Conana.eth 🔻🔻🔻

7.1K posts

Conana.eth 🔻🔻🔻

@conanahere

#Web3 | Business in Hardware Distribution. #Mecha

Singapore Katılım Aralık 2020

5.1K Takip Edilen4.4K Takipçiler

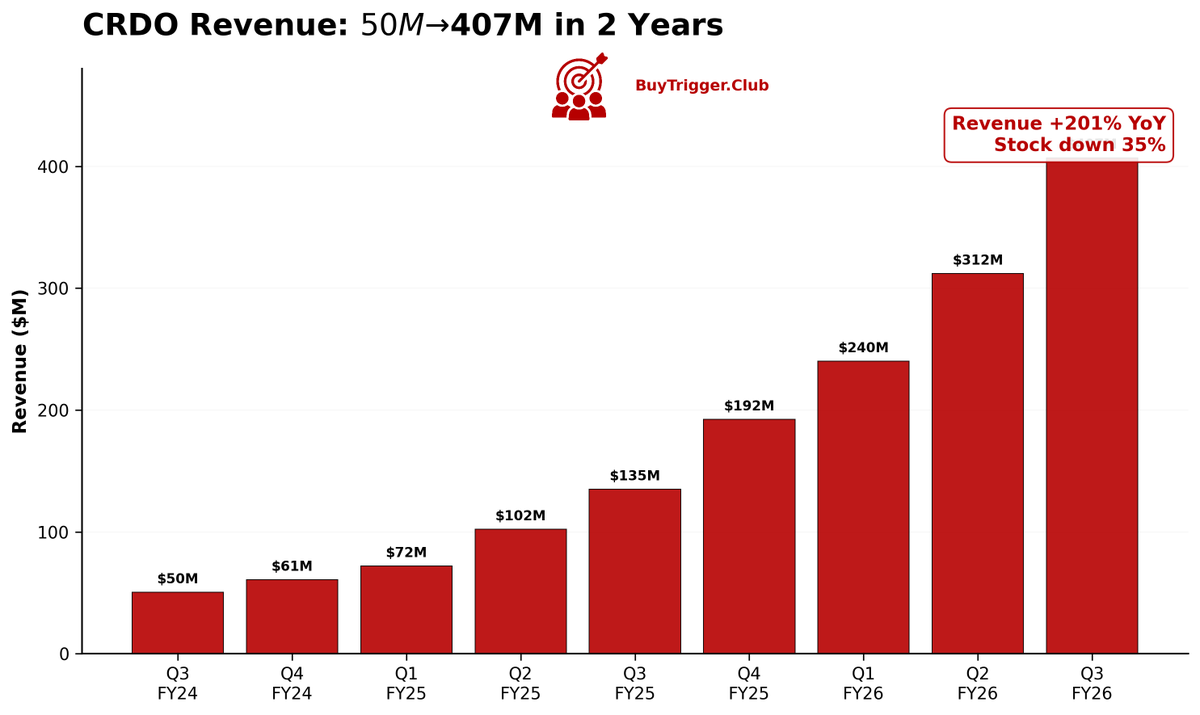

Credo $CRDO Technology grew revenue from $50M to $407M in two years.

That's 201% year-over-year growth. Five hyperscaler customers. Taking market share from incumbents every quarter.

Still in BuyTrigger range.

Full breakdown in my free Substack research article — one of 7 growth stocks I analysed below.

dralexkoh.substack.com/p/my-top-7-gro…

English

Stopped using Perplexity Pro because they were pushing me to pay $200 a month for the same research functionality which I had the last 10 months for work, personal and company research data.

Switch to Gemini for a week and it’s utter 💩 over polished and wrong info because Gemini is so heavy biased.

ChatGPT is the second best in research but not going back there are their model mood swings on revision.

Claude research is like my wife searching the whole internet for discount and come back with nothing and still In dielema.

Now testing Grok but it still feels disjointed as their reasoning is so far behind competition.

All want to say is that compute is the bottleneck here and cost will ever increase. If you are not making money from these LLM you cannot afford it for casual usage.

Buying more $NVDA and $TSM

English

Conana.eth 🔻🔻🔻 retweetledi

Mark Cuban on the next job wave.

Customized AI integration for small to mid-sized companies.

"Software is dead because everything's gonna be customized to your unique utilization. Who's gonna do it for them... And there are 33 mn companies in the US."

