Critic Bro

3.6K posts

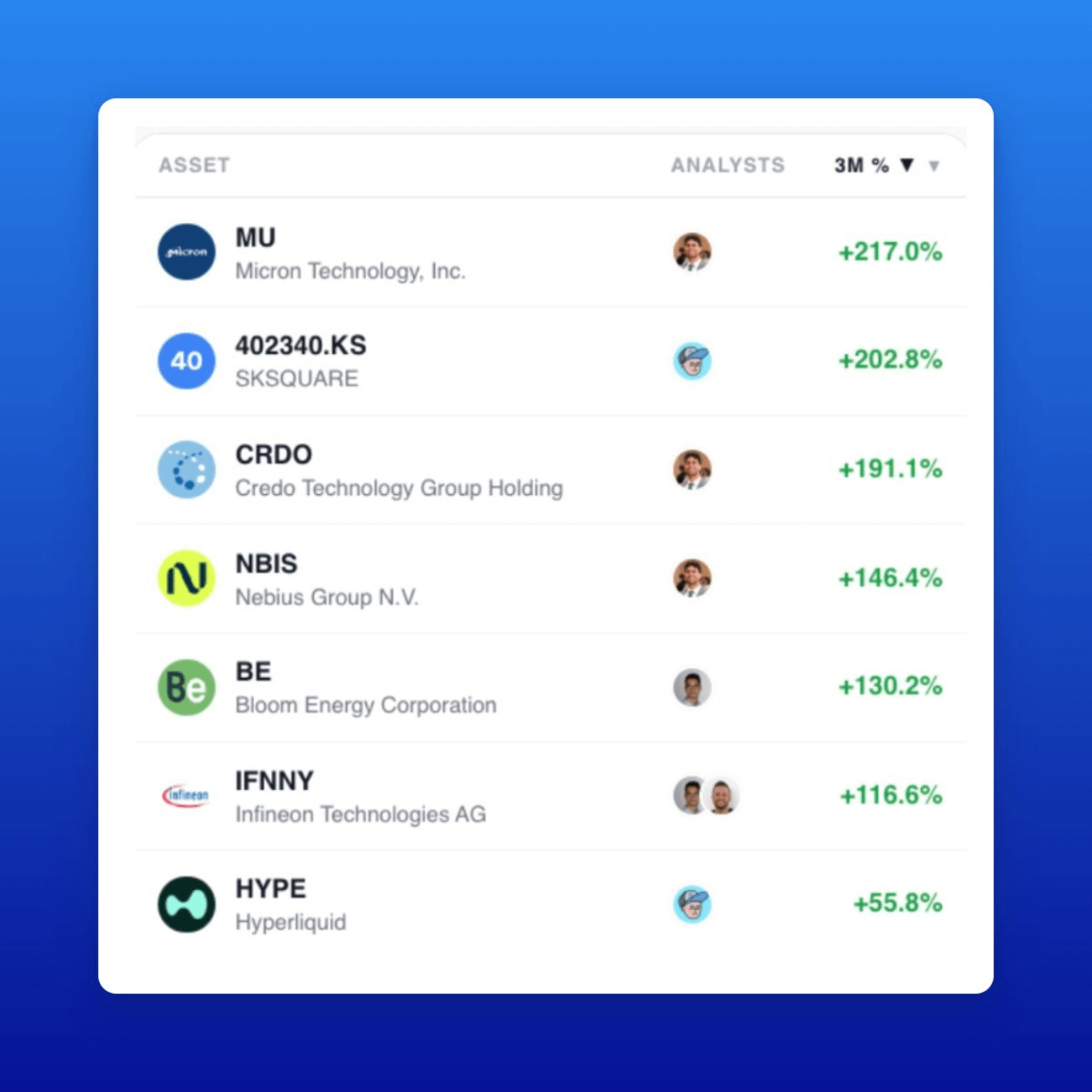

We called Nebius, Credo, Bloom Energy, AAOI, and AMD before their big run ups.

Don’t miss the next one, come join us for just a $1. milkroad.com/pro/?utm_mediu…

English

Chamath has been watching SpaceX for 15 years and he thinks the market is still not close to understanding what it actually is (Save this).

The first argument is the industrial logic of a Tesla SpaceX combination.

