compound2035

3.7K posts

compound2035

@compound2035

Investor in AI, space, drones, energy, precious metals, and IPOs.

San Diego, CA Katılım Şubat 2009

1.2K Takip Edilen489 Takipçiler

$BB $NOK

Blast from the past. Two names coming back to life.

Cray cray.

English

@RealSimpleAriel @ryancohen He’ll find it under the mattress, just needs like $16b

English

@compound2035 @ryancohen He is missing a good chunk of cash, and i think that comes in the form of dilution

English

@haciendo_verdes @RealSimpleAriel @ryancohen Lmao. 😂 which part isn’t clear, hunny? Half cash, half stock.

English

@compound2035 @RealSimpleAriel @ryancohen any time my wife asks me how we're going to afford something, this is gonna be my go-to line now

English

Rare earth names look ready to explode.

All these names have reclaimed and backtested ATH VWAP, which I consider a major level.

We should see stronger price action in this theme in the coming weeks.

$MP $UAMY $USAR $REMX

Venu@Venu_7_

Rare Earth names are giving the comeback as well $MP - MP materials breaking out of downtrend and held through $50 support level and VWAP from August 2025 lows! $UAMY - super coiled setup trading well above key moving average's $UUUU - it has theme of rare earth and uranium

English

@KawzInvests @KawzInvests I almost bought this one at $28. $lite had been running and I thought this one is next. I hesitated. Then it jumped 50% and I thought “Damn I missed it.” I had conviction and a good feeling. Now it’s up 4x. How do you learn to trust yourself? $aaoi

English

$AAOI is my biggest position. Let me show you exactly why using their own words.

On the Q4 earnings call, CEO Thompson Lin was asked about the $1B+ revenue guide for 2026.

His response:

"The demand is much, much bigger than $1 billion. That's the number we feel minimum 99% confident we can deliver."

Then the CFO said this about the $378M monthly run rate target for mid-2027:

"This revenue level is limited by our production capacity and supply chain — not market demand, which we believe is much larger."

Read that again.

The ceiling on this company is not customers. Not competition. Not pricing.

Purely how fast they can build fabs.

Now here's what nobody is modeling correctly.

That $378M monthly number — $4.5B annualized — is not the ceiling. Management explicitly said customer demand exceeds even that figure.

On capacity, here's the number that floored me:

End of 2025: 90,000 units/month of 800G capacity. End of 2026 target: 500,000 units/month.

5.5x capacity increase in 12 months.

Here's how that ramp actually plays out:

- 800G firmware completes: mid-March

- 800G volume ramp begins: Q2 2026

- 500,000 units/month online: end of 2026

- $378M monthly run rate: mid-2027

And here's the part the market is completely missing on capex efficiency:

800G and 1.6T are manufactured on the exact same production line. Every dollar $AAOI spends building 800G capacity is automatically 1.6T capacity.

Competitors building separate lines are burning capital twice. $AAOI is not.

Then on hard orders:

"Within less than three months — $100M+ in 800G orders. $200M+ in 1.6T orders."

From a company doing $134M in total quarterly revenue today.

"It's not a demand issue" — said three separate times on the call.

The question for $AAOI is not whether demand exists. That's been answered.

The question is purely execution. And they just committed $300M to triple their laser manufacturing capacity in Texas to answer it.

Full breakdown + DCF on my Substack(Link in Bio + Below)

KawzInvests 🦑@KawzInvests

$AAOI up 50% today. Management guided $378M per month in transceiver revenue by Q2 2027. That is $4.5B annualized. A $50B market cap does not sound crazy when you run those numbers. We are early. $LITE $COHR $AAOI

English

English

@KobeKapital @DividendRoots @Investmentkage nah. FLEX at $60 was the buy. my new ticker is absolute fire....and extremely low risk.