English

Conana.eth 🔻🔻🔻 retweetledi

Extra fireworks for an extra birthday 🎆🎊🤣

Starry Snow@StarrySnow303

GM my X frens! Happy TGIF 🥳 Its my birthday today! 🐣🎊 Another year wiser. And younger :D Birthday presents are very welcome 😝 I pray for all my loved ones to stay healthy and happy. Appreciate every one of you here. Stay blessed 🫶🏻

English

@conanahere It’s absolutely crazy - I’m convinced we’re going to see a sudden shift/covid like change this or next year where ai really redefines how we live & work (maybe not live yet) but work definitely

English

seeing seeddance 2.0 blow up on the TL gives me crazy goosebumps…

world is changing quick

industries are dying

new industries free from corporations will emerge

Marco "Shikoba"@shikoba_86

Seedance 2.0 Test text to video Prompt: [Shot 1: Frontal Menacing Shot] A medium shot of a SWAT officer in full tactical gear, gas mask, and helmet. He is pointing his assault rifle directly at the camera lens (breaking the fourth wall). He is shouting with visible intensity: "LET THE HOSTAGE GO! DROP THE WEAPON NOW!" [Shot 2: The Threat] Cut to a medium shot of the killer in a dirty tank top, holding a woman in a chokehold. He has a pistol pressed to her head. He is sweating and manic, screaming at the off-screen officer: "STAY BACK! I'LL KILL HER! I SWEAR I'LL DO IT!" [Shot 3: Over-the-Shoulder Resolution] The camera is positioned directly behind the SWAT officer's right shoulder. We see the back of his helmet and his rifle in the foreground. In the distance (mid-ground), the killer is still visible holding the girl. The killer screams one last time: "I'M GONNA DO IT!" after The officer's rifle kicks back with a single sho and hit head enemy. The killer falls instantly. The girl is left standing, shocked but safe. Technical Style: High-shutter speed action, realistic muzzle flashes, handheld camera shake, 24fps, English dialogue.

English

@benchuchu Definitely work first, and then how we live will be adapted accordingly. It will be so different.

English

Days like this are exactly why you diversify.

A mix of infrastructure.

A mix of AI and banks.

Growth stocks got hit, but the fundamentals are still intact.

Net-net, I’m still up because $VRT, $CRDO, and $GEV held up this week—while I added to $NOW and $HOOD.

Poetry. Discipline in motion.

