Sabitlenmiş Tweet

Mega Man

1.6K posts

Mega Man

@callah32

🔌 Energy Infrastructure CORZ IREN CIFR WULF - BITF MIGI? monetize Mw’s • Special situation • equity investor • Debt finance • Michigan State alum

Money priner Katılım Nisan 2012

1.7K Takip Edilen717 Takipçiler

$IREN just landed H5-9 Air-Cooled GB300s for Microsoft Horizon (likely Childress Phase 5-9). Key numbers: Total Contract Value: ~$9.7B (5 years, 20% prepayments) + software licensing ARR: $2.1B from this deal (part of $3.7B total guidance) GPU Costs: 85K B300s = $5.95B-$6.4B

English

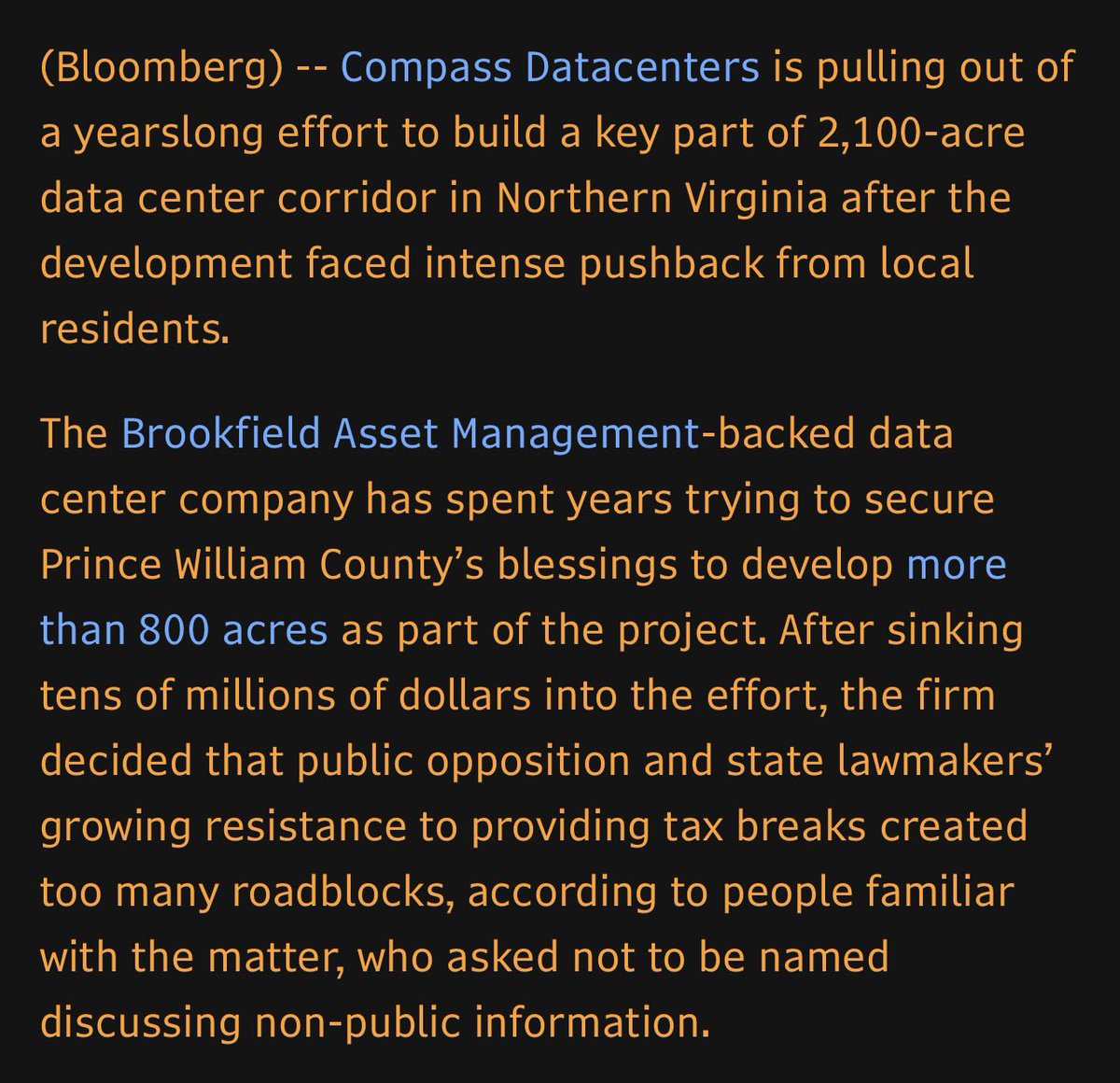

Huge. A Brookfield-backed datacenter company is pulling out of a major project in Virginia, that they had been working on for years, due to growing political opposition bloomberg.com/news/articles/…

English

@pdicarlotrader So regarded. No such thing as TA when a deal drops. TA trap lol

English

After a +50% run in a month, $IREN now looks like a classic retail trap. 🔻

In this video I walk through:

• Why I exited

• How these traps form in the market

• My worst case roadmap for $IREN

Watch this before your next trade.

English

@cantonmeow not enough pivot history (frames) these are not TA stocks. Driven by explosive deals vs the mundane

English

I didn't think $IREN break out of the trendline when I look at log. It got rejected.

But it's getting closer to support below at a slightly rising 20 week SMA.

English

@DonnyDyor @wallstengine Seriously tho, why can’t FCEL scale / deploy like BE? Legit curious the differences

English

Oracle said it will now power its Project Jupiter campus in New Mexico with up to 2.45 GW of Bloom Energy $BE fuel cells instead of gas turbines and diesel generators. The switch cuts NOx emissions by about 92% and keeps the AI data center on a single microgrid campus.

English

Mega Man retweetledi

Where power becomes intelligence.

NVIDIA GB300s arriving at Childress for our Microsoft Horizon deployment. Big effort from the team. $IREN

