sinan

5 posts

English

Haven't mentioned Ryan Specialty $RYAN in a while because every time I write about it, only a couple people chime in with useful content. One of them is @griffonomics and he did an episode on it, which I recommend: youtu.be/iVcFllDHbNg

Prior to launching Ryan Specialty, Patrick Ryan founded $AON and served as its Chairman and CEO for 41 years.

Ryan is a leading wholesale brokerage and specialty lines insurer known for its substantial footprint in the E&S market. The fill the gap between retail insurance brokers and E&S carriers for complex or hard-to-place commercial risks. AI can't disrupt this if you understand it.

Most interesting tidbit? He is using his own personal $RYAN stock to incentivize talent. Not diluting more but offering up his own. That's a legit CEO right there.

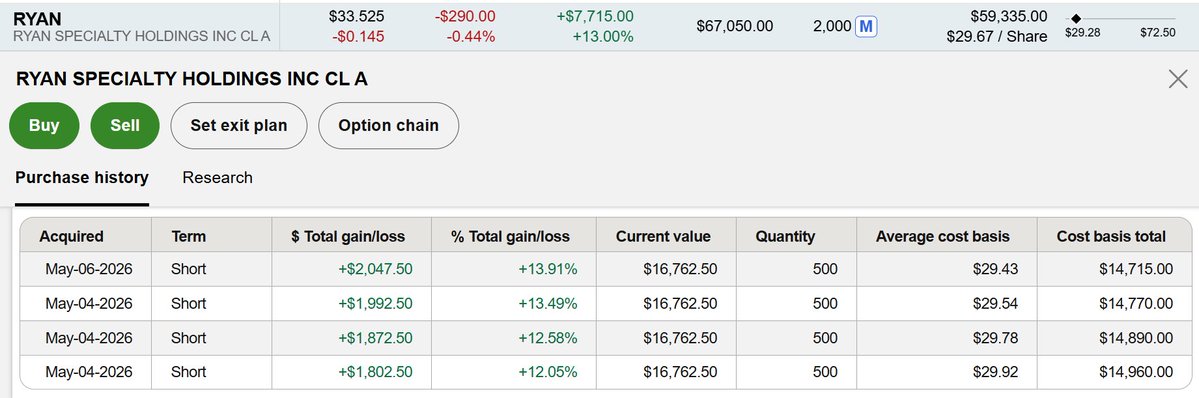

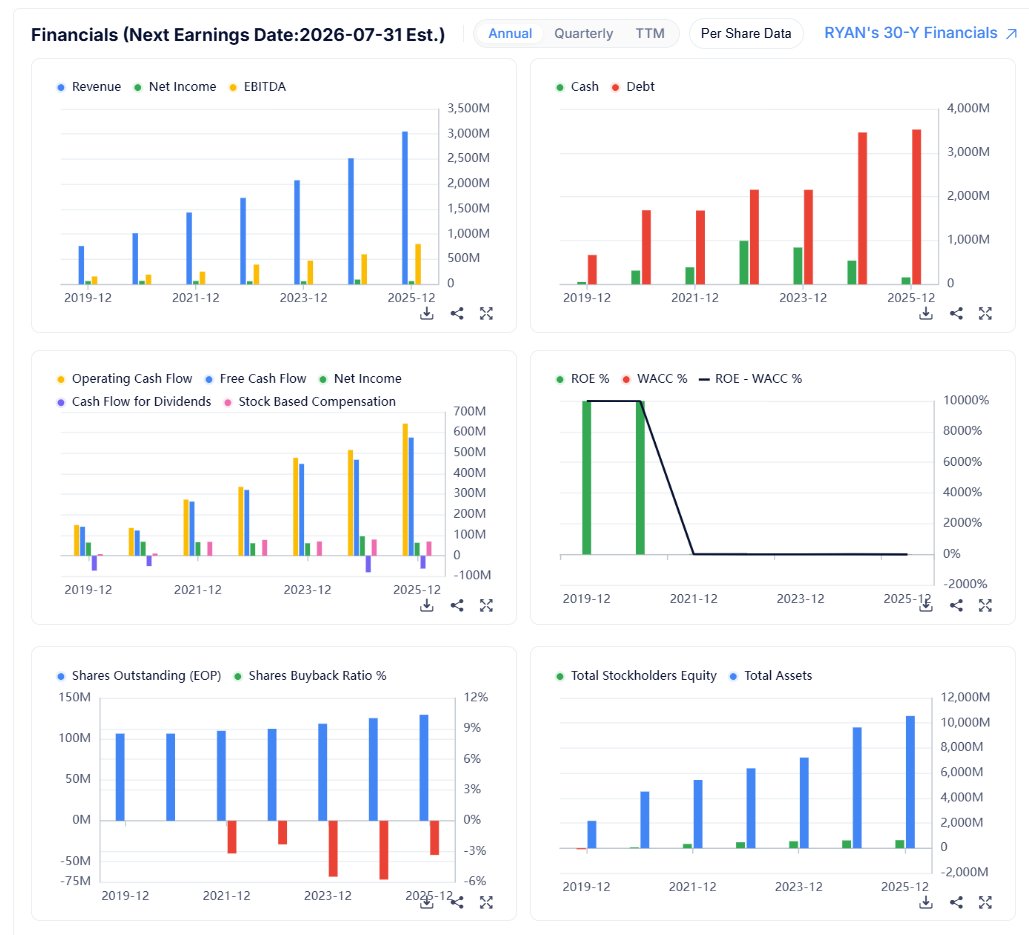

Price is still very low. Barely above the IPO from 5 years ago, despite the growth since. Financials from Gurufocus.

YouTube

English

@SayNoToTrading @InvestWithJorge @gyzo33 same here but for $CPRT. don't want to speak to soon but the price looks to have stabilized finally...

English

@InvestWithJorge @gyzo33 Nothing new to add to conversation.

English

Thanks to a callout by @gyzo33 on 50% off first $AMZN Subscribe and Save order of Spindrift, I was able to procure some within my budget.

However, if $NOW earnings don’t get us back to $112+ then no Spindrift for me.

