Cory Wake

836 posts

Cory Wake

@coryDwake

Co-Founder @ Silver Wave Capital, a senior housing investment firm | Exploring the Aging Economy | Mailing List ⬇️

Davis, CA Katılım Mart 2014

227 Takip Edilen1.1K Takipçiler

@joepohlen Posted with a lengthy delay

x.com/coryDwake/stat…

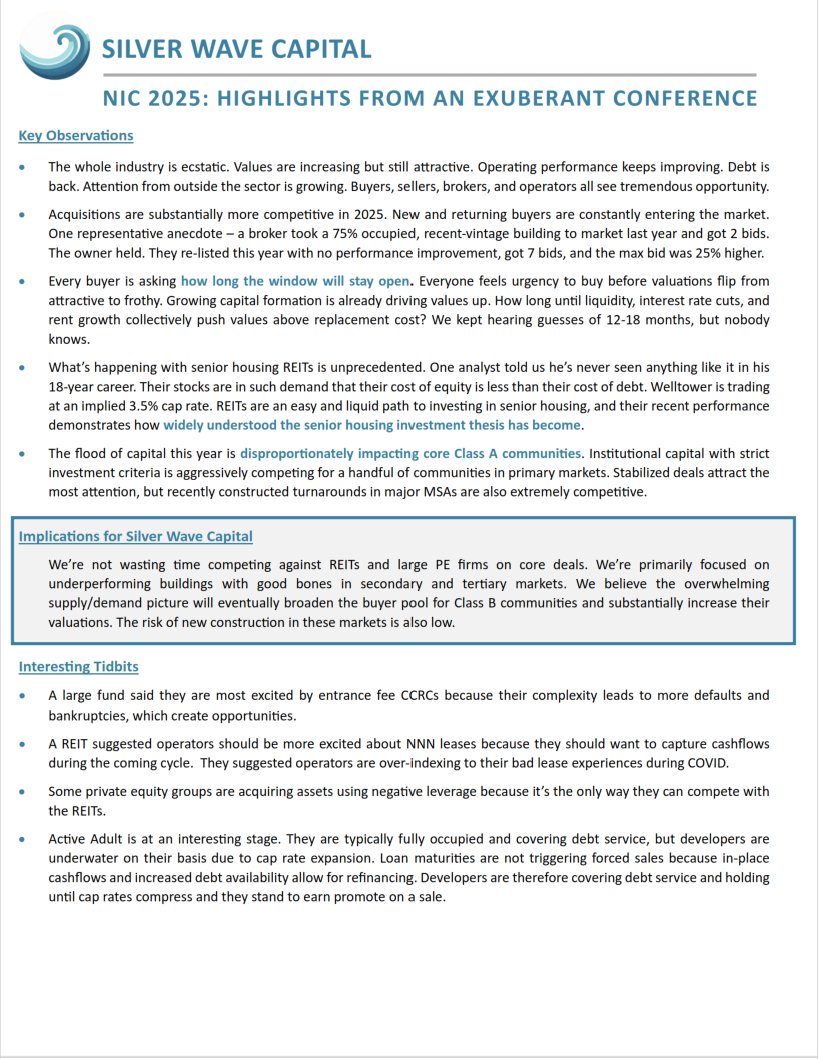

Cory Wake@coryDwake

Our takeaways from the NIC 2025 conference on senior housing:

English

Good first day at the NIC conference.

Lot of excitement around the industry. General sentiment is that we’ve endured long enough. Now is our time.

Looking first to reading @coryDwake recap on the event.

English

@coryDwake I agree - everyone obviously has their own interests, but given the economy/inflation was the hot topic of the last election it seems risky to push when everything is humming right now

English

To those calling for rate cuts - given we are at relatively normal levels on a historical perspective, are we not at all concerned about spurring inflation?