English

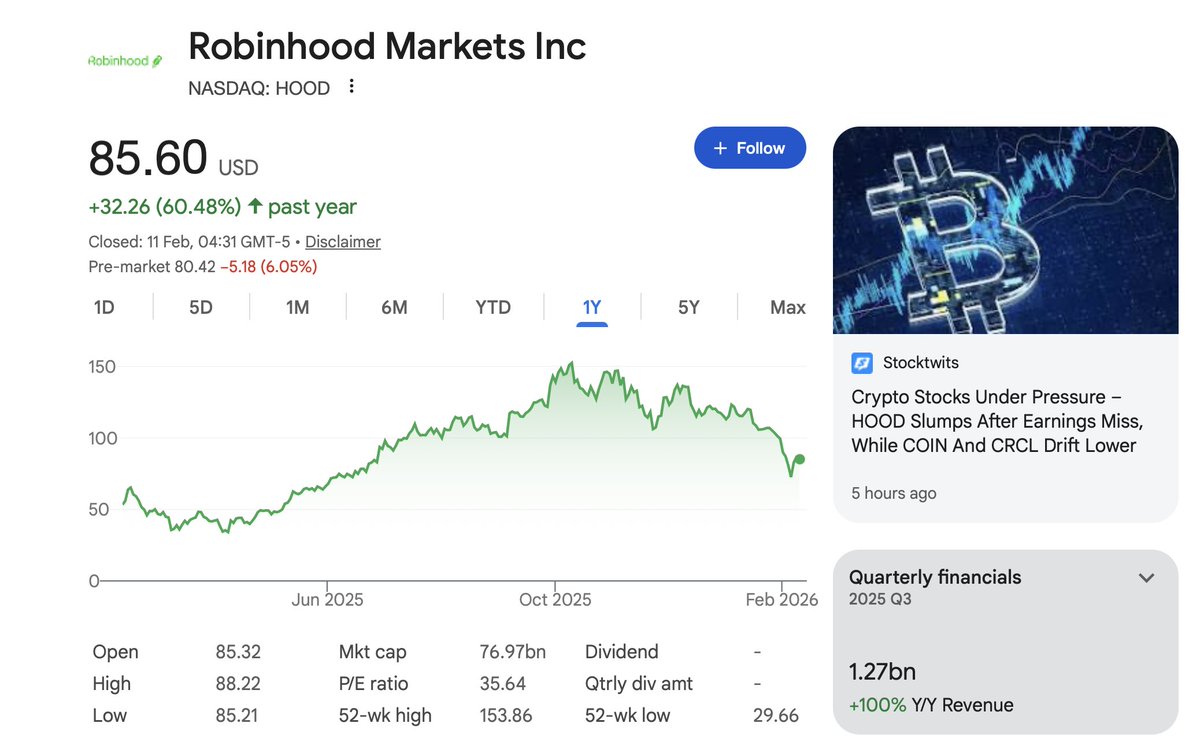

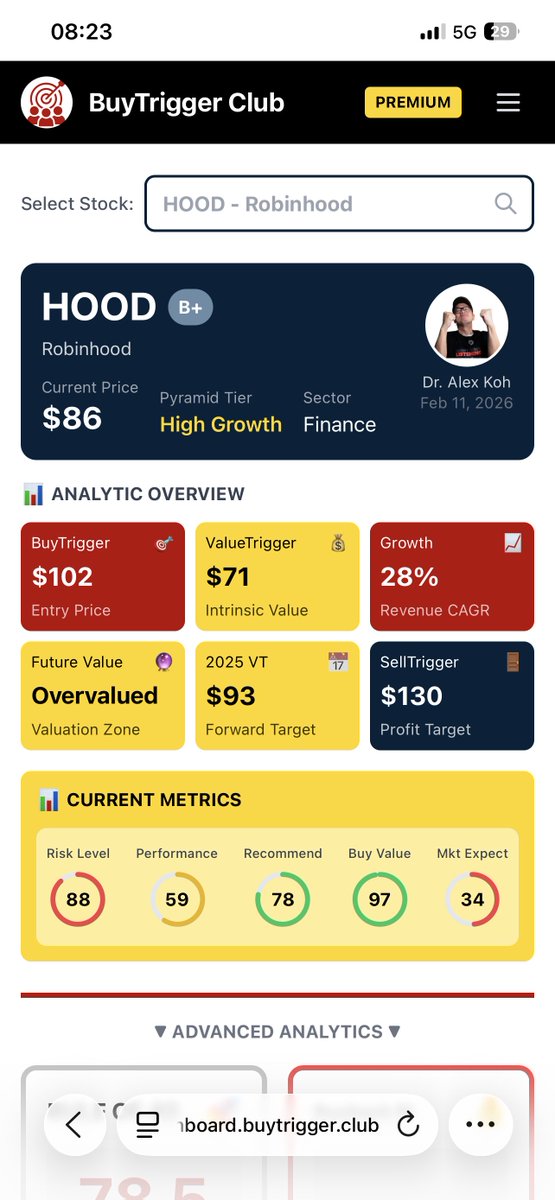

$HOOD down 8% after earnings. Crypto revenue fell 38%. Revenue miss.

But we knew this.

Crypto cooling. Users moving to buy-and-hold. That's actually healthy.

The replacement? Prediction markets up 375% YoY. Super app being built brick by brick.

BuyTrigger: $102

ValueTrigger: $71

At ~$78 overnight — approaching fair value for the first time in ages.

Young team vs banking giants. Give them time.

HOOD will grow. Hold and DCA if you believe in the thesis 🎯

English

Conana.eth 🔻🔻🔻 retweetledi

Why has this cycle felt so different?

I suggest reading “The Trunk Up Thesis”.

Top callers’ worst nightmare.

👉 techdev52.com/p/techdev-news…

English

Conana.eth 🔻🔻🔻 retweetledi

Conana.eth 🔻🔻🔻 retweetledi

say what you want about the @virtuals_io team but they’ve reinvented themselves repeatedly in the span of 12 months:

> first with the AI coin meta

> then as a memecoin launchpad

> and now they’ve pivoted to robotics

each time they’ve been meta leaders and have staged a comeback for $VIRTUAL. comfy betting on founders like @ethermage.

