Emil

10.4K posts

Emil

@cuzmane

Equities / Options trader. In the business since 2000 | Tweets are for entertainment and def. not investment advice

Katılım Mayıs 2012

304 Takip Edilen15.9K Takipçiler

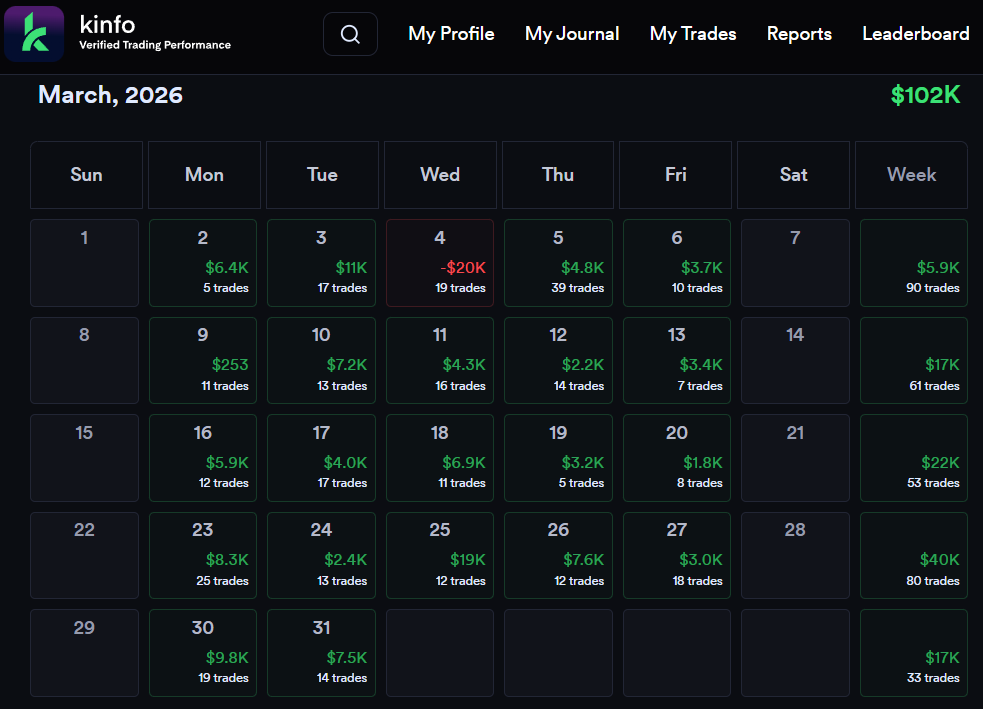

Resultados VERIFICADOS @kinfo Marzo2026 - $102K

1- Hay erosión de Edge? Si. A medida q más gente hace las mismas cosas, se hace más dificil aplicar los mismos patrones que uso hace 10 años. Cuando digo "más dificil" es q tienes q adaptarte. Adaptarse es: Perder dinero para entender que tienes que ajustar tu trading: ejm Ir por recorridos mas cortos en gappers que antes querias fade D1. Ir con size mas pequeño para ser más flexible en tu convicción del patrón (ejm con reversiones). Pasar de no tradear chinas a irles long... o a solo ir short en cosas q tengan liquidez extrema como WNW., etc

Adaptarse tiene que ver con HABILIDAD. A lo mejor en algun momento, mi adaptación será salir de Small Caps. Quien no se adapte, sea como sea, quien no cambie, quien no evolucione, esta MUERTO!

La habilidad del trader esta en:

* tener tolerancia al riesgo alta

* tener fortaleza para aguantar drawdowns

* Observación y mente abierta para potenciales nuevos edges, aprenderlos y hacer cosas que quizas no estes tan comodo.

* Asumir que estas EQUIVOCADO y tener la humildad de reconcerlo

* Ser contrarian en muchas ocasiones

* "Olfatear" oportunidad y reconocer ciclos de mercado.

* Reconocer en qué eres bueno y qué amerita incrementos de size y riesgo.

* Tener paciencia para esperar TUS setups y tomar tus profits.