By the way, flavored water + Lakanto liquid monk fruit = yum

English

@green_appl55431 but they don't disclose a revenue-per-vehicle metric, do they?

English

The most important number for $CPRT isn't revenue growth. It's service revenue per vehicle.

Copart makes money facilitating auctions AND providing physical services—towing, storage, title work. If insurers start demanding fee concessions, it shows up in per-unit economics first.

Watch for this metric in upcoming earnings. It's the canary in the coal mine for margin pressure.

English

@RyshabTalks recent follower. do you consider rotating a bit to safe havens? i know, they have already run up YTD but it seems that there are still a few that are not too expensive. or are you sticking with growth names, no matter what?

English

Portfolio Update as of Feb 27, 2026 ==================================

🔴 YTD Returns: -28%

🟢 $SPY +0% 🔴 $QQQ -2% 🟢 $IWM +8%

$CRDO 18%

$ALAB 18%

$RDDT 15%

$APP 14%

$DAVE 11%

$SNDK 7%

$MU 7%

$FBTC 6% (Bitcoin ETF)

$LMND 6%

Portfolio is 102% long and has 9 positions.

Changes this week: ==================================

Bought:

$FBTC (Never bought Bitcoin. But there always a first time. Given Bitcoin's history, this can go down another 50%, so this is a half position for now. I expect this to get back to all time highs, once risk on trade is underway. Fits well with my high beta growth portfolio strategy.

