乐活乐着

576 posts

亚历克斯这波 台北 101 真的真的只是表演秀,😓,他的大脑异于常人,对于这样的高峰只有兴奋没有恐惧。

他真正经典和第一波出圈是徒手攀岩 900 米高的酋长岩(纪录片拿了奥斯卡奖),101 才 500 米而且还是人造物。

希望商业世界能更多的关注这样真正极限挑战运动员,感谢 tradingview ,Netflix 。

小牛@Xiaoniu6161

亚历克斯·霍诺尔德完成台北101大楼的徒手攀登后说:“太棒了!” 攀登这座101层楼耗时1小时35分钟。 这简直成了他的表演舞台了,太优秀了。 希望奈飞公司能梗多也会创收。

中文

乐活乐着 retweetledi

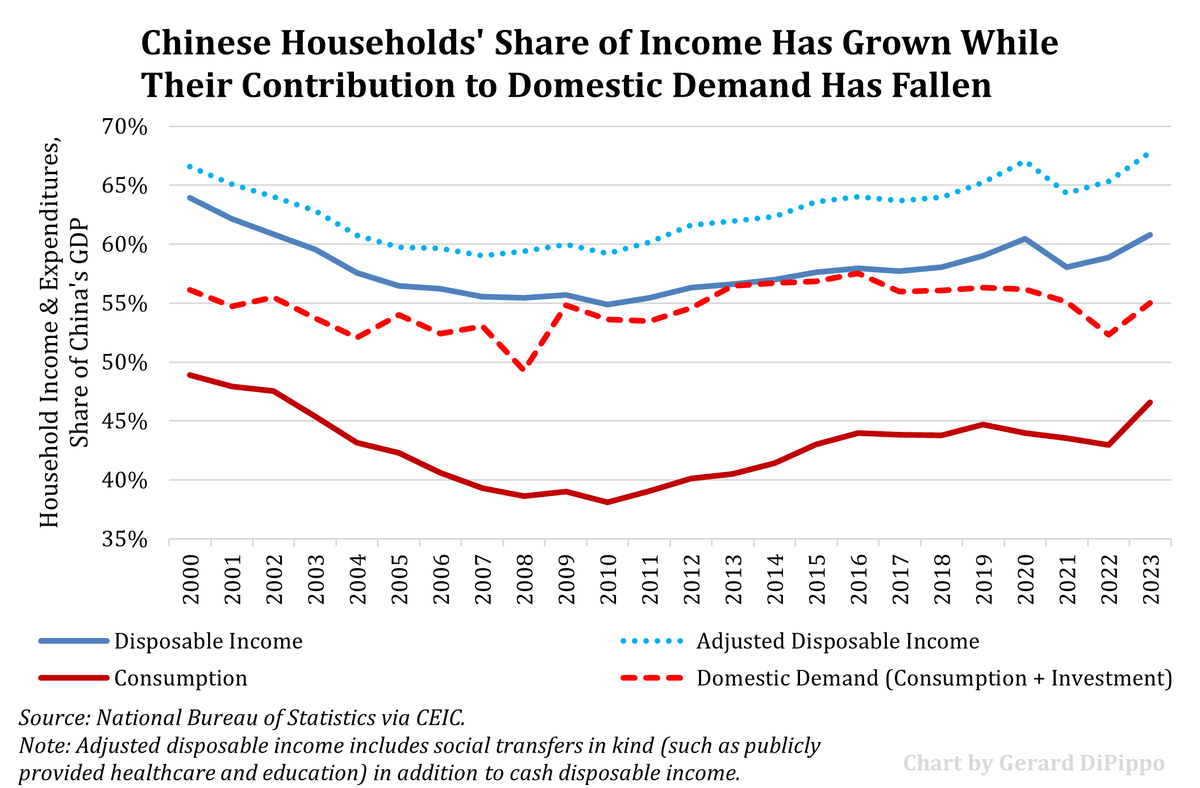

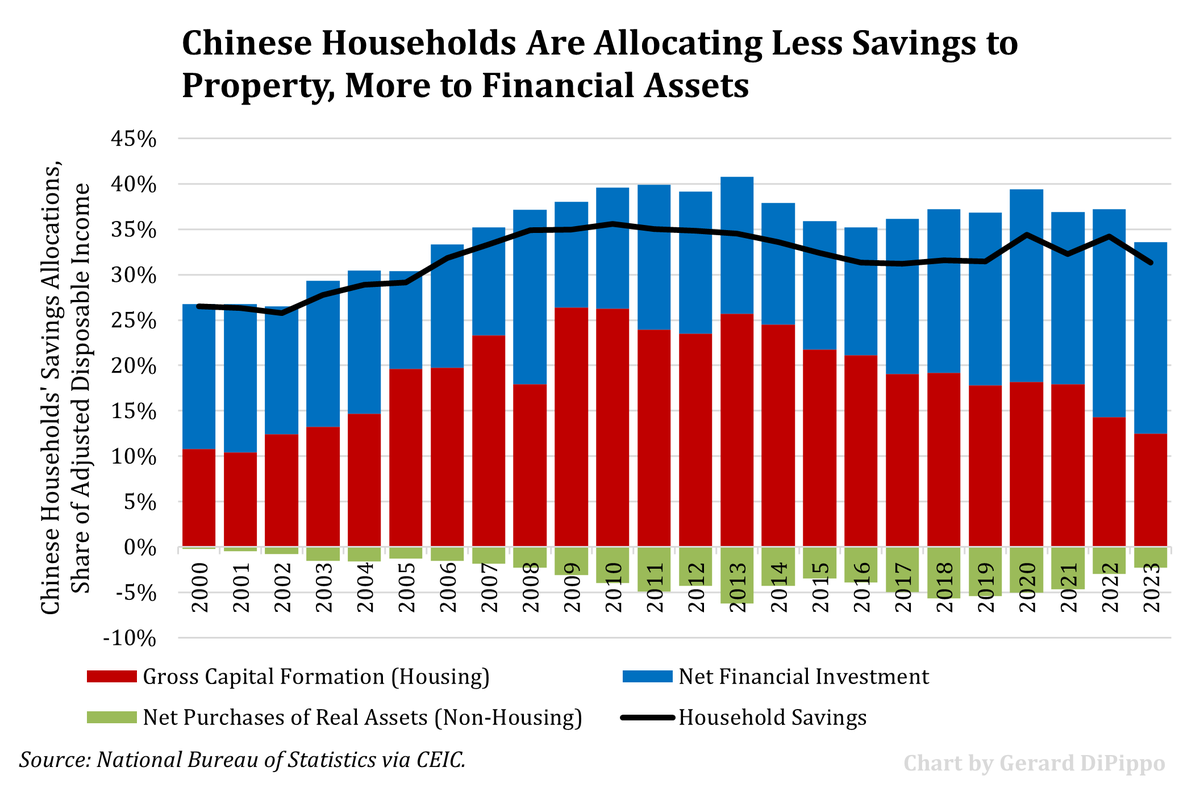

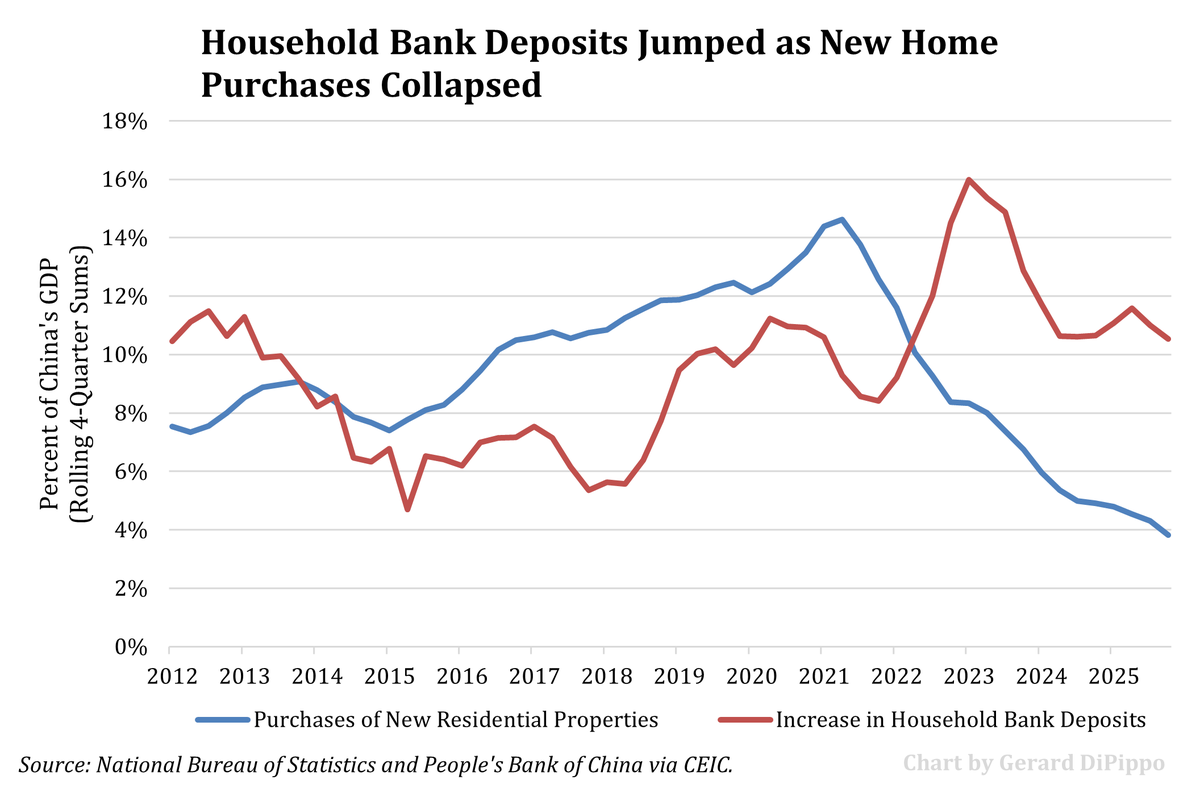

China’s “consumption problem” is often misunderstood, and the property sector is the missing link. It’s true, in accounting terms, that household consumption is low as a share of China’s GDP. But a common mistake is to equate “high household savings” with idle money sitting in a bank account. That’s not how China’s national accounts work.

Looking at China’s Flow of Funds data, it’s clear that household savings are not just financial savings. For much of the past two decades, savings were overwhelmingly allocated to “gross capital formation,” primarily purchases of new housing and related investment. From 2012–21, household capital formation (property) accounted for about 64% of household savings on average. Those “savings” were generating domestic demand through construction activity, upstream industrial demand, employment, and local government revenues. High savings do not necessarily mean weak demand.