Childress, TX 🇺🇸 English

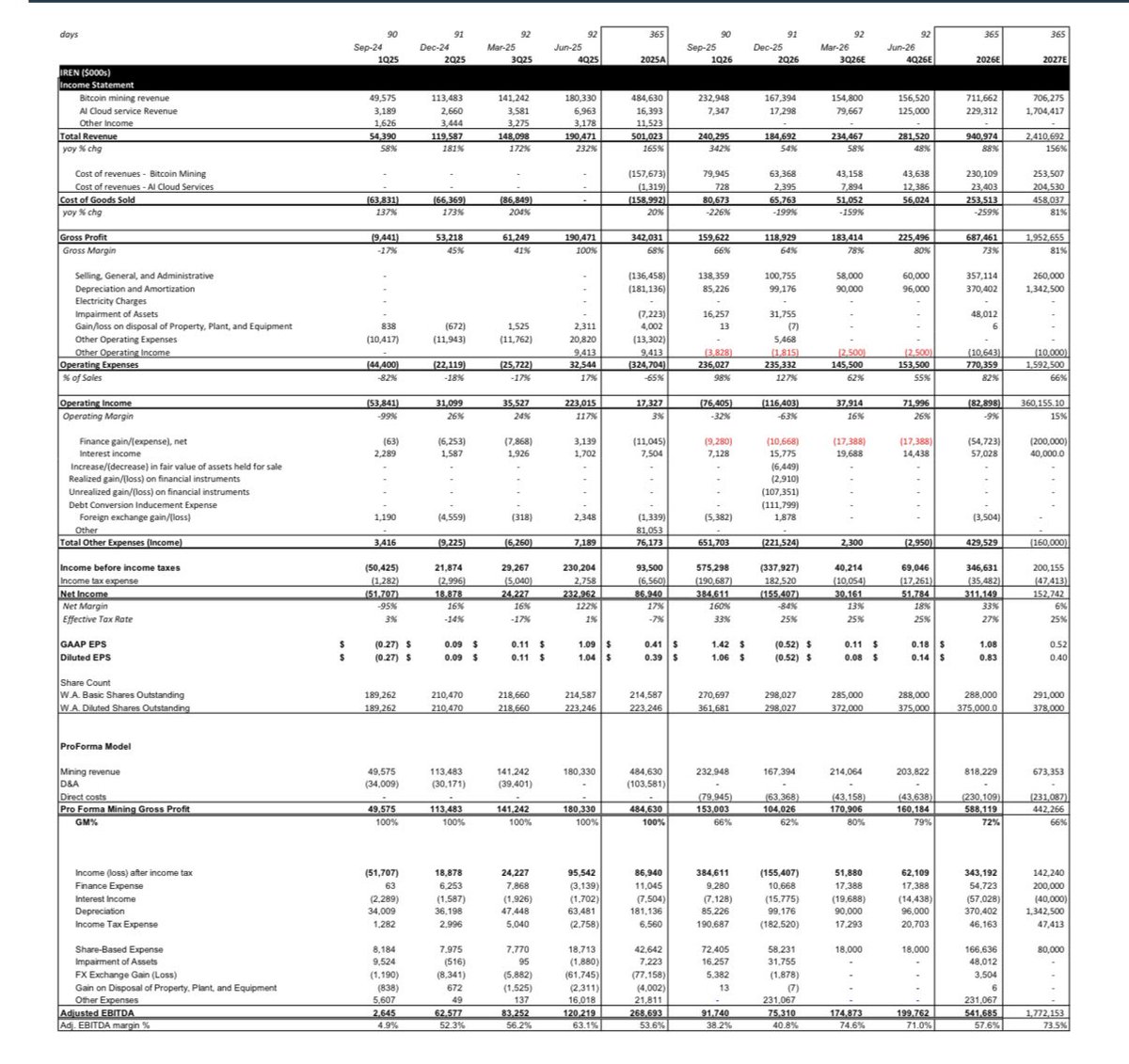

@Lazarus_Capital @bitcoinbutcher1 The top analysts and I all put out very good (and similar pro forma

IS) research. Thats ab as much detail and plenty legible, as I am able to share in the moment. Enjoy!

English

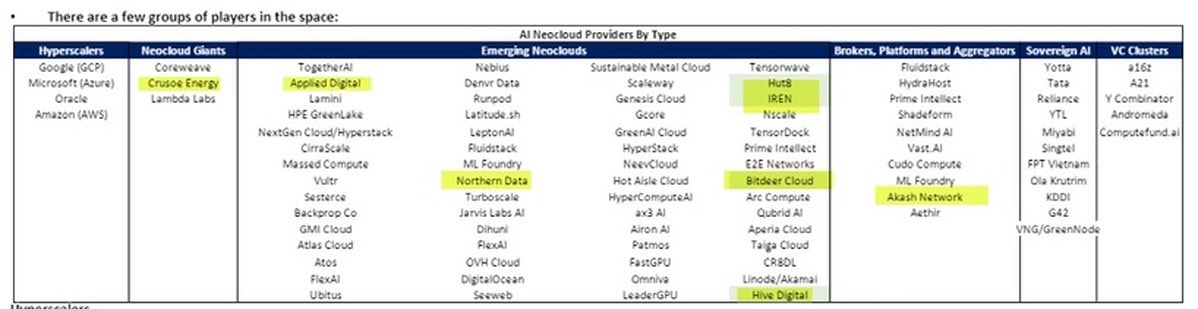

You keep sharing these two images, this one and another "neocloud players" or whatever.

Did you build it or do you just have access to compass research?

IF you did this yourself, can you send me a copy of your research? Would love to read it. If possible, in slightly better quality. This one gets pixedlated when looking at the numbers. Maybe a PDF?

