darwintIQ

32 posts

darwintIQ

@darwintIQ

Real-time ranking of adaptive trading models. Trend & structure analytics via API. Built for systematic traders. https://t.co/jBeNnTxLdZ

Worldwide Katılım Şubat 2026

48 Takip Edilen1 Takipçiler

Here is how you would get a Quant based Market Briefing via the API in Python yourself:

github.com/darwintIQ/API/…

#quantitativeTrading #quantAnalysis #python

English

Short term Market Briefing for DAX, done by our AI Quant analyst "Charlie". Check it out: darwintiq.com/articles/marke…

#dax #marketBriefing #quantitative #trading

English

Charlie by darwintIQ: The quant analyst you can actually ask producthunt.com/products/charl… by @darwintIQ

English

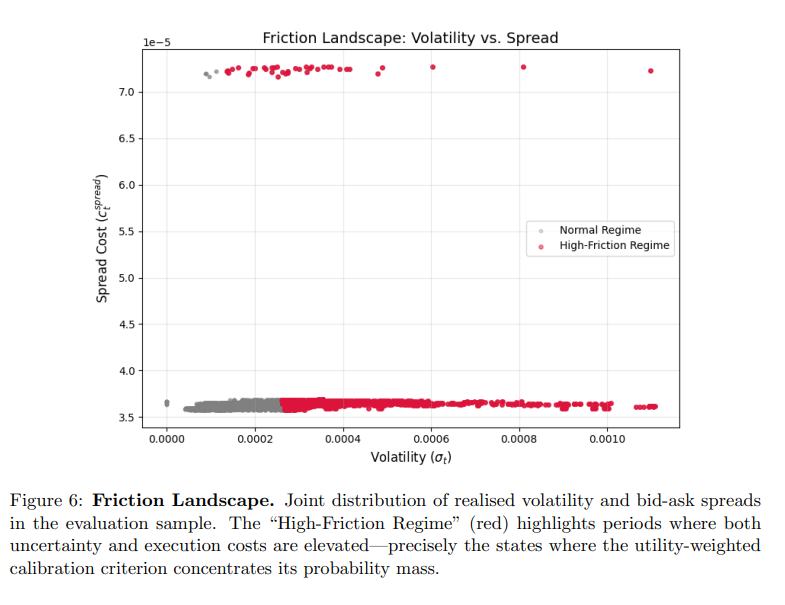

If you’re building or evaluating trading models,

understanding regime change is critical.

Full breakdown:

darwintiq.com/articles/regim…

English

Profit alone says very little about a trading model.

Two strategies can earn the same returns — but behave completely differently.

The Sharpe Ratio helps reveal that difference.

Read more: darwintiq.com/articles/what-…

English

Monte Carlo bots everywhere

most traders don't get why randomness beats math

> This 8-min visual lecture gives the missing piece everyone needs

Problems like stock market:

paths explode to billions of possibilities

analytical solution impossible, cuz integrals too hard to solve

Monte Carlo fixes it by sampling random paths, then averaging expectations

Law of large numbers guarantees convergence to true value with enough samples

Grids fail with exponential cost per added dimension,

Monte Carlo error only depends on sample count

Watch this, it builds the intuition everyone's missing

and apply these insights to your trading

English

Most trading strategies look great in backtests.

But markets drift.

That’s why strategies decay.

I made a short video explaining the idea:

youtube.com/watch?v=UXqjVq…

YouTube

English

Profit alone doesn't tell you if a trading model is good.

Two models can make the same money — while behaving completely differently.

One is stable.

One is fragile.

That’s why Fitness metrics matter.

Learn more:

darwintiq.com/articles/fitne…

English

@Quantocracy @JonathanKinlay Very interesting article. Thank you for posting it.

English

darwintIQ retweetledi

Reinforcement Learning for Portfolio Optimization: From Theory to Implementation [@JonathanKinlay] dlvr.it/TRMzgM

English

How does Jensen–Shannon Divergence influence model fitness in darwintIQ? Learn how it affects adaptive model ranking. darwintiq.com/articles/jense… #quant #algotrading

English

@gemchange_ltd @alvinjamur Amazing work! Thanks.

Would love to read more from you.

English

darwintIQ retweetledi

I admit that the "improves the Sharpe ratio from -3.62 to -2.29" thing caught my attention haha thankfully I then read "during a drawdown regime"

English