English

Conana.eth 🔻🔻🔻 retweetledi

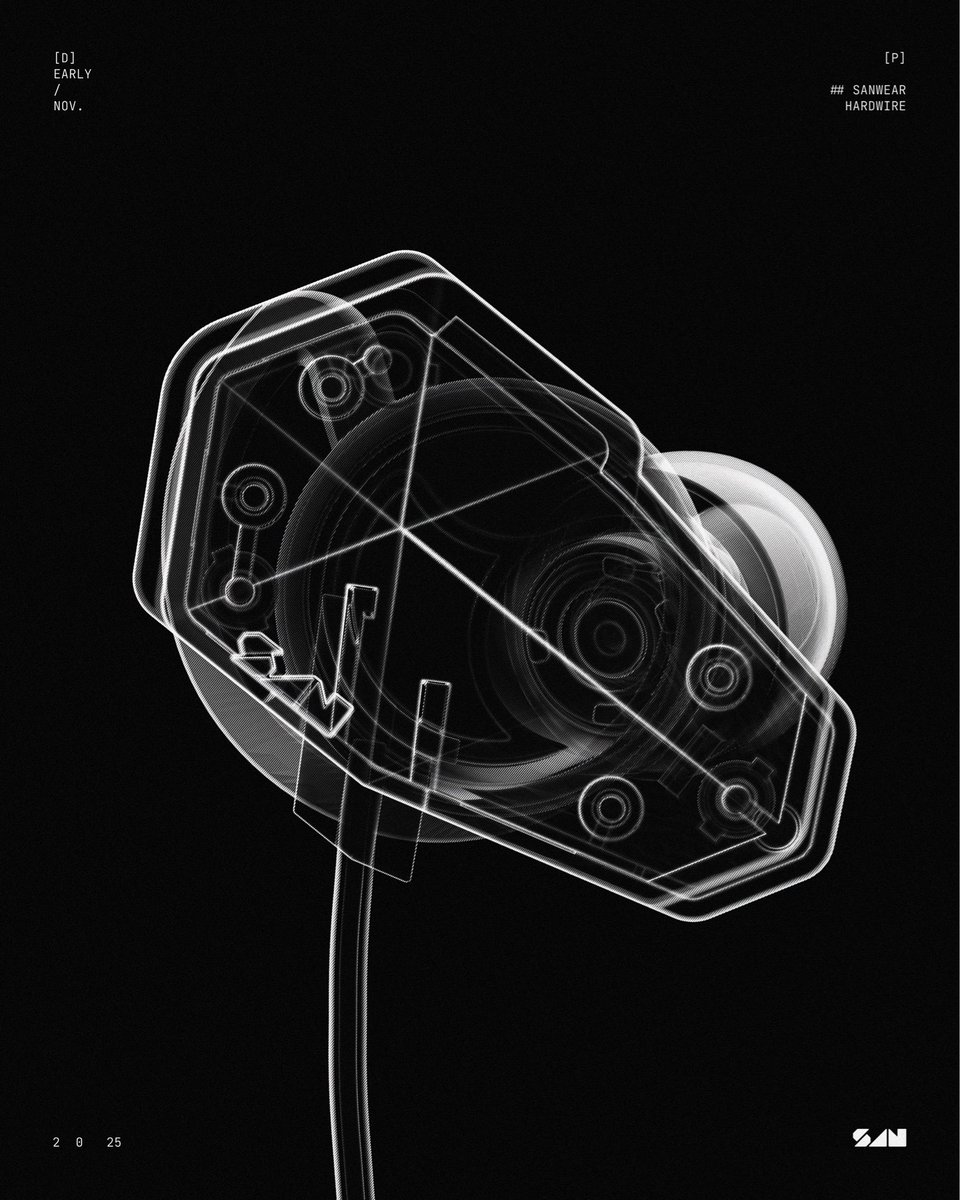

Half the size. Even more power.

At 50% smaller than our wireless SANWEAR models, HARDWIRE delivers the same force… and then some.

Powered by next-generation Planar-Dynamic Drivers and the Audio Cortex, HARDWIRE delivers our signature Holographic Audio: detailed, dynamic, and spatially precise.

English

Conana.eth 🔻🔻🔻 retweetledi

Yuga really dropped an info dump on us in ApeFest and everyone’s loving it

Clubhouse is obviously the major announcement but Amazon partnership is probably the biggest one

But tbh, there’s so much news dropped last night. It’s hard to keep track

I listed them for all below👇

English

Conana.eth 🔻🔻🔻 retweetledi

Wasn't able to attend APEFEST this time, but am always in there in spirit!

@BoredApeYC is still undoubtedly the best club in the world! Very excited for the future with the developments announced today.