One capital structure, one balance sheet, one vehicle to raise money across robotics, autonomous vehicles, energy, AI, and launch.

@chamath argument is that markets are treating this as a peripheral possibility rather than an obvious strategic inevitability.

The second is Starlink Direct to Cell, which he believes will generate enormous domestic cellular revenue before most of the bigger SpaceX narratives even begin to materialize.

The numbers already back this up.

Starlink has over 10 million Direct to Cell monthly active users with live partnerships with T-Mobile, Rogers and Optus standard smartphones connecting directly to satellites with no special hardware required.

SpaceX is currently deploying approximately 340 Direct to Cell satellites per month, targeting 25 million monthly active users by end of 2026.

Goldman forecasts SpaceX's AI division will generate $15.6 billion in 2026, rising to $34.5 billion in 2027 and accelerating to $322 billion by 2030 roughly a 100-fold increase in five years.

Total SpaceX revenue hits $474 billion by 2030, up from $18.7 billion in 2025.

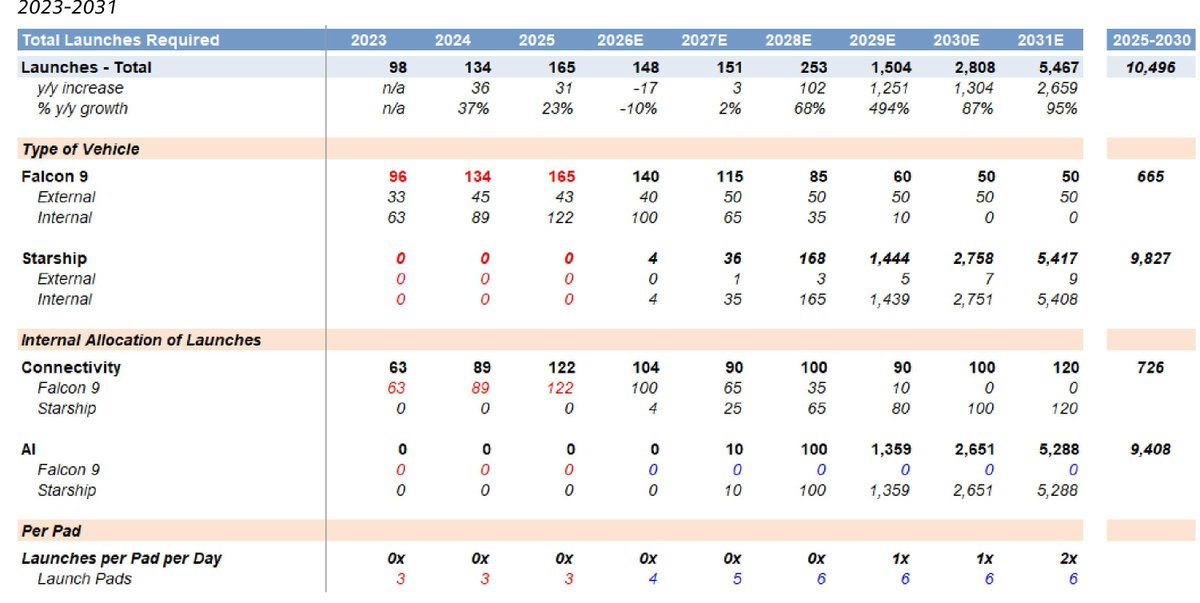

The launch cadence numbers are where this gets staggering.

SpaceX is expected to execute 151 Starship launches in 2027, scaling to 253 in 2028, then 1,504 in 2029, 2,808 in 2030, and 5,467 in 2031.

Goldman projects 5,288 of those 2031 launches will be dedicated Starship AI missions each carrying 30 to 50 satellites powered by one GB300 equivalent compute rack apiece.

The cost per kilogram to orbit falls below $100 as reusability matures, compared to $1,500 per kilogram on Falcon 9 today.

Morgan Stanley projected a 24-hour turnaround by late 2027, enabling the kind of cadence these numbers require.

That launch cost collapse is what makes the orbital AI compute thesis real @elonmusk

English

We called Nebius, Credo, Bloom Energy, AAOI, and AMD before their big run ups.

