CharanInvests

69 posts

CharanInvests

@charaninvests

Trader & Investor || 200k+ IG/TikTok ||

New Jersey, USA Katılım Şubat 2024

417 Takip Edilen1.2K Takipçiler

@charaninvests @retail_mourinho He’s a clown, I already addressed him in the DM’s. I’m gonna let him have his little moment this 1x

I actually added in the 70’s on Friday

Here’s my update on POWI

bryan@BryzonX

Today I added to my $POWI (Power Integrations) position, planting my flag in what I believe will be a massive Capex wave transforming the entire power semi space Currently, $NVTS is getting all the love which is fair, however... With the release of the specs for the upcoming architecture of the 800V Data center for VR200 it is quite clear that there will be a huge demand for high voltage GaN rather than high speed integration GaN in which NVTS provides The server rack will be scaling from 120 kW to 600 kW (!) The core issue isn't going to be how fast a chip can switch, it will be about how much raw voltage can actually survive Navitas flagship GaN tech (GaNFast and GaNSafe) maxes out at 650V It was originally designed for high speed switching in consumer electronics and lower volt apps not not megawatt scale AI infrastructure A 800V data center will instantly destroy a lone 650v chip. To participate, NVTS has to combine lower voltage components in a highly complex stacked build which creates clunky workarounds, wastes physical space, and introduces severe points of failure POWI's chips doesn't require these unnecessary workarounds Their InnoMux-2 is the ONLY chip on earth that features a 1700v switch on a single piece of silicon When NVDA starts to roll out these high power racks, a single PowiGaN chip will be able to handle it natively with an integrated safety buffer to spare Which is IMPORTANT because in the case of power spikes, POWI's voltage leaves a 900v buffer that is built to handle the power spikes without creating a power failure Let me put this into context for you guys If NVDA said F it let's skip 800v and go straight to 1200v DC POWI's 1700v chips are still able to handle the power consumption TODAY still with a SAFETY BUFFER Here is why $POWI is still undervalued: They didn't build the 1700v chip for AI They originally built it to handle unstable power grids in developing markets and heavy electric vehicle architectures When $NVDA shifted the Vera Rubin architecture to an 800V DC baseline, their engineers realized they needed a battle tested SINGLE chip solution to safely drive the background cooling infrastructure (fans, liquid pumps, and logic controllers) POWI was the only company in the world that had spent decades perfecting single chip high volt integration. That deep reliability is why they are co-designing power blueprints alongside NVIDIA TODAY If you track the projected power infrastructure spend per AI rack, the metrics are going vertical: Current (GB200): $36,000 per rack 2026 (Vera Rubin): $76,000 per rack 2027 (Vera Rubin Ultra / Kyber): >10x increase (Over $360,000 to $398,000+ per rack) POWI's TAM is literally multiplying right before our eyes Currently, their entire business is still being dragged down by legacy When you look at $POWI at surface level, you see flat YoY revenue, lower GAAP margins, and a high P/E ratio but don't be fooled, their PowiGaN product division is growing at over 40% annually and will continue to accelerate as the VR is deployed In February 2026, POWI even did a 7% workforce reduction to reallocate that money toward scaling DC revenue You are essentially paying a cyclical multiple for a boring legacy appliance business, and getting a structurally protected, high voltage AI pure play for free even after the initial move From a TA perspective, just look how coiled it is. Currently trading under it's HTF downtrend line while simultaneously allowing moving averages to play catch up It's only a matter of when not if imo this breaks out NFA. Research purposes only.

English

New Long Idea: $POWI

While everyone is talking about the new $NVDA Rubin and $AMD Mi-455x chips that are just entering volume ramp, the real winners are the companies whose revenue is about to explode in 2H 2026.

$POWI is exactly that play.

The new-generation GPUs are so power-hungry that hyperscalers are forced to move to 800V rack architectures. That creates a massive, power-intensive buildout.

$POWI is currently the only company in the world shipping 1700V GaN chips. That gives them a brutal moat. Their chips make the new super-racks 50% smaller, more reliable, and cheaper to run, less copper, higher revenue per square foot for $META, $GOOGL and $AMZN.

Their GaN technology has already been battle-tested for years in the automotive industry (the harshest environment on earth). Hyperscalers can drop it in immediately with almost zero qualification time.

Competition $NVTS has to stack multiple lower-voltage 650V chips → more failure points, bigger, more complex. POWI does it with a single chip. The market isn’t pricing this in yet because they’re still shifting from their old appliance business into AI infrastructure (they just did a 7% headcount reduction to reallocate capital).

But their industrial business is already growing 40% YoY, margins are expanding, and the Rubin cycle is set to kick off hard in 2H 2026.