Have fun APES! 🍌🍌🍌

English

Salty Soldier reporting for duty at ApeFest this year without my usual crew. If you see me looking lost, do holler at me.

See y’all in abit apes! 🫡

English

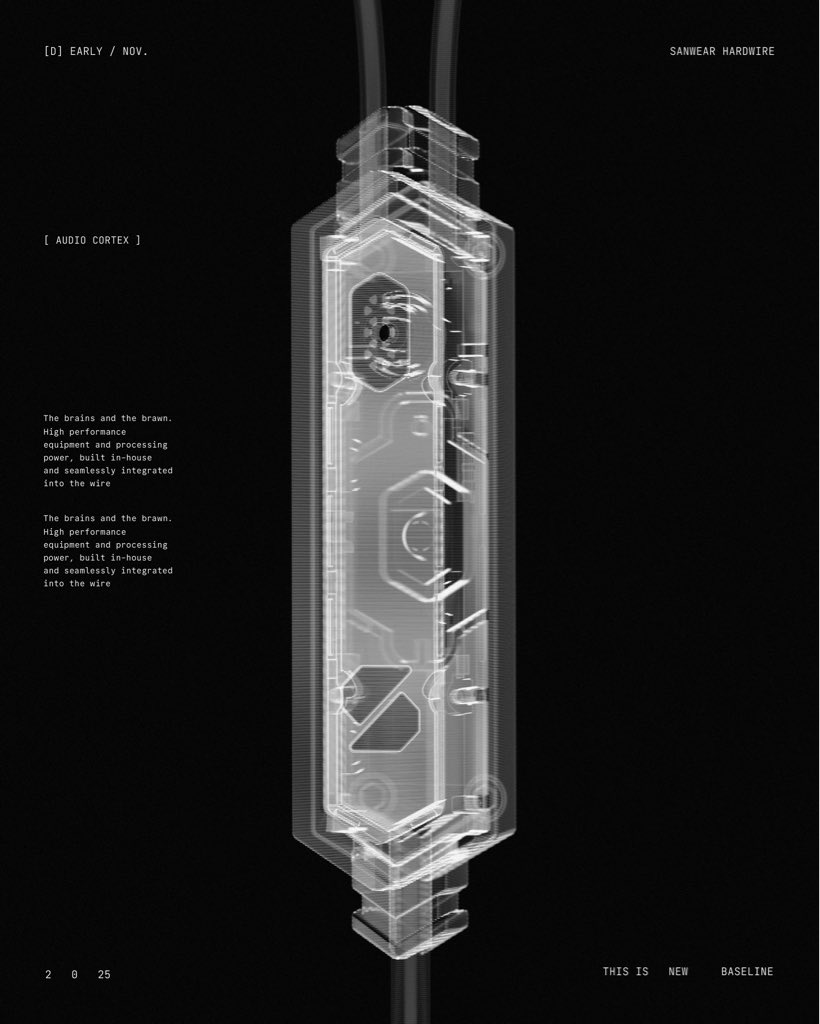

The Audio Cortex — the beating heart and mind of our wired system.