* Cuestionar tus habilidades TODO el tiempo para ser mejor día a día, pero aún asi tener CONFIANZA en ellas

* Entender que TODA la responsabilidad recae sobre TI y no en el mercado, broker, Trump, etc.

2- Small caps esta muerto? No, pues hay volatilidad y liquidez. Para referencia: En 2022 hasta 31Marzo habian 28 gappers de más de 50% y el gap promedio d estos fue de 86%. En 2026 ha habido 145 y el gap promedio 101%.

Siempre que haya volatilidad y liquidez, va a haber oportunidad.

Por último... Tengo 6 años publicando resultados TODOS los meses. Están verificados y son reales. No voy a parar porque a ti te de genere incomodidad ver a gente que le esta yendo mejor que a ti. Si tienes esa actitud, probablemente te alegraste d ver mi Enero negativo... pero de qué te sirvio? Eres mejor por eso? Porque yo si soy mejor gracias a mi Enero negativo. Usa esa incomodidad para ser mejor y no para odiar y reventar a otros.

Transparencia para generar Roger Bannister effect (q por algo tu timeline de twitter (X) esta lleno de traders en español... de nada), pero TAMBIÉN para tener autoridad y legitimidad desde mi espacio y transmitir lo DIFICIL, pero lo hermoso que es el trading como profesión.

PD: ¿No es una bocanada de aire fresco leer un post que no sea formato de AI?... Estoy LADILLADO de ese tipo de POSTS.

Español

Emil retweetledi

Morning Broadcast - Watchlist Prep - $SPY $BTC $QQQ $MRVL $FRO $DHT $INSW x.com/i/broadcasts/1…

English

📋 Watchlist for 03/30/26

Mixed setups heading into Monday — watching for bounce potential on $MSFT (355 support) and $META (520 level), while leaning short bias on $SNDK, $INTC, $AXTI, and $ASTS. Eyes also on $AMD and $AAPL both hovering around their 200SMA — key level to hold or lose. Let's see how it plays out 👀

investorsunderground.com/s/gEXHc

English

Emil retweetledi

Morning Broadcast - Watchlist Prep - $SPY $BTC $QQQ $NVDA $SEI $GEV x.com/i/broadcasts/1…

English

@SteveDJacobs @RealSimpleAriel Great lesson Steve that's a really dif approach, thanks

English

Backtesting Analysis With Claude - * Livestream *

I had the honor and pleasure of an impromptu* discussion with the ever excellent @RealSimpleAriel on my recent systematic algorithm backtesting and using Claude to perform the analysis.

Below is a link for anyone interested:

youtu.be/Q64pDDAlYEE?si…

Thanks to @RealSimpleAriel & @NickDrendel for running the BEST swing trading stream every market day. There is no better place to learn to trade than here (link below).

t.co/0Nm1cXpHv3

Special shout out to Stephen for kindly recording the chat - please give him a like, subscribe and comment for all his efforts. 🤝💙

PS. Apologies if I sound sleepy or unprepared (it was 2am and I was heading off to bed 😴)