Don’t miss the next one, come join us for just a $1. link.milkroad.com/3hw8m0

English

In the coming years, $SPCX will become the most valuable company in the world (Save this).

From 2023 to 2026, SpaceX's total annual launch count runs between 98 and 165.

But now they're ramping it up.

SpaceX is expected to do 151 launches in 2027. Then 253 in 2028. 1,504 in 2029. 2,808 in 2030. 5,467 in 2031.

The primary aim to ramp this up is to launch its own AI data centers into orbit via Starship.

This is their rationale:

Ground-based AI data centers have three hard limits:

1. Grid power takes 5 years to get connected.

2. Cooling water is running out in major markets.

3. Land generates local opposition that can kill a project before it breaks ground.

Launching data centres into space solves all three problems at once.

Each AI satellite runs on direct solar power, radiates heat into the cold of space for free and can be deployed to serve anywhere on Earth without a single permit.

SpaceX's first AI satellite, called AI1, targets 150 kilowatts of compute performance which is roughly equivalent to one NVIDIA GB300 rack. It has a 70-meter wingspan and uses the same laser inter-satellite link technology already proven across the Starlink network. The first generation runs on NVIDIA chips.

$NVDA is the most direct play. Every AI satellite in the first generation uses NVIDIA compute and every subsequent generation will require whatever NVIDIA's most advanced chips are at the time.

Micron and SK Hynix supply the HBM memory that goes into every satellite payload.

Standard commercial chips fail in space due to radiation. Every NVIDIA chip that goes into orbit needs radiation-hardened support components around it that only a handful of companies can supply. Redwire, Mercury Systems, and AXT are the smaller specialized names in that category.

Milk Road remains bullish on $SPCX. If you want our full AI trade list, check the link in the first comment.

English

Imagine getting stabbed over a bad stock pick.

GURGAVIN@gurgavin

A SOUTH KOREAN FINANCIAL YOUTUBER WAS JUST STABBED MULTIPLE TIMES BY ONE OF HIS SUBSCRIBERS THE SUBSCRIBER LOST MONEY FOLLOWING HIS STOCK PICKS 😭😭😭😭

English

We called Nebius, Credo, Bloom Energy, AAOI, and AMD before their big run ups.

Don’t miss the next one, come join us for just a $1. milkroad.com/pro/?utm_mediu…

English

AAOI just dropped the news that changes the entire capacity conversation and the market hasn't fully reacted yet (Save this).

Applied Optoelectronics announced it has broken ground on two adjacent properties in Pearland, Texas, adding nearly 400,000 square feet of new manufacturing capacity dedicated entirely to scaling 800G and 1.6T optical transceiver production.

As their CFO said it, these facilities will be instrumental in supporting their long-term growth strategy and strengthening AOI's position as a key supplier to the AI and cloud infrastructure markets.

The capacity timeline that this supports is staggering.

AAOI started Q1 2026 at 100,000 units of monthly transceiver capacity.

By end of 2026 they are targeting 650,000+ units per month and by 2027 that number hits 930,000+ units per month.

At those production levels, analysts are modeling $471 million in monthly transceiver revenue by mid-2027, if execution holds.

The bear case on AAOI has always been management execution risk this company has a history that makes investors nervous but they are progressing along exactly the timeline the bull case required several quarters ago.

Revenue hit a record $151M in Q1 2026, up 51% year over year, with Q2 guided to $180–$198M and the full year 2026 target is over $1 billion.

The Pearland announcement is the physical proof that the ramp is real.

AAOI is the toll road, the hyperscalers are the trucks and today they just broke ground on a second highway.

Bullish on AAOI, and come join Milk Road Pro to get our full AI thesis for just a dollar using the link below!

English

Our very own Chief Legal Officer is testifying in front of the United States Congress this Friday 👇

Sarah Aberg 🎈@SarahAberg1

Looking forward to testifying Friday before the House Financial Services Committee on the CLARITY Act and sharing @helium's perspective on what clear digital asset rules mean for companies building real things. Hearing details here: financialservices.house.gov/calendar/event…

English

Tom Lee: AI stocks up... Software up... War happening...

All three should have been rocket fuel for crypto - and yet crypto crashed anyway.

"In wartime situations, we should expect to see gold and Bitcoin do well. But instead, crypto's done really badly."