That changed after China’s property downturn. As new home purchases collapsed, households shifted savings away from housing investment toward net financial assets (first bank deposits and, more recently, equities). That portfolio shift may be rational for households, but it does not directly create real economic activity in the way housing investment once did.

This helps explain why China’s domestic demand challenge is harder than it sounds. It’s not just about getting households to consume more or save less. It’s about how to replace a massive housing-investment demand engine. Households can only buy so many new goods, absent the need to stock new homes.

One consequence is that household consumption growth is tilting toward services. I estimate that services accounted for roughly 60% of nominal consumption growth in 2023–25. That supports incomes and employment, but it generates relatively less demand for manufactured goods.

Thus, one key tension with the upcoming 15th Five-Year Plan is its top goal of “building a modern industrial system.” From a demand perspective, the old engine is gone, and the new one looks very different.

Bottom line: when thinking about China’s “consumption problem,” think about the property sector and how to fill that giant hole in domestic demand. It’s not obvious how Beijing does that quickly.

English

乐活乐着 retweetledi

China is a manufacturing powerhouse, yet it has low productivity per traditional analysis.

But when you look at actual physical output per worker, China’s labor productivity is far higher than traditional estimates.

Outstanding piece by Weijian Shan: research.gavekal.com/article/unrave…

Louis-Vincent Gave@gave_vincent

We just published a terrific guest piece from my friend Weijian Shan. I think it is a must read for anyone looking to understand China’s advances in manufacturing. research.gavekal.com/article/unrave… The piece has no firewall and is open to everyone. Incidentally, Weijian Shan wrote one of my favourite books; a book I had all four of my kids read. The book, OUT OF THE GOBI, details his growing up at the time of the cultural revolution. Hard to understand China today without understanding what the current generation of leaders went through in the late 1960s/early 1970s… Please forward widely!

English

企业家最重要的是性格和敏锐的商智,这俩都是天生的,不是学校能培养出来的,是天生,父母,社会和自己合力的激荡。很多出入最高级写字楼的高级打工仔,年薪几百万美元,都不具有企业家的能力,他们可以在一个已经形成的逻辑里把它变大,但创业是另外一回事,创业的话,很多这些成功的人都会失败。

麻黑 Clouds Gray@naitgray

企业家是人才,真的。一个企业家,对应很多税收和就业,特别是就业。一辈子打工的人不会懂创业多难。

中文

乐活乐着 retweetledi

若是有一天,你非常倒霉的和一头猪掉入泥潭,你能做的就是赶紧上岸,而不是在泥潭里跟猪打架。

——查理·芒格

中文

乐活乐着 retweetledi

这个世界上真正值得把握的机会只有那么几次,并且这样的机会只有精心准备的人才能抓到。他是极好的运气与不停努力的产物。

它什么时候来,没人知道。它来的时候可能你正在吃饭,也可能在睡觉,还有可能在做别的事情。为了抓住这样的机遇,我们能做的就是一动不动地盯着那件事,死死地盯着,全身心地投入,直到他完成。但也有可能有些人专注了一辈子,结果那个机会从未到来。