Sold:

$CRWV (Took a nose dive in FCF and management clearly told us, they would stay -100% FCF for the next 12 months. That's too much risk on execution, hence I am out)

Portfolio Summary: ==================================

Portfolio slid another 5%. There is no place to hide right now if you are in growth. Again, gotta play the hand you are dealt. Not happy with the performance, but I control how much leverage I have on the portfolio and I have pretty much taken out all risk as of today. I can just hold these stocks and let them recover. I expect each one of these stocks to get back to it's 52 week high over the near term.

I really want to increase my $MU and $SNDK positions but the stocks charts looks crazy. Don't have the balls right now. But ideally would have 10% in each. And the other one I am eyeing is $LITE. But again crazy looking chart. Hoping to get an entry before the next run.

This Week's Movers: ==================================

Top performers: $DAVE

And the worst ones: $CRDO $ALAB $LMND

Options Exposure: 2%

Sell Puts: $CRDO $ALAB $RDDT

Have a great weekend friends. Cheers!

English

Microsoft’un ($MSFT) günümüzde $475 civarında çok ucuz olduğunu ve dünyanın en iyi şirketlerinden biri için asimetrik bir risk/getiri profili sunduğunu düşünüyorum.

Hesabıma göre hisse şu anki seviyesinden oldukça cazip fiyatlanıyor ve %30’un üzerinde yükseliş potansiyeli taşıyor. 🎯Hedef Fiyatım $633

Piyasa şu an OpenAI kaynaklı belirsizlikleri ve artan harcamaları (Capex) risk olarak fiyatlıyor. Ancak yaptığım kapsamlı DCF Model çalışması, piyasanın bu riskleri olduğundan fazla büyüttüğünü ve bulut tarafındaki (Azure) gerçek büyümeyi hafife aldığını gösteriyor.

Gelin Microsoft’un alt şirketlerinden finansallarına kadar detaylara inip, neden piyasadaki en iyi fırsatlardan biri olduğunu inceleyelim

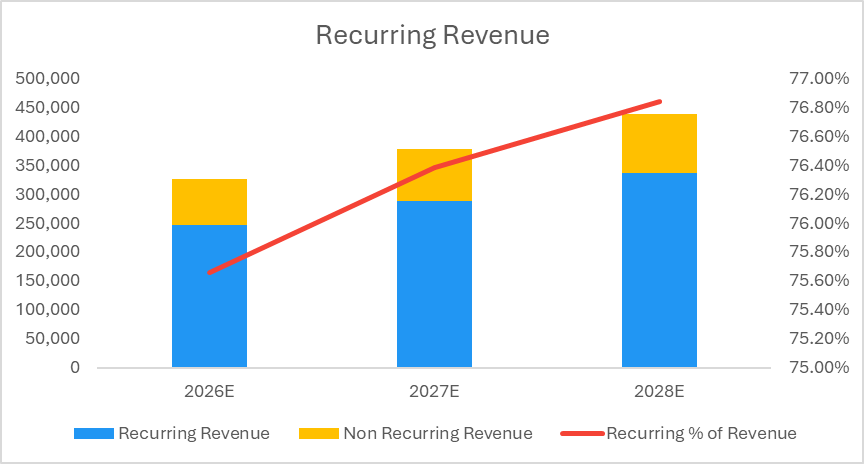

Analize başlamadan önce MSFT'ye bakış açımızı değiştirmemiz lazım. Microsoft klasik bir teknoloji şirketi değil. Finansal karakteristiği daha çok Visa, S&P Global veya FICO gibi çalışıyor.

Neden? Bloomberg Terminal beklenti verilerine (ve benim modelimdeki projeksiyonlara) göre gelirlerin %75’i Recurring (Tekrarlayan). Geçmişte %50-60 bandında olan bu oran, şirketi ekonomik döngülerden bağımsız bir kaleye dönüştürüyor.