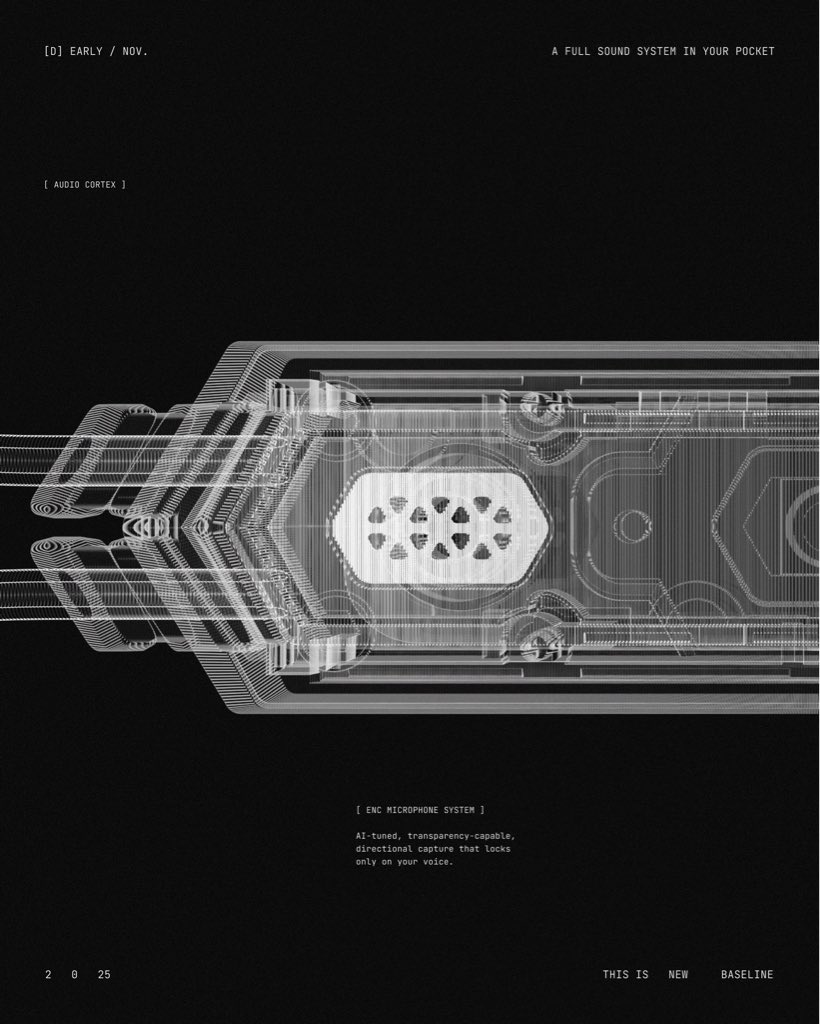

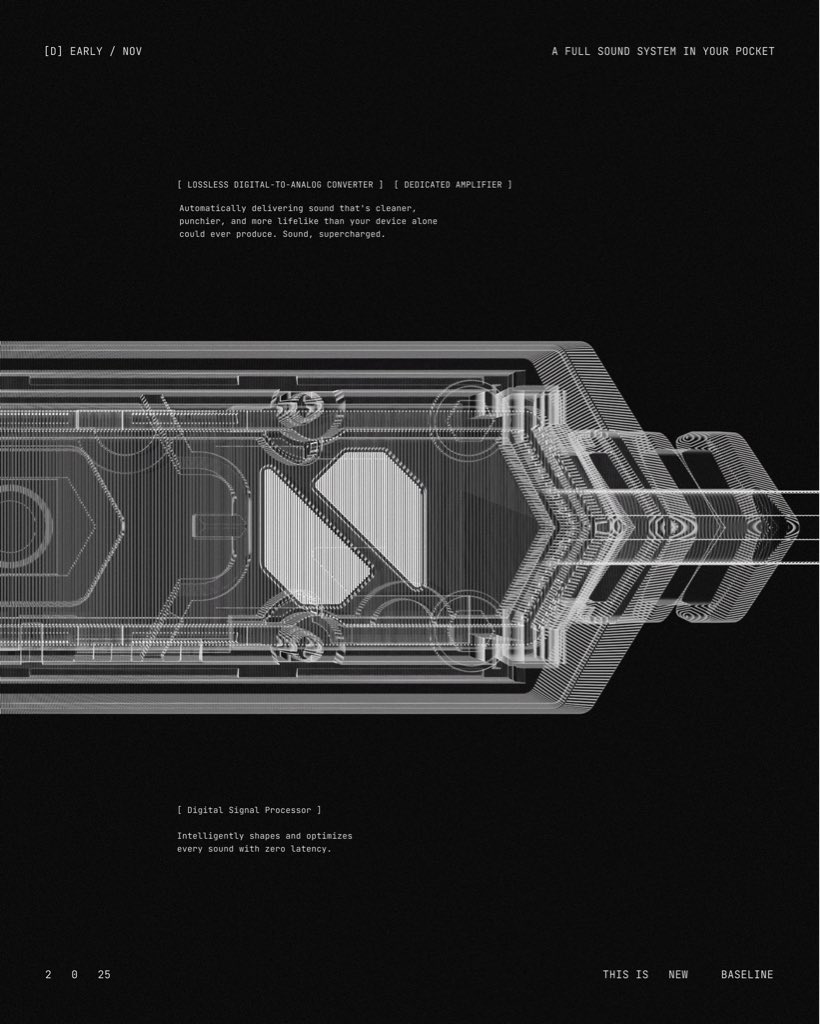

This first-of-its-kind feature seamlessly integrates an amplifier, lossless digital-to-analog converter (DAC), digital signal processor (DSP), Environmental Noise Cancellation (ENC) microphone, and programmable action button into a single elegant unit.

Supercharge your sound.

English