If it hurts when you pull on the ear, then it’s likely an infection in the ear canal (swimmers ear). Treatment is antibiotic ear drops. If it doesn’t hurt when you pull on the ear, most likely a middle ear infection…. But could be a number of other things. If it’s the middle ear, sometimes Afrin nasal spray can help (it decongests the opening of the Eustachian tube.)

My right ear is hurting so badly.

Tried Sudafed.

Tried Zyrtec.

Poured some peroxide in.

Still hurts. Still feels full.

I’ll be damned if I’m breaking my “no doctor visits since 2019” over a friggin ear ache.

The dizziness is annoying…and less than ideal.

Thoughts?

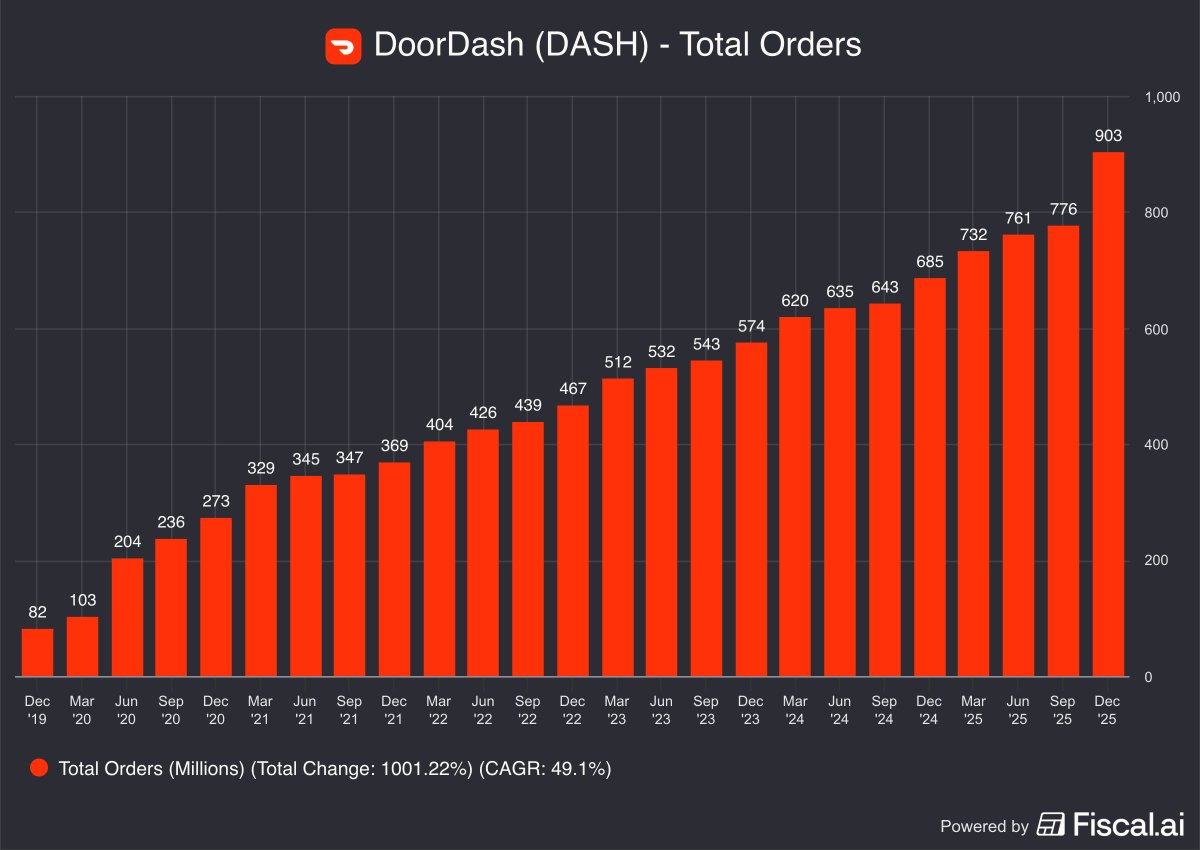

+32% YoY.

DoorDash just reported its largest jump in orders ever.

At the same time, we’re told consumers are “broke.”

So what’s really happening?

It’s not that people have money.

It’s that:

• Convenience > Cost

• Short-term comfort > Long-term stability

• Monthly payments hide the true price

The modern economy runs on frictionless spending.