这就是为什么我们要敬天爱人。敬的是那个提摸不定的规律,爱的是那些人付出的心血与执着。成功的人一定有其过人之处,但那些不断失败还努力一辈子的人更值得我们尊重。人生,就是这样,即便没有那种机会,也要认真地活着,做好每一件事,这样即便没有那样的机会,也能活得更加充实与杰出。

中文

乐活乐着 retweetledi

这两天有两条重要的“知情人士”爆料,

一是,给使用国产芯片的企业电力补贴;

二是,对接受政府资助的数据中心要求必须使用国产芯片。

路透评价这是推进国产化的“激进措施之一”,

这才哪到哪,

我此前写十五五前瞻时,用了八个字形容十五五的主线:

“大炼科技、产业跃进”

很快还会有更多、更激进的举措,

什么“超前布局”、“超常规”、“攻坚战”,这些激进的政策用词,不是说着玩的,背后是巨大的政策资源,以及政治决心

中文

乐活乐着 retweetledi

乐活乐着 retweetledi

当巴菲特囤3817亿美元现金时,他看到了什么?

他看到的不是泡沫,而是一场没人敢输的游戏。

一、两个极端的现实

一边是全球最激进的AI公司在用未来的钱下注,另一边是全球最成功的投资者在用现在的钱观望。

2025年11月1日,伯克希尔·哈撒韦公布三季度财报:现金储备3817亿美元,创美国企业史上最高纪录。这已是巴菲特连续第九个月零回购,单季度净卖出股票104亿美元。

就在同一周,华尔街日报披露:OpenAI与Oracle签署价值3000亿美元的五年云计算合同——相当于承诺每年支出600亿美元。而OpenAI 2025年预计全年收入仅130亿美元。

这两个场景放在一起看,会让人不寒而栗。

更要命的是,基于微软持股约32.5%,华尔街分析师反推出OpenAI第三季度亏损超过120亿美元。

每收入1美元,亏损3.3美元。

但甲骨文联合创始人Larry Ellison还是给了它3000亿美元的合同,一天之内个人财富增加1000亿美元。

这不是泡沫故事。

当游戏规则改变时,最聪明的人选择退出游戏。

二、OpenAI的创新

OpenAI的创新的不是GPT,不是Sora,不是8亿周活用户。

它真正的创新,是发明了一种新的商业模式:亏损本身就是护城河。

逻辑链条非常简单:

第一层:当你季度亏损120亿美元时,没有竞争对手能跟进。这比任何专利、任何技术壁垒都更有效。

第二层:当你的亏损规模达到3000亿美元级别时,你变成了"系统性重要企业"。Oracle不能让你倒,微软不能让你倒,整个AI生态都不能让你倒。

第三层:当你"大而不能倒"时,你就获得了无限续命的能力。3000亿美元合同不是因为你盈利了,而是因为你不能倒。

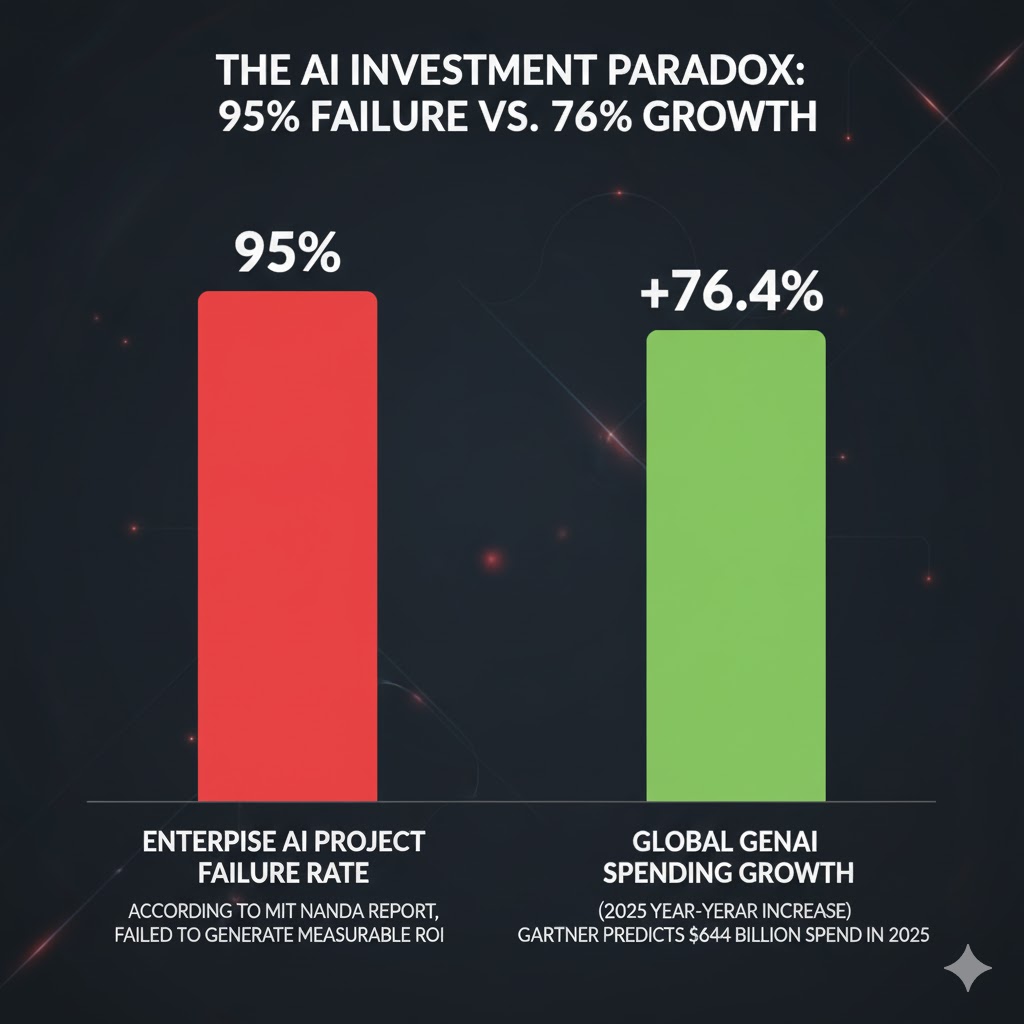

这就是为什么MIT报告显示95%的企业AI项目失败、300-400亿美元打水漂,但投资还在以76%的速度疯狂增长。

不是因为相信一定成功,而是因为不能承受失败的代价。

这不是价值投资。这是叙事投资的终极形态。

三、这次不一样:为什么AI泡沫比2000更危险

很多人把今天的AI基建类比成2000年的互联网光纤泡沫。

它们确实有相似之处——在应用层出现killer app大范围盈利之前,就投入巨资建设基础设施。当时是光纤,现在是数据中心。

但这次有四个致命的不同,既让AI泡沫比2000更危险,也让其更难破裂。

不同1:硬件集中度极高

2000年,光纤制造技术含量不高,全球有几十家供应商。但2025年,先进AI芯片全世界只有那么几家公司能做——Nvidia的GB300以及下一代AI芯片,已处于相对垄断。

泡沫的收益高度集中在极少数公司。Nvidia市值5万亿美元,占S&P 500约8%,创1981年以来单一股票最高占比。PE比57倍,是半导体行业均值的3倍。

但这也意味着:泡沫破裂的条件更高。因为只要Nvidia盈利能力不出问题,这个泡沫就很难破。事实上,2022年矿难时Nvidia利润率只是从65%回撤到56%,算上PE/宏观双杀股价才从300跌到100。