English

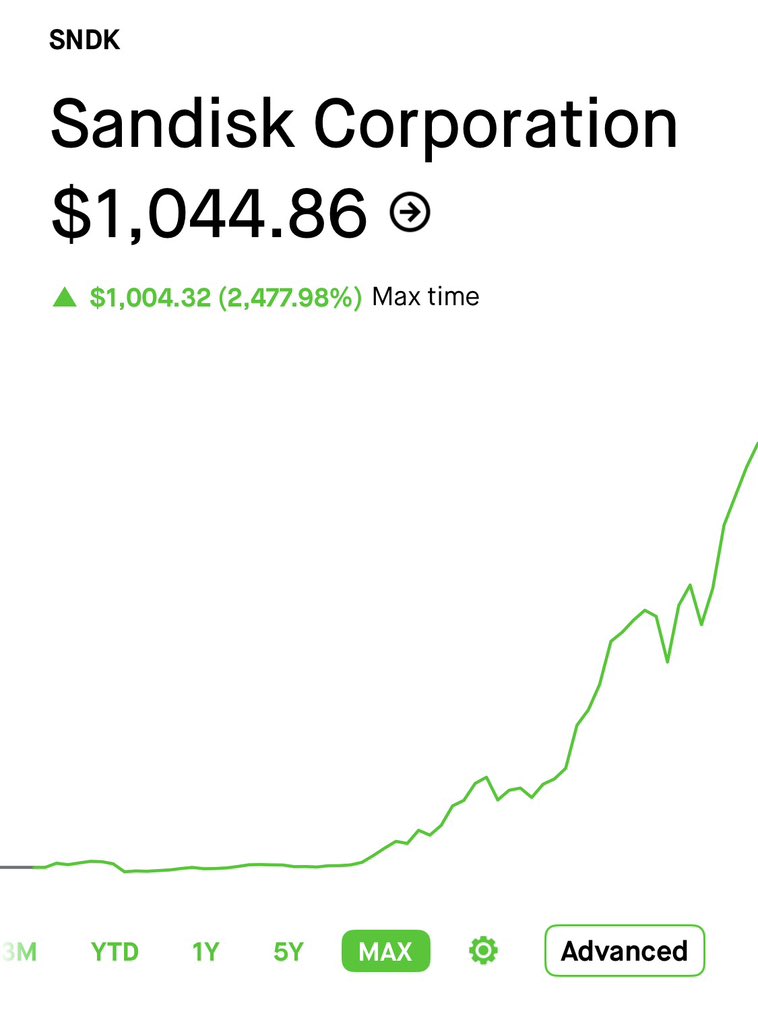

I just saw a post from @Investmentkage about $SNDK .. which made me remember about a year ago when @DGretta_Author was telling me about this ..sigh.. should have listened..

Oh well lol time to pay attention to his next mention

English

Massive moves in both $BE $STX. But not all is perfect $TER down roughly 8%

English

English

@BurnsAndGambo @Gambo987 Losing to Portland and THAT made all the difference.

English

What will you remember most about this Phoenix Suns season?

English

@BurnsAndGambo @Gambo987 How unwatchable the NBA is becoming thanks to all their replay reviews

English

@yezdi88 @johhnyWalkerAZ You’re right. Never getting back to $10.

English

@johhnyWalkerAZ Im completely baffled, maybe we will never see a <$10 again

English

@RealSimpleAriel Yikes. 😳 suddenly my fomo is gone on this one. Wild how quickly things can turn

English

$POET loses orders from from Celestial AI. down -48%.

Do we think that maybe these semis ran a little too hot?

English

@SFarringtonBKC I like gold and silver miners as a rotation out of tech leadership

English

My entire feed is data center bottleneck ideas. Feels kinda crowded. What's hated right now? Gold miners, consumer discretionary, healthcare, insurance?

(Not you software)

English

@StonkChris As Nokia goes, so goes the market? $nok $spy $qqq

English

Something for the doomer bears…

The last time $NOK monthly RSI got this overheated was back in 2000 and 2008.