YouTube

Steve Jacobs@SteveDJacobs

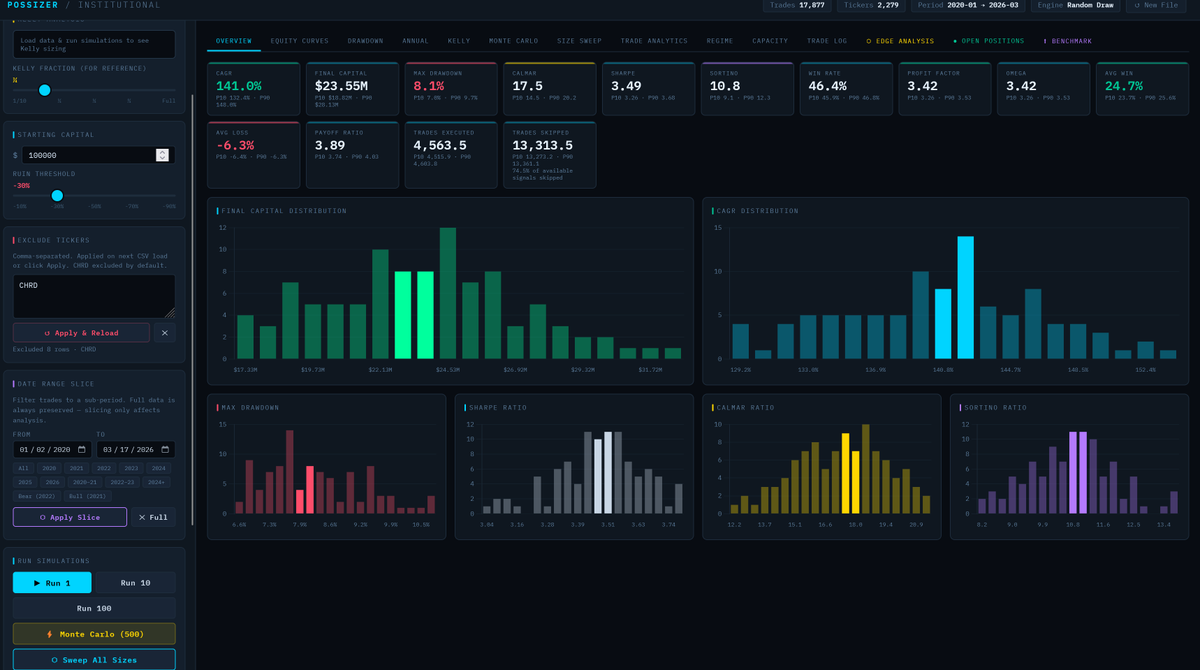

📈Stock Allocation - When Scaling-In Beats "Going Big" Recently I've been working on a systematic algorithm* backtested over 6.2 years (2020 to now) across stocks with a current market cap of $1B+ The backtest generated over 18,000 trade signals with an average return of 11.95% per trade. The question was "what allocation % per trade yields the best results?" It turned out 1–2% was the optimum. 1% produced a CAGR of 64.9% — worst year 2022 (+8.6%), best year 2025 (+100.6%). Max drawdown was 5.9% with a Sharpe of 1.76. $100,000 became $2,189,300. Win Rate: ~49–54% Avg Win: ~+25% Avg Loss: ~−6.2% Avg hold: 23.2 days 23 trades returned +500%+. Several exceeded +1,000%. Why does small sizing win? At 10% (10 slots), the sim skips most trades. At 1–2% (50–100 slots), you're actually there when the big ones hit. Admittedly this is WIP — there may be errors in the data. The large winners have been verified manually and with AI, and the raw trade data has been shared with colleagues for peer review. Next step: run it live with real capital through the rest of 2026 and track out-of-sample results. * Algorithm is written and executed in Python. The resulting trades are fed into Claude Pro (Sonnet 4.6) to run Monte-Carlo simulations, walk-forward portfolio analysis etc.

English

Weekend scan for the weak ahead

Market exposure stays light. Nasdaq broke below the 200-day, VIX is elevated,Energy and memory sectors are leading. Not much works in this tape, but the few names holding above their moving averages deserve attention.

investorsunderground.com/s/9eXng

$SNDK $MU $STX $DELL $OXY $DVN + quantum

English

Announcing Personal Computer.

Personal Computer is an always on, local merge with Perplexity Computer that works for you 24/7.

It's personal, secure, and works across your files, apps, and sessions through a continuously running Mac mini.

English

Anyone who traded through 2008, the Flash Crash, or the pandemic isn't going to roll over and die because of some geopolitical noise that’ll be quickly priced in.

Stay liquid, stay calm, and stop trading like it’s your first day! 📉 $SPY $QQQ

English

With tensions escalating due to the Iran conflict, I’m keeping today’s watchlist strictly price‑action focused and flexible. The market will likely gap down in the overnight session, so this is not a directional call—just levels and setups I’m watching, ready to adapt if volatility picks up.

investorsunderground.com/s/ix5c5

$AA $FCX $XLV $LLY $XOM $SLB $SNDK $CLS $AMD

English

Looking to short these names today AMD IREN AVGO CLS , focusing on weakness into pops and clearly defined levels, with a strict risk-first approach and quick adjustments if price action proves the idea wrong.

investorsunderground.com/s/ub3uV

English