不同2:泡沫扩散到能源领域

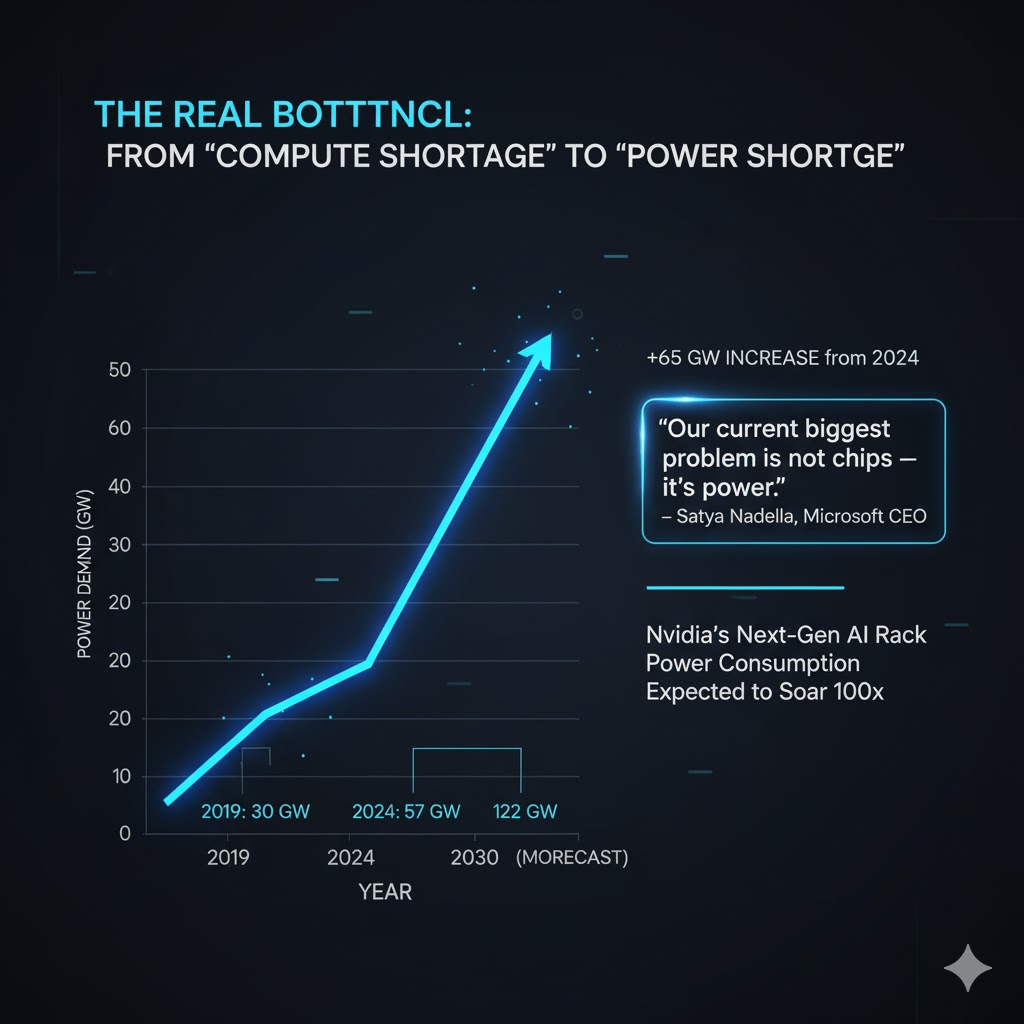

2000年,光纤就是光纤。但2025年,数据中心不仅需要GPU,还需要电能。

微软CEO纳德拉最近在播客里分享了一个让人意想不到的事实:

"微软手里囤了一堆英伟达AI芯片,但压根没法用。不是因为芯片不够,而是数据中心的供电和物理空间已接近极限,导致大量AI芯片只能滞留在库存中,无法'通电运行'。"

更夸张的是,英伟达每一代机架系统的功耗都在暴涨:从安培架构到下一代Kyber设计,单机架热设计功耗预计将激增100倍。

100倍意味着什么?意味着数据中心的电网、冷却系统、物理空间全得重新规划。

之前AI行业担心"算力荒",现在还要加上"电力荒"。这让泡沫连带扩散到了能源、电网、核电——比2000年涉及的领域广得多。

Goldman Sachs估算,全球数据中心电力需求将从2019年的30GW增长到2024年的57GW,到2030年需要再增加65GW。仅美国就需要新增约38GW,相当于38座核电站。

不同3:软件集中度也极高

2000年互联网泡沫催生了无数没有营收的.com公司,几千家公司拿到融资,最后死掉几千家。

但2025年的AI泡沫紧紧围绕在OpenAI、Anthropic、Google等为代表的模型公司周围,软件集中度特别高。

这意味着:泡沫破裂时影响的公司数量会少得多。不会像2000年那样,几千家互联网公司一起倒下。

但这也同时意味着:只要这三家不倒,叙事就不会崩塌。而OpenAI已经证明了"Too Big To Die"的逻辑——3000亿美元合同就是护身符。

不同4:NeoCloud模式转移了风险

数据中心投资特别大,周期特别长。为了避免账面债务甚至以后的烂尾风险,大科技公司逐渐把建设数据中心的任务外包给第三方——也就是NeoCloud。

这在2000年互联网泡沫中是没有出现过的。

NeoCloud作为退潮时受冲击最早也是最大的群体,也会是涨潮时受益最丰厚的群体。举债太多的NeoCloud可能会有危险,但大科技公司的资产负债表保持干净。

这种风险转移机制,让大科技公司可以继续保持"健康"的财报,进而让泡沫持续更久。

四、为什么这个泡沫还能继续?

因为需求实在太大了。

目前所有云的积压订单backlog堆到天上去了,造成下游厂商看到的订单全都是off-the-chart。从CSP、芯片、NeoCloud到存储、到电力,所有财报几乎全都是同一句台词且能交叉验证:

"挤压的订单太多,根本做不完。加上新增的订单,2028年都消化不完。"

这和2000年光纤泡沫有本质区别:

2000年光纤基建是提前预测需求,过度建设

2025年GPU基建是GPU utilization已经拉满还不够用,必须疯狂推动下游订单

Jensen Huang 10月29日说:"我们对2025-2026年Blackwell和Rubin产品有5000亿美元的累积收入可见性。"

不是合同,不是订单,是"可见性"。但市场信了。

因为市场已经不在乎现金流,市场在乎的是你在叙事中的位置。

只能谨慎乐观地说:we are still early。

五、风险在哪里?