Tom's theory: the industry never truly recovered from the FTX collapse.

People lost money and simply can't come back yet.

FT @CryptoMichNL @fundstrat @new_era_finance.

Milk Road@milkroaddaily

Haseeb: People claim current crypto sentiment is worse than after FTX collapsed... "I think it's complete bullsh*t." "It's just total recency bias because yeah, it's happening right now, so therefore it's worse." You don't remember how many people had no choice but to quit after FTX - they lost everything. FT @KevinWSHPod @hosseeb @dragonfly_xyz.

English

@KyleReidhead 1. not everyone

2. coreweave is an even bigger gift looking at the past 1y chart

English

$NBIS down 35% is a gift and it's going above $300 soon

Everyone thinks Meta just killed Nebius, it didn't

The company that supposedly declared war on Nebius signed a deal to BUY up to $27 billion of Nebius capacity less than 4 months ago

Here's what happened and why $NBIS is a must buy

On July 1, Bloomberg reported Meta is building "Meta Compute," a plan to rent out spare GPU capacity to outside customers

Nebius fell 17% in a single day, roughly $12 billion in market value erased, and kept sliding from its June peak of $300 down below $200 in 3 weeks

The market read that headline as competition, but Meta is actually just becoming an even bigger customer

In March, Meta signed a 5 year deal with Nebius worth up to $27 billion, with $12 billion of it dedicated capacity. Companies do not hand $27 billion to a supplier they plan to destroy. Meta is renting because even while spending $125-145 billion on AI infrastructure this year, it cannot build compute fast enough

And while the stock fell 30%, the business continues to accelerate (expanding in Europe and potentially India)

Q1 revenue grew 684% year over year to $399 million (wow). AI cloud revenue grew 841% and AI cloud ARR hit $1.92 billion, up 54% in a single quarter

Management reiterated $7-9 billion in ARR exiting 2026 and raised capex to $20-25 billion for one reason, demand keeps outrunning supply. Contracted power passed 3.5 gigawatts, targeting over 4 by year end. Capacity is effectively sold out before it gets built

But the part that matters the most is: the backlog

Over $46 billion in signed long term contracts. Microsoft at $17.4 billion, expandable to $19.4 billion. Meta at up to $27 billion. And this morning, a fresh $1 billion compute deal with Reflection AI

The stock repriced down 35%, yet the contracted revenue repriced 0% (if anything it grew)

Getting back to $300 only requires the multiple the market was happily paying 3 weeks ago, applied to numbers that are bigger today. This should be a no brainer as long as you think AI capex continues or grows (which I do)

The analysts at Milk Road PRO bought $NBIS at $130 earlier this year and have continued to add to their positions. You can track our real time analysis and portfolios for just $1 in Milk Road PRO

Don't miss out!

English

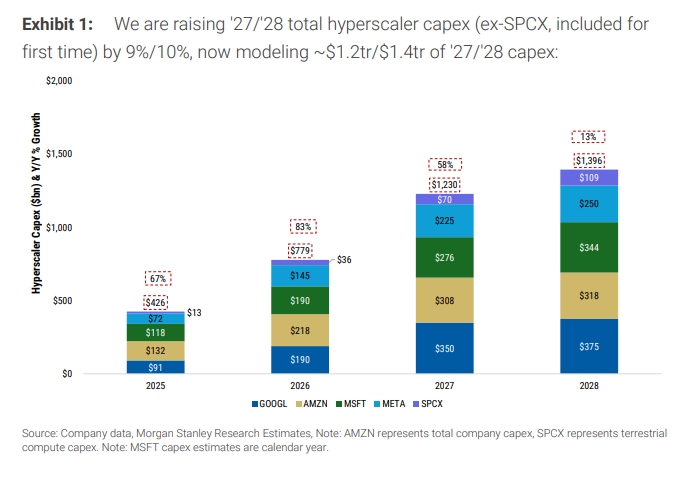

Morgan Stanley just dropped numbers that should make every investor pay attention (Save this).

Hyperscalers spent $261B in 2024, they're now projected to spend $1.4T in 2028, a 5x increase in four years and that doesn't even include OpenAI or Anthropic.