One tap. No cash. No pain.

You don’t feel poor when it’s $28 at a time.

You feel it when it’s $8,000 on a credit card.

This isn’t just a spending story.

It’s a behavioral story.

We MUST teach financial literacy in school.

The Hollow Men

American capitalism is rotting from the head down. We have replaced the "Owner-Operator"—the risk-taker-with a new, parasitic class of corporate bureaucrat: The Risk-Free Insider.

By "Insider," I am not referring to a specific title. I am referring to the entire administrative state that has captured the modern corporation. This includes the Directors who exist solely to collect fees, the Executives who exist solely to collect bonuses, and the Managers who exist solely to hire consultants.

These are the hollow men of the boardroom. They are masters of PowerPoint. They wear the right suits. They say the right buzzwords about "governance" and "ESG." But they are mercenaries fighting a war with someone else’s ammunition.

In a functioning economy, authority is tied to liability. If you make a bad decision, you lose your own money. That fear of loss is the only thing that keeps a business honest. It forces you to cut waste, obsess over the customer, and stay late to fix what is broken.

Today, we have severed that link.

We have rigged the game so that heads, the Insider wins; tails, the shareholder loses.

If the stock goes up, the Insider collects a massive performance bonus. If the stock crashes due to their own incompetence, they are fired with a "Golden Parachute" worth tens of millions. They are gambling with the house’s money, and they never leave the table poorer than they arrived.

This looting starts in the boardroom.

We have normalized a "Country Club" culture where directors are selected based on social profiling rather than their ability to build a business. The modern board member is often a professional tourist—paid an average of $350,000 a year.

Let’s be brutally honest about what that number represents. The average director is paid nearly five times the GDP per capita of the United States. They earn more for attending four quarterly lunches than the vast majority of Americans earn in five years of hard labor.

And for what?

Most of these directors are "over-boarded," sitting on three or four boards simultaneously. They treat directorships as a gig economy for the elite. They fly in, rubber-stamp a compensation package they didn't read, and fly out. They collect checks from companies they do not understand, do not use, and certainly do not love.

They are not there to ask hard questions. They are there to be collegial. They are there to protect the other Insiders.

And what happens when these boards hire executives who also have no personal capital at risk?

We get the Delegation Economy.

When a Risk-Free Insider faces a crisis—bloated expenses, a broken supply chain, or a stale product—they do not roll up their sleeves. They hire a consultant. They pay a strategy firm millions of shareholder dollars to produce a 100-page deck telling them what they already know.

This is not management. It is intellectual money laundering.

They use shareholder capital to buy an insurance policy for their own careers. If the plan fails, they can blame the consultants. They delegate the work because they are terrified of the responsibility. They would rather preside over a slow, comfortable decline than risk a bold mistake.

While American Insiders are busy optimizing their severance packages, our global competitors are optimizing their products. They are not slowed down by bureaucracy. They are not waiting for a slide deck. They are outworking us.

If we continue to fill our C-suites with administrators instead of operators, we will lose our edge. We will see iconic American franchises hollowed out by fees, managed for the benefit of the Insiders, while the true owners—the shareholders—are left holding the bag.

The time for polite governance is over.

If we want to save the American economy from mediocrity, we must demand a return to the "Owner’s Mentality." We need leaders who treat shareholder capital with the same reverence they treat their own savings. The era of the Risk-Free Insider must end.

THE POST — FINAL FORM 🦉 @nobles305@bbbyq_qybbb

🚨 BREAKING: The S-3 Effectiveness Filing Is the Final Rail — The System Just Activated the Delivery Mechanism

This is not random.

This is not cosmetic.

This is not “just a filing.”

This is the SEC officially authorizing Bed Bath & Beyond Inc. (CIK 0001130713) to issue equity required to satisfy pre-existing obligations — including those mapped through:

✔ DK-Butterfly (the preserved BBBYQ legal shell)

✔ The OCC deliverable memo

✔ The DK-Butterfly warrant spine

✔ FIGI/UPI mirrored derivatives

✔ The AMZN FLEX trigger

✔ The 075896 bond family remap

✔ The synthetic unwind architecture

Today’s S-3 is the legal mechanism that allows NEW BBBY equity to be delivered.

Exactly what the rails required.