English

I do. That’s who I remembered you to be an IREN (only?) specific only bear. Have you done the work on NBIS or CRWV or beyond? I have; Private and pubco’s. ~$1.77b EBITDA bottom right, plenty sustainable and growing. I am not only focused on IREN the whole sector is going to make it NBIS and CRWV. IREN happens to have the clearest growth runway (capability) at the moment. Good luck

English

@callah32 @bitcoinbutcher1 Maybe, but you can also just do the work on IREN instead of trying to argue that others are successful

English

@Lazarus_Capital @bitcoinbutcher1 Ah I see, fair. My generic reply statement can stand then.

English

@callah32 @bitcoinbutcher1 Not sure you’re understanding what I stated

English

@Lazarus_Capital @bitcoinbutcher1 Here’s a whole list (some of them my customers) that run sustainable businesses via the same economic model, DSCr 1.25x and beyond. Close your shorts

English

@bitcoinbutcher1 @callah32 50k b300 guide was in early March. Lets see by how much $IREN improves their year end guide on those b300s

English

@bitcoinbutcher1 No bubble, need more compute. Neo cloud is the neo-oil

< spike. Hot commodity supply < demand

English

@OpenAINewsroom Where did this silly CFO lady news come from without context/release of the rest of the financials. Terrible

English

We agree. The real leading indicators are clear: breakout Codex growth ✅, enterprise offerings on every cloud ✅, the only consumer app that matters ✅, a compute strategy built to accelerate ✅, and the best researchers in the world ✅.

Rittenhouse Research@RHouseResearch

The irony of the WSJ dropping a hit-piece referencing last year's numbers is that the real-time signal on OpenAI came from @SemiAnalysis_ just a few days ago.. With GPT 5.5's release and Anthropic's capacity constraints, OpenAI probably is accelerating as we speak while the WSJ is writing about 2025, lol.

English

@danroberts0101 dan this is the article you forgot to add

on LINKEDIN WE SAW THE MISTAKE, MAYBE X NEEDS MORE COMPUTE

tomshardware.com/tech-industry/…

English

Feels like we’re still early in the compute cycle.

Supply isn’t easy, real-world constraints are everywhere.

And every step forward in AI just seems to create more demand for compute.

English

@danroberts0101 Tbh it’s refreshing that you aren’t bottle-necking up your feelings

English

@danroberts0101 setting up a gamma squeeze to sell ATM into. CEO 410 Smrt

English

😆 well I love your EBITDA comps. what discount/debt rate do you want to assign $MSFT in this instance, sweet jezus (Lazarus) 😄? Your pretty close EBITDA number is down there bottom right. Also Who are you 😆 - and what are you favorite longs, Or are you and are just gonna (anon) resting on the energy infra to zero ~hill (or hate all neo’s and co-lo? none will make it?) I have other neo cloud customers on this list that have made it for years on this list, not just pubco’s. Debt lender by trade.

English

I am tragically dyslexic, and I work in finance. Seems weird, but hear me out. While I struggle with basic spelling often, and reading comprehension was insanely difficult as a child, I really couldn't read until 5th grade. It’s much better now, but it’s still something I deal with.

Even today, my amazing team @OGAdvisors has to put up with my chronic typos and often cryptic messages (sorry guys).

But here's the great part of my dyslexia: I tested in the savant category for pattern recognition and spatial awareness. I see the world in 4D*. I often struggle to understand why others don't. Just like they don't understand why I can't spell...

The dyslexia made it hard to fit into the normie's way of life. But it gave me a superpower, one that fits perfectly into finance and Bitcoin. And because I am one of the few who actually loves what they do for work, I wouldn't change a thing.

So if you see typos in my posts, I am not lazy, I am just retarded.

Thank you for your attention to this matter.

*4D (four-dimensional) thinking:

The ability to perceive and interpret patterns across multiple dimensions, typically including space and time, allowing for a dynamic understanding of how elements interact, evolve, and influence future outcomes. In practical terms, it refers to seeing beyond static snapshots and recognizing systems, relationships, and changes as they develop over time.