For the first time, Morgan Stanley is classifying SpaceX as a legitimate hyperscaler alongside Google, Amazon, Microsoft, and Meta.

All of it flows into chips, data centers and memory and the supply chain companies sitting beneath the hyperscalers are the ones that will compound quietly.

The most underrated play is memory.

Micron is the only American HBM supplier, giving it a structural edge in government AI contracts that Samsung and SK Hynix cannot touch.

Its entire 2026 HBM4 production is already sold out, revenue nearly tripled to $23.9B, and the memory prices are roughly doubling every year.

The cooling problem is one of the most profitable bottlenecks in this entire trade.

Vertiv makes the power management, liquid cooling systems and racks that keep GPU clusters from melting and it's up over 100% year to date in 2026 with a $15B+ backlog and guidance raised to $13.5–$14B in full year revenue.

Arista Networks (ANET) is the networking infrastructure play, every AI data center needs ultra high speed networking fabric to connect thousands of GPUs together

And Arista just doubled its 2026 AI revenue target as the industry shifts from proprietary InfiniBand to Open Ethernet, a shift that plays directly into Arista's strengths.

Astera Labs solves the interconnect bottleneck inside data centers, the problem of getting data between chips fast enough to keep up with the GPUs.

Revenue grew 93% year over year, it's already profitable, and its customers are Microsoft and Amazon directly.

The hyperscalers are the miners and the real money is in the companies selling them the shovels, the electricity, the memory, the cooling, the networking, and the custom silicon.

Make sure to follow me @melvininvests for more underrated infrastructure plays.

English

@milkroaddaily only jordi compares ai with fracking. dont see that comparison elsewhere often in tech

English

Jordi Visser: People keep comparing AI compute investment to fracking in oil.

It's the wrong analogy.

"Oil is oil. Intelligence is everything."

Oil demand grows linearly with GDP. AI usage grows exponentially with every model advancement.

When token prices drop, usage explodes. Oil doesn't work that way.

The only thing constraining AI is the physical supply of data centers and gas turbines - and those can't be built fast enough.

FT @APompliano @jvisserlabs.

Milk Road@milkroaddaily

Eric Schmidt got booed every time he mentioned AI in his commencement address. His response: "Guys, you can boo me all you want, but this is going to be your reality." Mike Novogratz sees AI as "disruptive as heck" but the power demand story is undeniable. AI agents, driverless cars, robots - "the token usage just explodes." His bull thesis on data centers is simple: There's no future with less power. FT @Novogratz @GalaxyHQ.

English

The Marinade portfolio page, rebuilt.

• Performance chart on by default

• mSOL now in your wallet balance

• Send and receive any Solana token, in-app

Your whole staking picture in one place. More from our own @azikmund 👇

Albert Zikmund@azikmund

Launching a revamped portfolio page today. Here are some of the quality-of-life improvements we packed in 🧵

English

Clearstream added Litecoin to regulated institutional custody this month.

It is one of two international central securities depositories globally, the post-trade settlement layer under Deutsche Börse, holding over 15 trillion euros in assets.

$LTC now settles through that system via @CryptoFinanceAG, the MiCAR-licensed sub custodian in the group, which means institutions custody it inside their existing account with no separate crypto counterparty.

Settlement access is the unglamorous gate every allocation passes through, and Litecoin is now on the right side of it.

Payments. Privacy. Hard money.

English

Marinade Portfolio updates

- portfolio change over time

- usd/sol

- wallet balance

- receive crypto

- send crypto

- should I go on?

Albert Zikmund@azikmund

Launching a revamped portfolio page today. Here are some of the quality-of-life improvements we packed in 🧵

English

Liquidity is one of the clearest signals of where onchain markets are forming.

Today, that signal points to Solana.

Fast, global and built for markets that never sleep.

Solana szn 😎

Cointelegraph@Cointelegraph

⚡️ UPDATE: Solana ranked first in 24-hour DEX volume with $4.15 billion, followed by BNB Chain and Robinhood Chain.

English

@EquityBrian still outperforming four, baba, vnet, csu over the past year

English

We called Nebius, Credo, Bloom Energy, AAOI, and AMD before their big run ups.