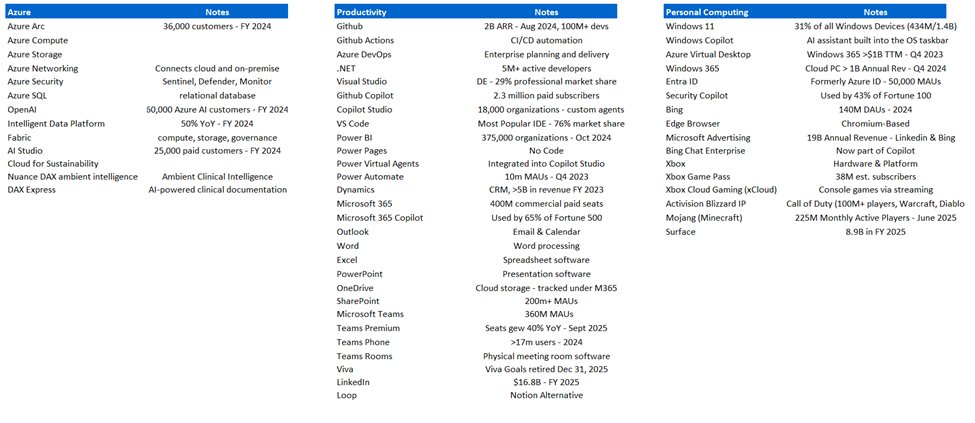

Bu kaleyi daha da sağlamlaştıran diğer unsur ise "Çeşitlilik". Amerika dışında hiçbir ülke ve portföydeki hiçbir tekil müşteri, toplam gelirin %10'unu geçmiyor. Yani şirket ne jeopolitik risklere ne de tek bir müşteriye bağımlı.

Yukarıdaki görselde, şirketin farklı kollarını nasıl bir araya getirdiğini ve gelir yapısının ne kadar çeşitli (diversified) olduğunu net bir şekilde görebilirsiniz.

Krizde Netflix aboneliğinizi iptal edebilirsiniz ama Office 365’i veya Azure altyapısını kapatamazsınız. Bu yapı, aşağı yönlü (downside) riskinizi inanılmaz limitliyor. Aynı şekilde müşteriler bir kez Microsoft ekosistemine girdiğinde kolay kolay çıkamadığı için şirkete inanılmaz bir fiyatlama gücü sunuyor.

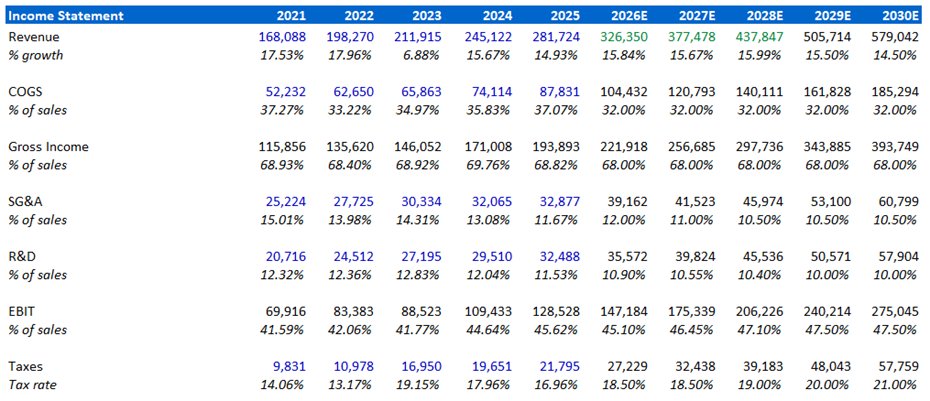

Bu fiyatlama gücünü ve "ekosistem hapsini" son 5 yıllık finansallara baktığımızda çok net bir şekilde görebiliyoruz.

Fotoğrafa dikkat edin. 2021-2025 arası Ciro (Revenue) devasa bir hızla artarken, giderlerin ciro içindeki payı (SG&A % of Sales) istikrarlı bir şekilde düşüyor.

1/3🧵

Türkçe