@athuinvests Is there any reason for the general tech drop off today? Seems a great second chance to get into TRT for those (like me) who missed the opportunity yesterday

English

Cryptotron38

219 posts

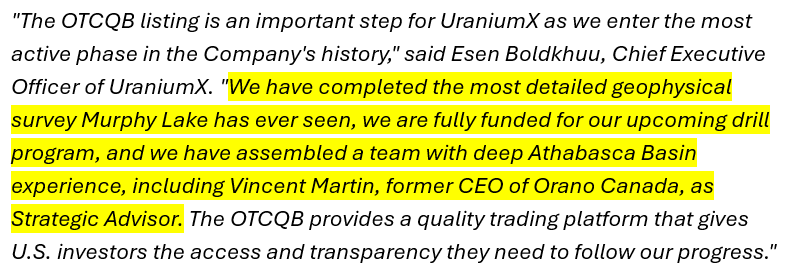

🚨 Buy Alert Today I initiated a position in $TRT (5% of my portfolio at ~$14). HELLO $TRT: Trio-Tech International is a U.S.-listed company providing essential back-end semiconductor testing and burn-in services. Its operations are primarily centered in Asia, with the largest revenue-generating hub and testing facilities in Malaysia. After chips (AI GPUs, HBM memory stacks, high-performance CPUs, or power semiconductors) are packaged, they require rigorous stress testing, reliability screening, and quality validation before shipping. $TRT delivers exactly that - the final critical quality gate. With AI demand surging, supply of reliable testing capacity is struggling to keep up. Customers simply cannot afford to ship faulty chips into data centers or vehicles, making this step non-negotiable. While $AEHR focuses on wafer-level testing, $TRT serves as the complementary “last mile” quality assurance provider. TIER-1 RELATIONS & POSITION: > Booked Tier-1 Orders: ~$7.8M in burn-in board orders for a next-generation AI GPU platform (possibly $AMD). Additionally, they secured a ~$2.5M order from a leading automotive IDM. > Malaysia Advantage: Penang handles roughly 13% of global chip assembly and testing. $TRT’s aggressive expansion (new 104k sq ft facility) positions it perfectly to capture more Tier-1 orders and reduce customer concentration risk. > Broader Applicability: Critical for HBM stacks, AI GPUs/CPUs, photonics/CPO (co-packaged optics), and SiC/GaN power devices. Back-end testing is a structural bottleneck in high-power AI hardware - a point even Michael Dell has highlighted. > Competitive Edge: $TRT doesn’t have $AEHR’s deep moat, nor does it directly compete head-on with giants like ASE or KYEC right now. Those larger players are already capacity-constrained on flagship work. $TRT is ready and scaling into niches they deprioritize. Its diversified footprint (Malaysia, Singapore, Thailand, US, China) also offers a premium for Western fabless and IDM customers seeking supply chain diversification away from Taiwan/China concentration. VALUATION & GROWTH: - Market Cap: ~$140M - TTM Revenue: ~$58M - P/S Ratio: ~2.3x Recent revenue has been accelerating hard: - Q1 FY2026: +58% YoY - Q2 FY2026: +82% YoY - Q3 FY2026: $16.5M (+124% YoY) Gross margins sit around 16-25%, reflecting a competitive services business. However, I still feel this kind of valuation at triple-digit growth won’t last. The balance sheet is clean: ~$16M cash and very low debt (~0.1 debt-to-equity). PRICE TARGETS: At full capacity (~$190M+ for total potential - calculated by @kishwarAI), and 5x P/S, I would expect 5-7X from today's ~$140M valuation. - EOY'26 - $60-$70 - EOY'27 - $100 If the street decides to price this higher, considering the revenue growth, demand > supply & full capacity utilisation (and more expansion) with more Tier-1 orders, we could see the stock hitting $120-$140 kind of levels. That is the BULL case. HOW I WILL PLAY THIS: 5% of my portfolio today consists of $TRT at a $14 average. As the story plays out through revenue growth & orders, I plan to keep BUYING dips. RISKS: > Key customer concentration: Malaysia footprint & high-demand will bring more orders. > Margin compression & dilution: Dilution looks strategic for capacity expansion and margin compression seems temporary due to their aggressive, forward-looking AI expansion phase. > Execution: Revenue growth & capacity expansion (including $10M raise) has given me confidence in their ability to execute. Balance sheet is clean. TLDR: We got real AI tailwinds with demand, booked orders from Tier-1 customers, capacity buildout, triple-digit revenue growth, geographic edge, undervaluation, and a clean balance sheet which means financial discipline. Really hard to ignore this! I am in.