Don’t miss the next one, come join us for just a $1. link.milkroad.com/3hw8m0

English

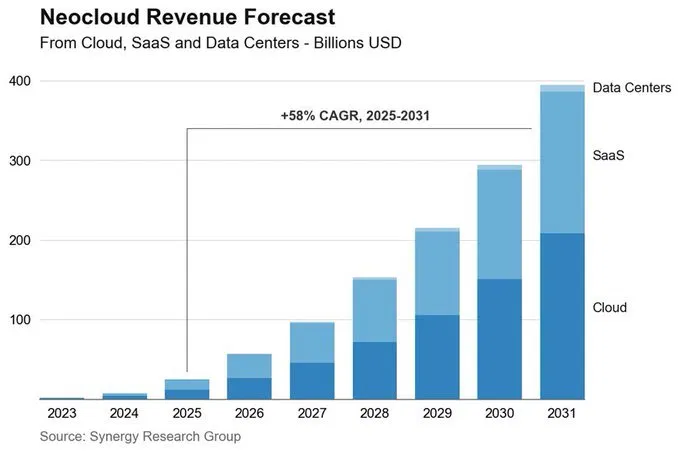

$NBIS will reach $300 in 2026 (Save this).

AI startup Reflection has just signed a deal worth more than $1B to secure compute capacity from Nebius.

This also includes access to Nvidia GB300 chips through 2029.

Nebius did $25B in revenue in 2025 (223% YoY) and now, Synergy Research projects it approaches $400B by 2031.

Out of all the names in the neocloud space, our analysts are betting on $NBIS.

This is their rationale:

Most neocloud companies like CoreWeave, Iren and Cipher mining follow the same playbook. They rent GPUs by the hour, mark them up, repeat.

But $NBIS is different.

It owns the infrastructure, designs its own rack architecture and optimizes the software layer on top. It owns the whole stack, top to bottom.

This gives them a strong competitive edge as owning the entire stack gives Nebius more control over performance and better economics as demand scales. For that matter, anyone with large capital can replicate the pure GPU rental business.

With $49B in contracted backlog from Meta and Microsoft, $NBIS is sitting on the top of the neocloud trade.

In the last market dip, our analyst doubled down on his Nebius position. He is already up 42% on his position but he wants more.

Inside Milk Road PRO, you can see exactly how he is playing his Nebius position along with his other AI stocks.

Join PRO for just $1 (link in first comment below).

Shay Boloor@StockSavvyShay

$NBIS has secured a $1B+ AI compute deal with Reflection AI through 2029 providing access to $NVDA GB300 chips. Reflection is building open-source models to compete with OpenAI and Anthropic.

English

We called Nebius, Credo, Bloom Energy, AAOI, and AMD before their big run ups.

Don’t miss the next one, come join us for just a $1. milkroad.com/pro/?utm_mediu…

English

This Morgan Stanley chart is probably the most important single slide in investing right now (Save this).

Morgan Stanley just raised its 2027 and 2028 hyperscaler capex estimates by 9% and 10% respectively and the new numbers: $1.23 trillion in 2027 and $1.4 trillion in 2028.

Those figures include SpaceX terrestrial compute capex for the first time, a new entrant Morgan Stanley is now treating as a legitimate hyperscaler class spender alongside Amazon, Google, Microsoft and Meta.

To put the trajectory in context: hyperscalers spent $261 billion in 2024 and now projected to spend $1.4 trillion in 2028 which is a 5x increase in four years.

Now, who captures this spending and how could you benefit from all of this?

NVIDIA is the most direct beneficiary, every dollar of AI compute capex disproportionately flows through GPU purchases first.

Goldman Sachs estimates semiconductor sales revisions for 2026 are already up approximately 60% as a result of these capex uplifts and the $1.2-1.4 trillion spending level creates demand visibility essentially locked in 18-24 months forward.

Micron and SK Hynix are the memory layer, every NVIDIA GPU requires HBM, high bandwidth memory stacked directly on the chip package and there is no substitute.

Micron's HBM3E is now shipping at scale into the GB300 ecosystem and SK Hynix continues to dominate HBM supply overall.

As capex scales toward $1.4 trillion, HBM demand scales in direct proportion and Micron is the most accessible US-listed pure-play on this dynamic.

Broadcom captures the custom silicon and networking layer.