>Market cap: only ~$2.6B

>Zero debt

>$250M cash

>313 days of strategic chip inventory held back for the data-center boom

>1.81% dividend (already cash-flow positive)

The new chip cycle is creating an entirely new set of winners. $POWI could be one of them.

-RM

English

@BryzonX @retail_mourinho You were early lmao - what do you think about going long in the 70s i didn’t see your original tweet back then lol

English

@retail_mourinho lol it’s a copy of @BryzonX old tweet that’s why mc is wrong😂

English

@retail_mourinho It’s closer to 4 billion mc? Also where do you get that 40% yoy growth number for industrial i couldn’t find it

English

Just posted my high conviction LT pick to SS subscribers.

It’s a company that has pivoted its product portfolio to target data center optics and a 10x increase in SAM.

Link below.

English

English

$AAOI is setting up what I would consider a textbook “slingshot setup.”

Large expansion move higher → healthy pullback into the 9/21EMAs → weak hands shaken out → now starting to curl back up on the right side of the base.

This is exactly the type of setup I obsess over in leadership names because the goal is NOT to chase emotional extension… it’s to position during controlled weakness while risk remains definable.

And volume is showing very little real selling pressure here. This looks much more like digestion/resetting than actual distribution to me.

I’m long again.

Let’s see what this next leg can do from here!

Chart: $AAOI.

iain@ohiain

4 names I’m watching closely tomorrow: > $INTC (slingshot setup) > $AAOI (slingshot setup) > $INOD (HVE + PEG setup) > $QCOM (PB focus + HL setup) All 4 made strong range moves higher and are now pulling back into the 9/21EMAs, which is exactly where I start paying very close attention for potential "slingshot" setups. The first pullback after expansion is usually where institutions step in again if the trend is truly healthy. Strong stocks rarely go straight up forever… they move, digest, shake weak hands out, let the moving averages catch up underneath price, then attempt the next leg. That’s why I love these “right side of the V” setups so much. I’m not trying to buy dead stocks making new lows. I’m looking for strong names in strong groups that already proved they can move, then waiting for controlled weakness into support where risk becomes definable again. The pullback into the 9/21EMA is often where: - weak hands panic sell - momentum cools off - patient buyers reload Compression → Expansion. Same process over and over again on leadership names. Names: $INTC, $AAOI, $INOD + $QCOM.

English

You know what’s crazy?

This dude

Kevin Xu

Has 3x more followers than me.

I have 4 mill more than him and a CAGR way above his.

He charges 200 per month for his “ideas”

I charge nothing.

Yet I’m way below his follower count.

Bro, why are you charging that much if you have that much?

What am I missing?

English

A important part of my framework for trading the mkt is that there are a lot of excellent setups (both long and short) that make perfect sense but simply won't work because the mkt simply isn't ready for it yet.

The sweet spot is being able to catch these ideas right before you can see a wave of inflection coming to the idea.

an example:

The memory trade has been strong for a while already but only recently did the 2nd (and 3rd --mram) layers derivative benfeciaries from it start to a very strong bid.

Not many (one) completely legit ones (one) left out there and you can feel the tide coming.

English

@joedab12 Can you also explain the Anthropic and $AAOI connection (from a numbers standpoint) haven’t seen anyone else talk about this?

English

@charaninvests They may but with much more downside risk. Vicor is derisked with fab1 alone putting them at 400+ next year being conservative.

English

I was literally the only person on X telling people to play Anthropic upside via $AAOI 300% ago even after it had just run up from $20 last November to $50s in february. Now I may be the only person telling you to play $CBRS upside via $VICR even after it has just run from 50 to 250 in 9 months.

I'm still buying more $VICR every week. Here's why:

-$CBRS wafer scale engines require massive power density and Vicors vertical power delivery is the solution they picked.

-Very recently a "major hyperscaler" and AI chip "OEM" tested Vicors 2nd gen VPD and that is the reason for the additional capacity expansion at their first fab in Andover, MA.

-Founder/CEO with largest stake of any profitable/public semiconductor company on US market. If you dont know how successful founder lead companies are, you should do a little research. This one is not only founder lead, but at 79 years old he retains a MASSIVE equity stake of over 20% of his company.

-$1.5b fab at max capacity by year end-for comparison $MPWR will do roughly 3.5b next year but has 13x the market cap of $VICR - there is a huge re-rate due here once the market begins to price in this first fab running at/near full capacity as it gets closer to reality in Q4.

-$90m annual royalty revenue after defending IP succesfuly last year and on path to $180m+ royalty ARR next year or two as they have a 2nd ITC case pending against some giant companies such as Delta MPWR and others.