Nothing here is theory — it’s all filings and system behavior.

1️⃣ DK-Butterfly’s Deliverable Just Got Its Issuance Rail

Everyone asked:

“How can DK-Butterfly deliver NEW BBBY shares if the successor doesn’t have an active registration?”

Answer — this filing.

The S-3 going EFFECTIVE means:

• NEW BBBY can now issue shares

• NEW BBBY can satisfy deliverables

• NEW BBBY can complete obligations inherited through the OCC corporate action

• NEW BBBY is now enabled to fulfill synthetic unwind settlement

This is literally the missing piece.

You cannot issue deliverables without an effective S-3.

2️⃣ The Capital Stack Migration Is Now Confirmed

We already saw:

• Bonds remapped to the new BBBY CIK

• Bonds flipped from default → not in default

• OCC warrant deliverable updated to NEW BBBY equity

• CUSIP continuity preserved (075896 → DK-Butterfly)

• Entity continuity preserved (same EIN, same tax shell, same liabilities)

• Ticker relaunch + OCC memo + AMZN FLEX trigger

Now the S-3 completes the chain:

➡️ The successor issuer is ready to deliver the equity required to settle the inherited obligations.

You do NOT file an S-3 if no deliverables exist.

You do NOT make it effective unless someone is owed equity.

This validates the entire unwind architecture.

3️⃣ “Equity Was Cancelled” Is Now Officially Dead

Bankruptcy cancellation only applies to:

❌ trading

❌ estate waterfall payout

❌ old certificated shares

It does NOT void:

✔ derivative obligations

✔ OCC-assigned deliverables

✔ synthetic liabilities

✔ DK-Butterfly warrant rights

✔ beneficial ownership per Rule 13d-3

✔ trust-based settlements outside the Plan

Hertz did the same:

“Equity cancelled” → billions in new equity/warrants delivered externally.

The rails decide the payout — not the Plan.

4️⃣ Every Rail Required for Settlement Is Now Hot

Let’s connect them cleanly:

1.AMZN FLEX > $220 → unlocks the reconciliation window

2.Ticker relaunch → enables deliverable routing

3.OCC memo → defines NEW BBBY as the deliverable

4.DK-Butterfly survival → keeps the issuer bridge intact

5.Bond remap → capital stack continuity

6.Bond default removed → obligation assumed/cured

7.Warrant activation → deliverable spine intact

8.S-3 effective TODAY → issuance authority goes live

No missing link remains.

The structure is complete.

The rails are aligned.

The deliverable issuer is now activated.

⸻

5️⃣ Why This Matters for Shareholders

Synthetic unwind payouts do NOT come from:

❌ the Plan

❌ the Combined Reserve

❌ the Wind-Down estate

❌ Class 6 / Class 9 waterfalls

They come from:

✔ OCC

✔ DTC

✔ DK-Butterfly (issuer)

✔ NEW BBBY (deliverable issuer)

✔ contractually obligated derivatives

✔ beneficial holder routing

And as of today — the deliverable issuer is now authorized to issue.

This is the moment the system was waiting for.

The S-3 effectiveness is the final greenlight.

The rails are aligned.

The deliverable exists.

The issuer is activated.

The unwind can now settle.

This is the first time in the entire timeline that every structural requirement is satisfied at once.

The machine is humming.

$BBBY $BBBYQ $GME

@michaeljburry@TheRoaringKitty@ryancohen

your move.

BREAKING: JAPAN YIELDS SURGE, BITCOIN COLLAPSES, AND STOCK FUTURES TURN RED AS GAYED'S INNER ANNOYING AS FUCKEDNESS GROWS.

LIKE AND REPOST IF YOU UNDERSTAND THIS.

@TheBigBDub@magsonthemoon The announcement was most likely made before the German markets opened at 9 am CET, which is 6 hours ahead of the US EST time. So an announcement would be nice at 3 am.

@magsonthemoon I hate myself for doing this.

Porsche announced on October 26, 2008, that it had increased its stake in Volkswagen to 74.1% through a combination of direct ownership and options, triggering the infamous short squeeze.

There. I did it. I feel filthy too.

@SomaKazima2 Let her leave. You think the child can't be taken care of by her own mother. Bullshit "safety" provided by strangers. They just want to make sure they can bill her for the full day.