Google TPUs, Amazon Trainium, Meta MTIA, every major hyperscaler custom AI chip program runs through Broadcom for networking silicon and packaging.

As total capex grows and custom silicon share within it grows, Broadcom's addressable market expands on both axes simultaneously.

Marvell captures the optical DSP and custom ASIC layer specifically the photonic engines and SerDes that connect GPU clusters together at scale.

Fiscal 2027 revenue is tracking toward $11 billion, $15 billion guided for fiscal 2028, driven almost entirely by hyperscaler AI commitments already in backlog.

Vertiv and Eaton capture power and cooling infrastructure, every GPU cluster requires thermal management and power distribution at roughly $0.30-0.40 of infrastructure spend per dollar of compute.

At $1.4 trillion total capex, that translates to $400-550 billion flowing into power and cooling infrastructure over the next two years.

The infrastructure suppliers get paid regardless of whether AI ROI materializes while the hyperscalers bear the risk.

That asymmetry is the core reason the picks and shovels trade remains compelling even at current valuations.

Milk Pro Subscribers are up massively on these trades and come join us using the link below to get our full AI trades and today is the last day to get 33% off.

English

We called Nebius, Credo, Bloom Energy, AAOI, and AMD before their big run ups.

Don’t miss the next one, come join us for just a $1. milkroad.com/pro/?utm_mediu…

English

Tom Lee just went on CNBC and said buy every dip in Korea, SK Hynix, and Samsung and here is why he is right (Save this).

SK Hynix controls approximately 60% of the global HBM market and reported an operating margin of 72% in Q1 2026 and its entire HBM supply through 2026 is fully contracted.

The selloff is technical driven by Korean retail leveraged ETF mechanics not a deterioration in the underlying business.

The ADR listing is the structural event that changes the stock's trajectory.

SK Hynix listed on Nasdaq under ticker SKHY on July 10, raising $29.65 billion, the largest foreign ADR offering in history, surpassing Alibaba's 2014 debut.

Until this listing, most American institutional capital was categorically unable to own SK Hynix.

Pension funds, index funds, and insurance companies operating under US listed only mandates had no direct path to the dominant AI memory company in the world and that changes overnight.

SK Hynix trades at 6.2x forward P/E versus Micron's 7x, despite holding the superior position in HBM and that discount closes as passive inflows materialize.

The core argument across all of it, unless memory and semiconductors are no longer central to AI and there is no replacement in sight there is no reason to be worried about Korea, SK Hynix, or Samsung.

Every dip is buyable and Milk Road Pro members are up massively on these trades, come join Milk Road Pro for just a dollar using the link below to get our full trades.

English

Earning on stablecoins doesn't need to be hard.

Deposit USDT, USDC or USDe to EarnUSD for daily, USD-denominated rewards from a diversified selection of blue-chip DeFi protocols.

stake.lido.fi/earn/usd/depos…

English

Crypto moves 24/7. Humans don’t.

That’s why Aethir Claw introduced CARA: a pre-built crypto AI agent designed for market monitoring, wallet tracking, project research, social feeds, and Web3 workflows.

No manual skill setup.

No complex deployment.

Just a crypto-native agent running on Aethir’s decentralized cloud.

English

Institutional adoption doesn't arrive as a smooth climb, it comes in steps, and this is one of them.

When an allocator can hold $LTC inside the same account as their bonds, with no new counterparty to onboard, the operational reason to stay out is just gone.

That barrier was never really about conviction, it was about whether the plumbing existed, and now it does.

Talk to enough allocators and you learn it's never the vision that stops them, it's the operational headache. Watching that headache quietly disappear for Litecoin is a good day uk.

WELCOME TO THE LITECOIN INSTITUTIONAL ERA.

Lite Strategy@LiteStrategy

Clearstream added Litecoin to regulated institutional custody this month. It is one of two international central securities depositories globally, the post-trade settlement layer under Deutsche Börse, holding over 15 trillion euros in assets. $LTC now settles through that system via @CryptoFinanceAG, the MiCAR-licensed sub custodian in the group, which means institutions custody it inside their existing account with no separate crypto counterparty. Settlement access is the unglamorous gate every allocation passes through, and Litecoin is now on the right side of it. Payments. Privacy. Hard money.

English