-EXCESS demand to the point where their 2nd fab planned to be operational in 2028 is not enough-they are actively looking to license their IP to someone with extra capacity and scale to serve other customers they do not have the ability to supply. Why not just wait till 2028 when the 2nd fab is operational? Maybe that customer is $NVDA and they dont want to miss being designed into Feynman(read my many other posts as to why that is likely going to end up the case)

-

Joe@joedab12

Not if your top holding is $NVDA $AAOI $VICR Plenty of companies benefit from anthropics success, Ive posted many times why AAOI is the purest anthropic proxy and now the market is agreeing with me. Vicor is still dirt cheap trading at 25x 2027 earnings BEFORE they inevitably land nvda/amd/google/amzn for their vpd gen 2 chip. Nvidia is nvidia.

English

On January 17, 2026, @Han_Akamatsu told his 61,000 followers that buying $ONDS at $12+ would help them become a millionaire.

He still hasn’t bought himself.

His history with the stock is damning:

On November 12, 2025 at $5.80, Han called for a downtrend on $ONDS with targets of $4.20 and then $2.

“Every time this played perfectly,” he said.

The stock continued higher.

On December 4 at $8.92, he posted the monthly RSI overbought thesis and called $4.50 as the next entry point.

The stock exploded to $15+ in a month.

Then on January 17 at $12+ — after both calls were proven wrong — he told his 61,000 followers to buy $ONDS as part of his public “millionaire” stock list.

But he still did not buy it himself.

Today at $9.06, he is back with a bearish pennant thesis hoping for $4.50.

He followed it up with this: “All I can do is pray for that move to the downside so I can have a better average than most people.”

He is not analyzing. He is praying.

His technical analysis on $ONDS is not special insight either.

The entire drone and defense sector has pulled back.

Every chart is under the same pressure right now.

Three bearish calls over three months.

Every single one wrong.

His 61,000 followers deserve to know that before they act on the next one.

I am beginning to seriously question why this account is treated as a credible source on anything.

For context:

At $4.50, the market cap is $2.27B against $1.4B in cash.

Enterprise value drops to $777M.

The contracted backlog of $457M alone covers nearly 60% of that.

Forward revenue guidance is $375 million.

EV/Sales on 2026 guidance is 2.07x.

I shouldn’t need to explain how absurd of a valuation that is for this company.

At some point, the cheaper entry stops being a strategy and starts being the reason you missed it.

Please, be careful who you take advice from on here.

Han Akamatsu 赤松@Han_Akamatsu

$ONDS Still on the verge of a collapse if it losses this 1W Pennant with good volume. Sitting on the sidelines until a move is made from the stock. Hopefully to the downside. In case stock reaches $5/4.5 I’m prepared to go full LEAPS.

English

$CBRS IPO this week and I think it goes nuclear

Cerebras built what nobody thought was possible. One chip. An entire silicon wafer. No stitching together hundreds of GPUs, no bottlenecks, no bs. Up to 15x faster inference than Nvidia’s best.

Groq has been getting all the hype for fast inference. Cerebras makes Groq look slow.

OpenAI just signed a $20B deal with them -> $510M in revenue last year -> every major tech company on the planet is trying to find an alternative to Nvidia and this is the only thing that actually delivers.

“Cerebras is the first architecture in decades that actually challenges the GPU at its own game” -> Dylan Patel, SemiAnalysis

They are IPOing at the perfect time. Just look at $SMH. AI infra spend is going vertical. The window is open right now.

IPO range $115-125. I expect it opens above $170. Already trading above $250 on Hyperliquid.

Fills will probably be shit given how oversubscribed (~20x) the IPO is - I am watching $WYFI and $VICR as sympathy plays

English

@labubu_trader What do you think about $VICR as a proxy play?

English

I will play this IPO for sure.

And already bought $WYFI as the proxy play.

3X Long Labubu@labubu_trader

Fuck there was an opportunity to buy secondaries at $1.8B back in 2024, and I skipped it as everyone around me(including me) thought it was a fucking scam

English

@HunterAllen4 What is this ai generated bs

The market cap is over 1 billion not 200 million?