风险在于当技术跃迁发生时,所有这些基础设施都可能一夜过剩。

1996-2000年,电信公司疯狂铺设光纤,累计投资超过万亿美元。叙事很简单:互联网流量将呈指数级增长,光纤需求无限。

需求判断完全正确。

但1998年,WDM(波分复用)技术取得突破——单根光纤的容量增加了100倍。突然间,"光纤短缺"变成了"光纤过剩"。85-95%已铺设光纤永久闲置。

WorldCom、Global Crossing破产,股东损失超过2万亿美元。

光纤泡沫破裂不是因为需求错判,而是因为技术跃迁让旧基础设施过剩。

现在看AI,Nvidia自己也在投资:

Quantinuum(量子计算):6亿美元

PsiQuantum:10亿美元

2024年推出NVQLink:量子-GPU互联标准

量子计算不会"替代"GPU,但如果量子-AI混合让训练效率提升10-100倍,GPU需求可能骤降50-70%。

类似1998年的WDM:不是光纤没用了,而是需要的数量骤降90%。

这就是"光纤时刻",技术跃迁导致基础设施过剩。

如果3-5年内发生,当前4200亿美元年度资本开支中有多少会变成闲置产能?

回到开头的问题:巴菲特看到了什么?

他看到的不是泡沫,他看到的是游戏规则改变了。

1930年代,Benjamin Graham创立价值投资:内在价值、安全边际、市场非理性。90多年来,这套哲学经历了无数次考验,每一次泡沫破裂后都证明了自己。

但2025年,规则改变了:

亏损不再是风险,而是护城河(OpenAI模式)

估值不再基于现金流,而是基于叙事中的位置(Nvidia PE 57倍)

"大而不能倒"不再是银行的特权,而是科技公司的常态(3000亿美元合同)

当游戏规则改变时,巴菲特的做法不是适应新规则,而是退出游戏。

这就是3817亿美元现金的真正含义。

六、三种可能的结局

结局1:叙事赢了

AI真的是电力级革命,OpenAI最终盈利,Nvidia持续垄断。巴菲特又一次错过了科技革命。

但即使这种情况发生,也不意味着所有人都赢。因为这次泡沫的收益高度集中——只有Mag 7受益,其他几千家公司无关。

结局2:1998重演

技术跃迁(量子/新架构/算法革命),GPU需求骤降50-70%,4200亿资本开支变成闲置产能。

但和2000年不同:影响的公司会少得多,因为本来也就没有几家AI上市公司。举债太多的NeoCloud会死,但Nvidia、OpenAI这些核心资产可能只是估值回调,不会消失。

结局3:中长期混沌

AI既不快速崩盘,也不快速爆发。进入5-10年"边投资边试错"阶段。巴菲特继续持有现金,等待更确定的机会。

问题只有一个:你选择相信哪个现实?

是MIT经济学家Daron Acemoglu(2024诺贝尔奖得主)说的"AI仅影响5%的工作任务"?

还是Jensen Huang说的"5000亿美元收入可见性"?

我不知道答案。

但我知道,当巴菲特囤3817亿美元现金时,他看到的不是机会,而是一个他不再理解的世界。

而在一个你不再理解的世界里,最聪明的做法就是持有现金,直到世界重新变得可以理解。

他是在等待那些信奉“新游戏”的玩家被“旧规则”(物理、财务和盈利)的现实所摧毁。

他持有的3817亿美元现金,不是用来退出游戏的,而是用来在“叙事”最终破灭时,从那些破产的信徒手中,以他所理解的“价值”价格,买下那些幸存的、真正有价值的资产。

美股在基本面上的回调叙事也已经到位:缺电、缺数据中心。

纳德拉的那句话值得反复咀嚼:

"我们目前面临的最大问题不是算力过剩,而是电力短缺。如果你无法提供足够的电力,那么即使拥有大量芯片,也只能让它们闲置在仓库里。"

当芯片在仓库里等电力时,泡沫就开始出现裂痕了。

但也许,这只是下一轮更大叙事的开始:核电复兴、能源革命、量子飞跃。

只要叙事不死,游戏就会继续。

而巴菲特,已经做好了准备。

中文

乐活乐着 retweetledi

Trading Space for Time: The World’s Most Expensive Breakup

Since Trump’s presidency, the term “grand bargain” has frequently been used as a possible U.S.–China deal — a broad, mutually beneficial agreement built on sweeping compromises across multiple issues.

I don’t think either political system still believes such a thing is possible. Both now view the other as a sworn adversary in a larger strategic contest.