GIF

English

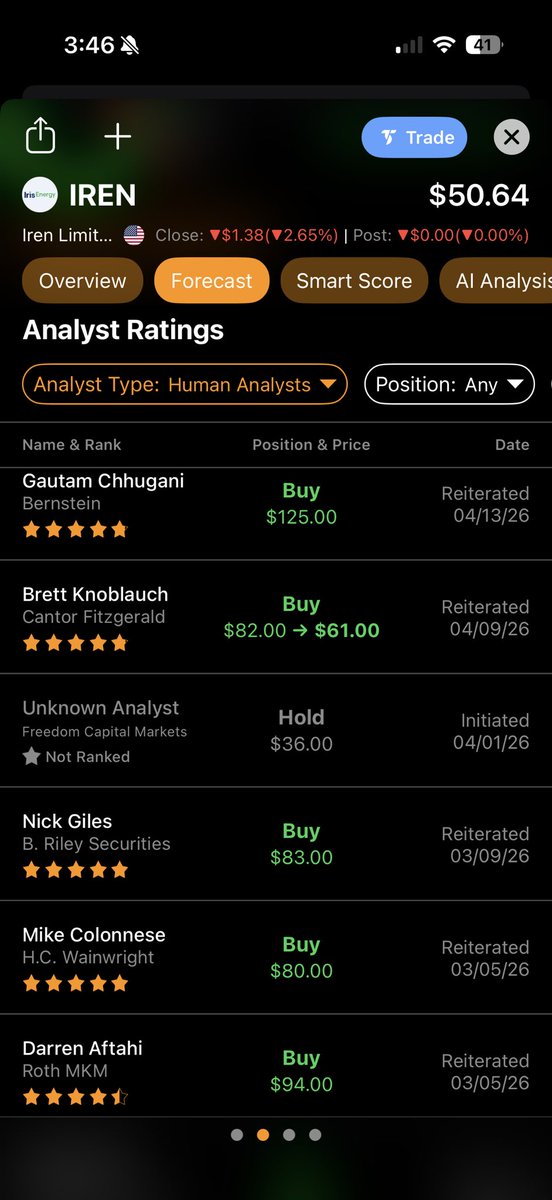

Not much to discount (% rate) w $MSFT as a Moodys aaa counter party (not gonna default over 5 years). So Just the face value (PV) of the of the contract $10b. You see it your way, personally I like the way the market is triangulating TEV at $3.7b x 5 ARR guidance or $50PT today; work in your EBITDA comps reconciles near TEV too. Market is pretty consistent across all 3 neo comps. IREN just happens to have the most room to add ARR rn. I’m w these guys below, their 12 mo PT prices in more ARR imo. Good luck!

English

@callah32 @JarronJackson4 if You’re doing PV you need to discount it. And I used unreasonable assumptions to show that it doesn’t even work under those.

Mind sharing your DCF math where you get $10B in NPV as a floor?

English

I don’t see how you’re bearish on $1.65b EBITDA x 10 or $16b TEV seems very reasonable to me. No doubt alot of ‘sunken cost’ (accumulated deficit) to build 30-40 year power shells (concrete, roof, steel walls, conduit), substations, and transformers. Should infact arguably Command an even more growing premium EV/EBITDA fwd value since the grid doesn’t have infinite Mw available. Talk w you during the week.

English

depends on what you mean by monetizing? profitably where it justifies the return? No.

So just using the MSFT contract as an example, lets round ARR to $2B annually, you're saying a $10B NPV. We know DC and GPU Capex are $8.8B, so the amount of positive cash inflows you need are a PV of $18.8B. First year revenue is $1.94B, ebitda of $1.65B. If we ASSUME some unrealistic assumptions such as the DC lasts forever, the GPUs last forever, no downtime, and that they earn $1.65B per year, every year, FOREVER, would require a discount rate of 8.8%... Check their WACC.

Honestly, would love to see your model where 5x ARR is the floor valuation. I don't see it. Not even close.

English