You are very late

English

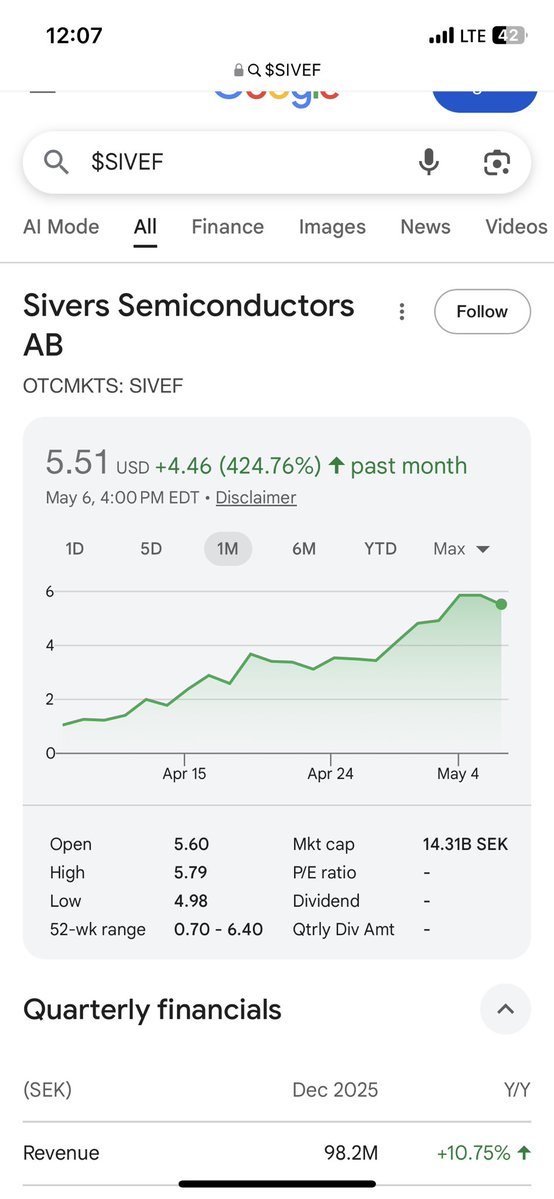

Don’t miss the next $LITE

$SIVE $SIVEF

A 100x play of this generation.

A CPO cycle bottom ticker still unknown to many.

This is the bottom.

Like buying $LITE at $20 in 2015.

Up 424% in 1 month as Nasdaq listing looms.

All at ~1B SEK valuation / roughly ~$200M USD market cap.

We are EARLY.

This is THE photonics play if Nasdaq approval is granted.

500$ stock chilling at 5$.

AI infrastructure supercycle is accelerating.

Power + compute + optical bandwidth = the bottleneck of the AI era.

THIS IS A POTENTIAL 100x AI PHOTONICS RE-RATING IN EARLY STAGE FORM

~$200M market cap vs multi-billion dollar optics peers

Record FY2025 revenue: SEK 304.1M (+25% YoY, +33% constant FX)

Q1 revenue: SEK 78.5M (+40% YoY)

Q4 revenue: SEK 80.7M

~87% gross margin profile

Product revenue growth +13%

Wireless growth +35%

Product pipeline growth +90%

Total opportunity pipeline: $453M (+64% YoY)

Q4 adjusted EBITDA turned positive at +10.8M

FY adjusted EBITDA improved 31% YoY

Cash flow breakeven targeted at only ~$50–55M revenue run-rate

~SEK 1.07B equity base

Strengthened balance sheet via refinancing + raises

Cash position improved entering 2026

Heavy R&D investment phase ahead of hyperscale ramps

2026 analyst revenue estimates:

SEK 360–415M

2027 analyst revenue estimates:

SEK 487–536M

2028 bullish scenarios:

SEK 650M–1.3B+

Long-term targets:

25–30% CAGR

Gross margins >50%

EBITDA margins >30%

Major ramps begin:

• AI photonics / CPO

• 1.6T optical interconnects

• LiDAR

• SATCOM

• Defense

• FWA

This is the upstream laser supplier for:

$AMZN

$MSFT

$META

$GOOGL

$POET

$JBL

O-Net

Enablence

Same exact category rotation path as:

$LITE $COHR $AAOI $POET $MRVL

This is the upstream light source layer most people still don’t understand.

$NVDA $AMD $AVGO $ANET $MRVL $LITE $COHR $POET $AAOI $GFS $TSM $NBIS $IREN $DRAM

DON’T MISS THIS GIANT🚀

English

@Han_Akamatsu Many accounts blown lol…

Why short these momentum names?

English

@enrichtrades It’s already overcrowded lol you know it’s late when every single post is about photonics

English

Photonics 101 - why this sector is the next leg of AI:

Every data center being built right now has a bottleneck. It's not compute. It's the cables & connections moving data BETWEEN the chips.

Copper can't keep up. Light can.

That's photonics. Moving data through fiber & optical components instead of copper wire.

The ecosystem:

→ Lasers & light generation: $LITE $COHR $LASR

→ Optical transceivers: $AAOI $POET

→ Connectivity & DSPs: $CRDO $MRVL $AVGO

→ Networking: $ANET $CIEN

→ Glass & fiber: $GLW

→ Manufacturing: $FN

AI demand isn't slowing. The infrastructure to support it is just getting started.

Learn the sector before it gets crowded!!!

English