@brandon Let's go! What's happening with Synapse and Evolve? (nothing good) Is having the ex-FDIC Chair involved a signal of something greater? (not really) What can we expect for fintechs in general? (come and see!)

English

Chris Dean

1K posts

@ctdean

CEO and Co-founder of @treasuryprime. Our banking software, network of banks, and technology partners power enterprise-class embedded banking solutions.

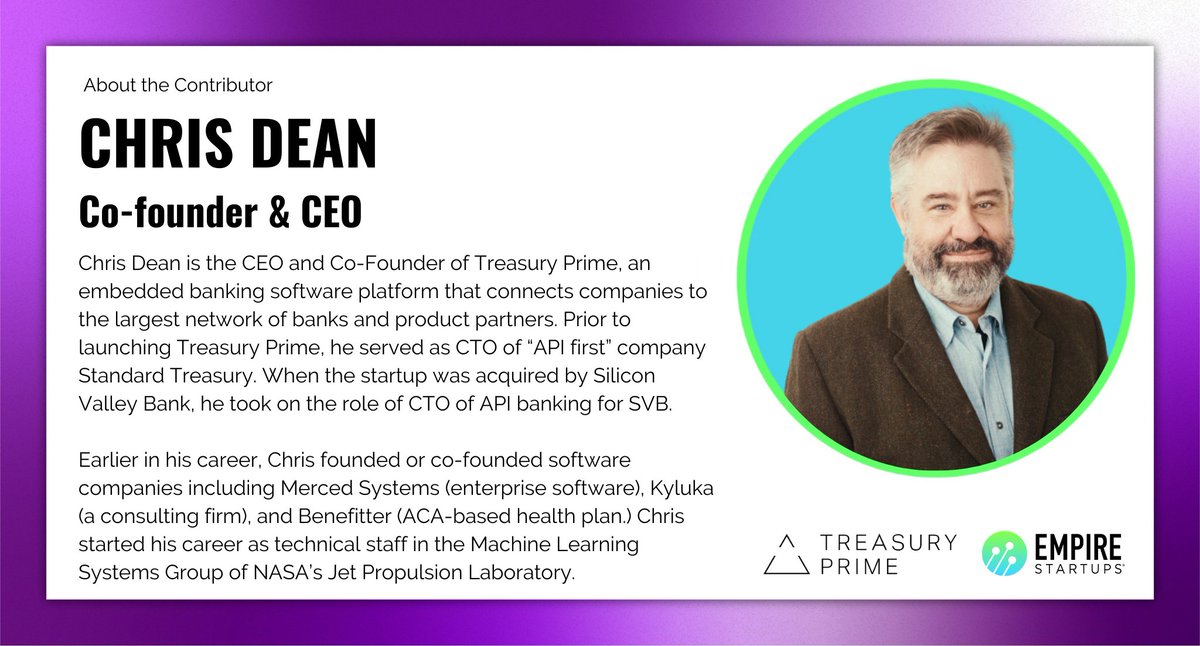

Read the latest edition of @EmpireStartups FinTech Newsletter for more of Chris’s insights on how fintech startups can grow quickly and safely: empirestartups.substack.com/p/how-fintech-… #Fintech #FraudPrevention #StartupEcosystem

I’m thrilled to share Cable has raised an $11M Series A! I wrote a blog post explaining how we’ll be using this funding and what this means for Cable going forward. We’re already hard at work building even faster and reaching more customers. community.cable.tech/weve-raised-an…

1/ Cross River is making time to chat with clients on the consent order. I joined one such call and my tl;dr is they're doing a good job managing the normal give-and-take that happens in this space. If I'm a fintech founder, I'd be excited to keep working with them.