Price still looks like it has a bit more room to run into that major HTF downtrend resistance line, but we’re clearly getting into stretched territory here.

So the real question, does that level line up as the broader market sell signal as well?

English

@YoYInvestor Great work ngl. No position in $AVEX but always on the look for cool small-cap defense plays.

English

$AVEX - This $3.6B Anduril competitor could be the next 5x drone stock.

Calling it at $34/share as the most asymmetrical defense stock since $KRKNF.

AEVEX went public on the NYSE last Thursday but FinX totally missed it.

This 650 employee baby Anduril has shipped 10K drones to Ukraine, is guiding for $800M 2026 revenue, and has 100K sq. ft of manufacturing space that can push out 1000/units a month.

Did I mention it beat out Anduril on an Army program?

At $32/share it’s MC is over $1B less than $ONDS despite doing 5x the forward revenue, having a suite of highly integrated, battle tested products/software, a deep history as a government contractor, and winning two sole source Pentagon contracts worth $1.2B combined.

It also trades at half of $KTOS on forward revenue, despite growing way faster (85% guide) and being a pure play drone stock. Has a $500M+ backlog and an $8B identified backlog amplified by $50B in proposed UAS spending by the DoD this year.

What differentiates AEVEX from other wannabe drone stocks is they’ve been doing ISR missions since 2008 (founded by OG UAV Air Force guys) and have been pumping out thousands of attritable mass units for Ukraine for years.

In 2022 the Pentagon needed thousands of cheap drones in Ukrainian hands in weeks, and $AVEX was the only one who could turn on the line. They delivered 4,400 units across 7 platforms for roughly $554M in contract value, with the fastest runs moving from order to warfighter in 9 days. The follow on was EUCOM AOR Deep Strike which awarded another $645.7M for 4,800 aircraft across 7 platforms, sole sourced again.

What’s crazy is the diversity of $AEVX’s platforms. Their website feels like Anduril in that they have so many exciting products/designs from loitering munitions (Dagger) to long range drones (Raker) to even unmanned surface vessels (Mako).

They also have a software platform called CompassX they expect every product to run on by year end (and be compatible with other manufacturers) AND a crazy moonshot product called ForgeX which is a mobile manufacturing facility for drones. ForgeX is literally a container placed near the battlefield and can pump out attritable weapons.

I think there’s a strong margin of safety on the valuation side but the risks are worth mentioning. Basically all their revenue is coming from programs for Ukraine which could flip on a dime if the war ends or if the U.S. pulls support. AEVEX is spending way less on R&D than Anduril and Shield, which is not encouraging in a fast-evolving landscape. IPO proceeds are mostly being used to retire debt than fund growth and re-investment into the business. Lock up expires in 6 months in mid-October and MDP (a PE firm) holds 79% of the float.

My rebuttal is that even without Ukraine the DoD is spending $50B of UAS with the new $1.5T budget and new theaters are emerging in Iran and the Pacific. R&D as a percentage of revenue is actually higher than public peers AVAV and KTOS. On the liquidity side, $375M of new credit facilities will help bolster things. I can’t find any reason to believe MDP is a bad actor or “worse” than other PE firms, but governance is always going to be a risk in this kind of set up.

Overall, I don't think a drone prime as high quality and proven as $AVEX should be trading anywhere near the MC of a diluting, pump holdco like $ONDS, especially with the new defense budget and Iran War tailwind. Retail deserves a higher quality drone prime with credible contracts, manufacturing, and capacity. I think $AVEX is that stock and presents a phenomenal long for anyone trying to play the future of defense.

$AVEX is at 4.5x forward sales at $32/share.

$AVAV at 4.5x.

$KTOS is 7.8x

Anduril at 14x.

$ONDS at 23x.

Shield AI at 24x.

Bear case: $31 ($AVAV floor)

Base case: $56 ($KTOS, +74%)

Bull case: $170+ (Shield AI / ONDS multiple, +430%)

To read my free deep dive report on AEVEX I’ve linked it below.

English