A more fitting concept is “trade space for time” (以空间换取时间) — a phrase born from China’s wartime playbook against Japan and later during the CCP–KMT conflict. It means a tactical retreat: temporarily yielding ground to regroup, reorganize, and prepare for a better strike later.

That’s likely the only pragmatic course. The two economies are too large to knock each other out with a single blow. Each needs time to adjust, reconfigure supply chains, secure resources, and reduce vulnerabilities.

The U.S. is racing to cut rare-earth deals worldwide; within a year or two, China’s chokehold will loosen. China, meanwhile, is working to strip out its own dependencies — in semiconductors, aviation, core technologies, and reliance on the American consumer market.

This isn’t grand bargain. It’s managed disengagement — a slow, deliberate unwinding of a forty-year marriage.

And like any long divorce, it won’t be clean, quick, or cheap. But once it starts, there’s no going back.

Desmond Shum@DesmondShum

US–China Are Divorcing. The Settlement Will Reshape Global Business. People get too caught up in the daily drama of the U.S.–China relationship — the tariffs, the summits, the “breakthroughs” that never last. The decoupling isn’t theoretical anymore — it’s operational. Supply chains are shifting, capital flows are splitting, and CEOs now talk more about resilience than efficiency. To me, this isn’t a lovers’ spat. It’s a divorce in progress. After forty years of marriage, they’ve decided they can’t stand each other. The lawyers are in, and the accountants are dividing the joint assets — supply chains, tech, capital, markets. A couple of beliefs of mine: 1.They’re not getting back together. This was a marriage of convenience and necessity — different values, systems, and goals. It worked for a while; now it doesn’t. 2.Divorce is messy. There’ll be drama, retaliation, and moments that look like reconciliation. But the ending’s already written. Most corporates have just woken up to the reality — and some still refuse to accept it (wink wink, Germans). They see the signs: tariffs, export bans, investment restrictions. Yet few are acting on them. Many still hope it’s just a rough patch. It isn’t. The real question now isn’t if the divorce happens — it’s how your business will live with it. •Where are your supply chains rooted, and can they survive custody battles? •How exposed are you to regulatory crossfire — export bans, data rules, sanctions? •Where will your capital come from when one side shuts its markets? •How do you position your brand when each camp demands loyalty? Inside boardrooms, the divorce is already shaping strategy. CFOs are running dual cost models — one for each camp. General Counsels are spending more time decoding export rules than drafting M&A term sheets. For many multinationals, geopolitics has become a permanent line item on the balance sheet. Every divorce creates winners and losers. Southeast Asia, India, and Mexico are taking order books once bound for China. Defense and rare earth companies are thriving. But firms that built their fortunes as the bridge between both sides now find that bridge burning from both ends. This is where scenario play becomes essential. The companies that thrive won’t be the ones reacting to headlines, but those rehearsing different futures — testing assumptions, mapping contingencies, and preparing to pivot before they’re forced to. The marriage is over. The paperwork’s ongoing. The settlement will reshape global business — and only those who’ve rehearsed the next act will still have a role in it.

English

乐活乐着 retweetledi

China’s Economic Misnomers — and the Commentators Who Still Talk Like the Bazooka Is Coming

1. The Myth of a “Bazooka” Real Estate Rescue

Commentators keep waiting for Beijing to unveil a massive rescue plan to save the property market. But the problem isn’t liquidity — it’s physics.

China has built enough apartments for three billion people in a country whose population is now shrinking. Roughly 90% of developers are effectively insolvent, and the market has been contracting by about 20% a year for four consecutive years. That’s not a cycle; that’s exhaustion. No “bazooka” policy can resurrect a sector that overshot demographic reality by a generation — and policymakers know it.

2. The Fantasy of a Demand-Side Revival

The next popular refrain: if only Beijing launched a huge stimulus, domestic demand would roar back. But demand isn’t being held back by policy hesitation — it’s being held back by poverty.

An estimated 600 million Chinese earn less than RMB 1,000 (USD 160) a month, and 900 million earn under RMB 3,000 (USD 500). Pension and social-security coverage remain minimal. You can’t stimulate spending in a population that simply doesn’t have disposable income — especially when about 70% of household wealth is tied up in property that’s steadily losing value.

More importantly, China’s global competitiveness still relies on a vast, low-income, low-benefit workforce. Raising wages and benefits at scale would undercut that advantage, which is why Beijing has limited incentive to fundamentally rebalance the distribution of income.

So when analysts say, “if only Beijing recognized the problem and fired a bazooka stimulus, growth would rebound,” they’re misreading the model. The issue isn’t the absence of the right policy lever — it’s that the structure itself no longer supports the old playbook.

English

乐活乐着 retweetledi