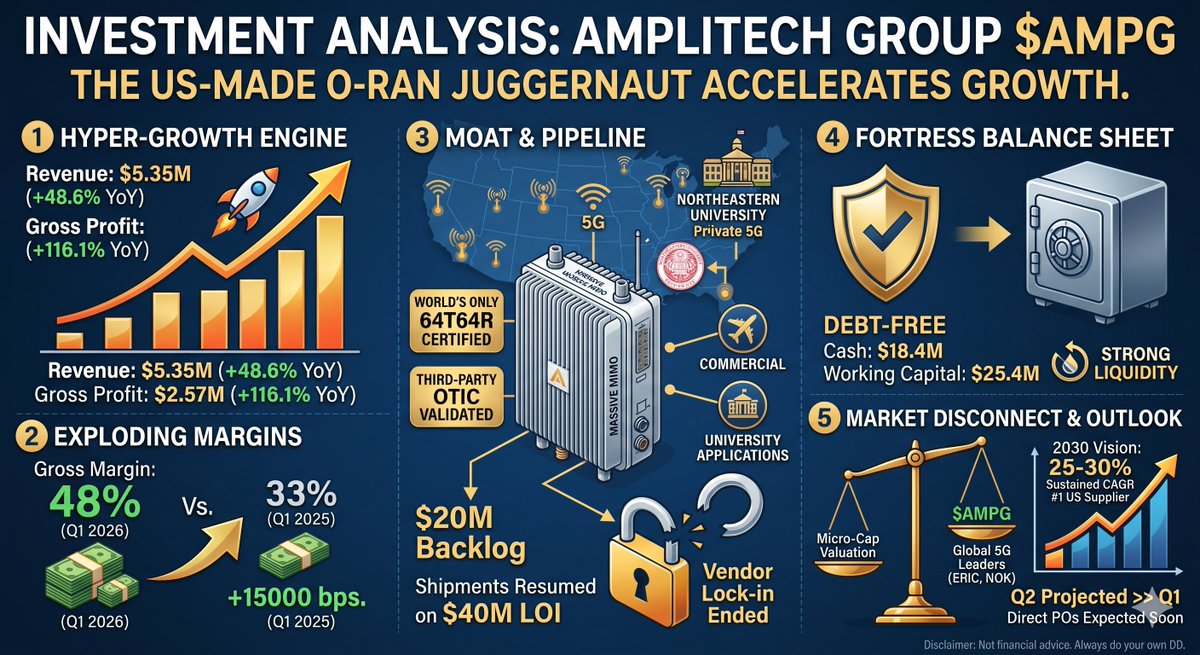

a. The Company: Based in New York, AmpliTech $AMPG designs world-leading signal processing tools. From satellite links to 5G and Quantum Computing, they solve the "noise" problem in wireless data. b.

Shareholder Structure: Strong alignment with a ~12.6% insider stake (led by Founder/CEO Fawad Maqbool). Institutional backing (~22%) from giants like Vanguard provides a solid floor.

2. The Product Edge: Why they win 🛠️

The "LNA" Secret: Their Low Noise Amplifiers offer the world’s lowest noise figures. Better signal purity = more range + less power consumption.

O-RAN First: The first US company with a certified 64T64R MIMO radio platform. This is the "Open RAN" holy grail that allows carriers to break free from proprietary hardware lockdowns.

Beyond Earth: Their "Space-Qualified" tech is built for the vacuum of orbit, while their Cryogenic amps power the sub-zero world of Quantum Computing.

3. Valuation Snapshot (March 2026) 📊

Market Cap: ~$65.65M (Still a micro-cap with massive upside).

Enterprise Value (EV): ~$57.26M.

Net Debt: -$8.39M (Strong cash position, effectively debt-free).

EBITDA: Positive momentum started in late 2025; scaling rapidly now.

4. Earnings & Growth 💰

2025 Performance: Revenue hit ~$25M+ (160% YoY growth).

2026 Target: On track for $50M+ with a pivot to full-year profitability.

The Pipeline: A massive $118M in LOIs (Letters of Intent) provides huge revenue visibility for the next 24 months.

5. The "Ericsson" Factor & Peer Group 🔍

While peers like Airgain or Eltek focus on standard RF, $AMPG is a prime M&A target.

The Synergy: As Ericsson $ERIC shifts to O-RAN (notably the $14B AT&T deal), AmpliTech’s US-made, certified hardware is the "Perfect Match" to fill their hardware gap.

Growth: Outpacing the industry average with a projected 44% revenue CAGR.

6. Forecast 2030 🔮

Vision 2030: Targeting a 25-30% sustained CAGR.

Goal: To be the #1 US-based supplier for domestic 5G/6G infrastructure, leveraging "Made in USA" incentives like the CHIPS Act.

7. Opportunities & Risks ⚖️

✅ Wins:

Strategic O-RAN lead, high barriers to entry in Cryo-tech, and a clean, debt-free balance sheet.

⚠️ Risks: Small-cap volatility, execution risk on the $118M pipeline, and competition from global giants.

8. Conclusion 🏁

AmpliTech is a "Small Fish in a $20B Pond." With its unique ability to serve both the ground (5G) and space (SatCom) segments, it is perfectly positioned for the next era of connectivity.

Whether as a standalone grower or a takeover target for a giant like Ericsson, the value is clear.

Disclaimer: Not financial advice. Always do your own DD.

#5G #QuantumComputing #StockMarket #AMPG #Investing #ORAN #Ericsson #TechStocks #SpaceEconomy #MadeInUSA

globenewswire.com/news-release/2…