Or is that the point, and we know the only way out of our debt levels is to inflate our way out of it? I get that it cuts interest expense and understand everyone wants the resulting higher asset valuations, but no one seems concerned…

English

I think I'm in the process of learning the power of hyper-local banking relationships. I got a term sheet last week from one and, relative to national banks:

5-10% higher LTC

50 bps lower SOFR spread

And.... zero prepayment penalties!

Plus the banker felt like Grandpa.

English

A senior housing broker succinctly summarized for me the difference between 2024 and 2025:

In 2024, the market had a per-unit cap of $300k. Transactions prices above that cap were scarce.

In 2025, that cap is gone.

Our internal data agrees. On an annualized basis, we see over 4x more deals with guidance above the cap this year.

(Granted this is guidance, not trade price. Still - instructive.)

English

@coryDwake This doesn’t take into consideration how hyper local the business has always been.

There will be markets with appropriate supply and some markets that will be very out of balance.

English

Another framing of the tremendous supply/demand growth imbalance in senior housing right now:

Unit construction required to meet demand by 2030: 564,000

Units constructed by 2030 at current development pace: 191,000

We will need 3x more units than are on track to be built

English

@coryDwake Congrats! Signed one a few weeks ago too. It's crazy to think how hard it is to get to an accepted LOI and then it's even harder to get it from there to actually across the finish line. Wishing you continued good luck!

English

Cory Wake retweetledi

Deal Pricing vs. Reality

@coryDwake and his partner Elan dug into 51 closed senior housing deals since January 2024 where they had both broker guidance and the actual sale price. That’s out of 330 reviewed deals (closing price is notoriously hard to pin down).

What did they find?

•23 traded below guidance

•9 traded at guidance

•19 traded above guidance

•Only 12 landed within a tight ±10% band

Most common outcome? Deals going 5–10% below what brokers were guiding.

What predicts that spread?

They looked at the “Transaction Delta” vs. revPOR, facility size, NOI margin, and vintage.

The results:

•No clear relationship with revPOR or size

•Some correlation with vintage (newer = better)

•Erratic link with NOI margin—except at the low end, where poor margins led to steeper discounts

Two big takeaways:

1.Pricing is more normally distributed around guidance than you’d expect.

2.Newer builds are more likely to beat guidance.

Caveat: This doesn’t capture deals that didn’t close because the price was just too high—but it’s still a super useful lens on the market.

Nice work Cory and Elan.

English

@coryDwake Great to know.

If your modeling template is still available, please include me, Cory.

English

Last year we solved a problem that was limiting us as a small team: we were wasting too many hours in Excel underwriting deals that never went anywhere.

When a deal piques our interest, we want to test the numbers and tweak assumptions. For too long, we did that by jumping straight to full discounted cashflow underwritings. We’d spend 3-5 hours building a model that was unnecessarily complex.

For raising capital, you need a DCF model. For vetting deals, talking to operators, and submitting LOIs, you don’t. We needed a faster, 80/20 analysis that told us what we needed to know without bogging us down.

Thus, the SWC Roll-Up Analysis was born.

Shown below, this simple dashboard gives us the key info needed for deciding whether to pursue or pass, and the analysis takes an hour at most. We just pull in historical financials, tweak the adjustable inputs, and make minor deal-specific changes.

What results is a 360-view of the deal, including:

• Trended historical financials, including revenue and expenses per occupied unit.

• A pro forma sketch based on 3 simple inputs: occupancy, rate growth, and operating margin. It’s not perfect, but it grounds our expectations.

• Asset info including unit mix, vintage, pricing guidance, and potential bid amount (including cap rates and price-per-unit).

• Sources and Uses.

• Debt assumptions (in this example we’re underwriting a bridge-to-HUD, so we include both the bridge and HUD loan).

• NOI-to-cashflow conversion estimates.

• Historical and projected cash-on-cash return based on our assumed capital stack.

• If we have square footage, we include a discount-to-replacement-cost estimate using NICMap construction cost data.

With this model our throughput significantly increased without reducing the quality of our analysis.

We’re happy to share the template with anyone. If interested, reply/DM me and I'll send you a link.

English