danny williamson retweetledi

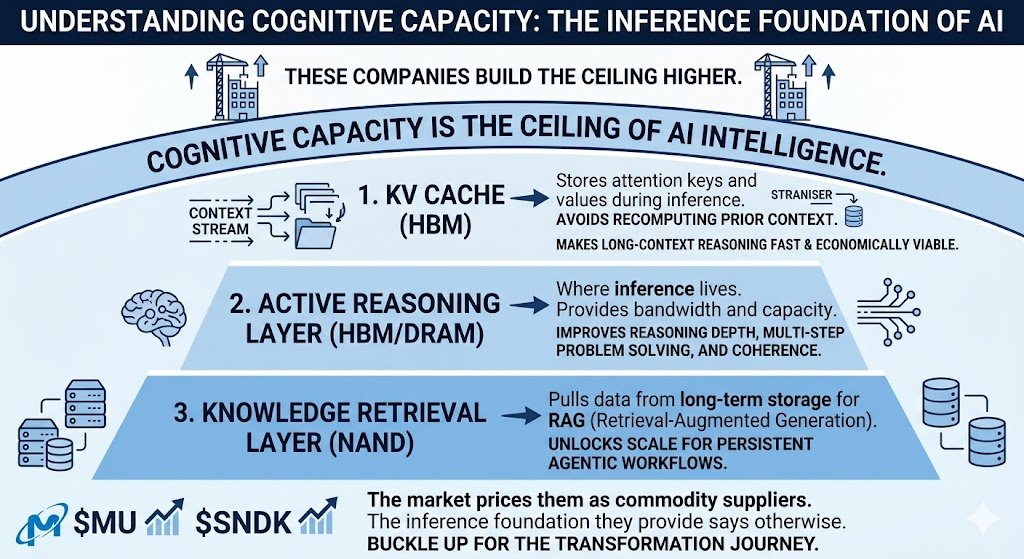

Today's AI is the least capable version you will ever interact with, running on the least amount of HBM it will ever be equipped with.

The trajectory from here has only one direction.

$MU $DRAM $SNDK

English

danny williamson

87 posts

This $EWY trade was stupid good. If you are an investor or trader on X, you simply must be following @aleabitoreddit . He understands macro, micro/company-level, and derivatives technicals, then puts it all together for you in one easily understandable package. A tremendous amount to learn from him.

This is my current portfolio As I said, I wouldn't sell any positions And I’ve kept my word, the money for the new position in $PENG does not come from my existing investments At the moment, I don’t see better opportunities in the market than what is already in my portfolio At least not at these prices I have on my radar things like $KOPN $DGXX $SOI etc

Who wants to go out in Japan tonight on me

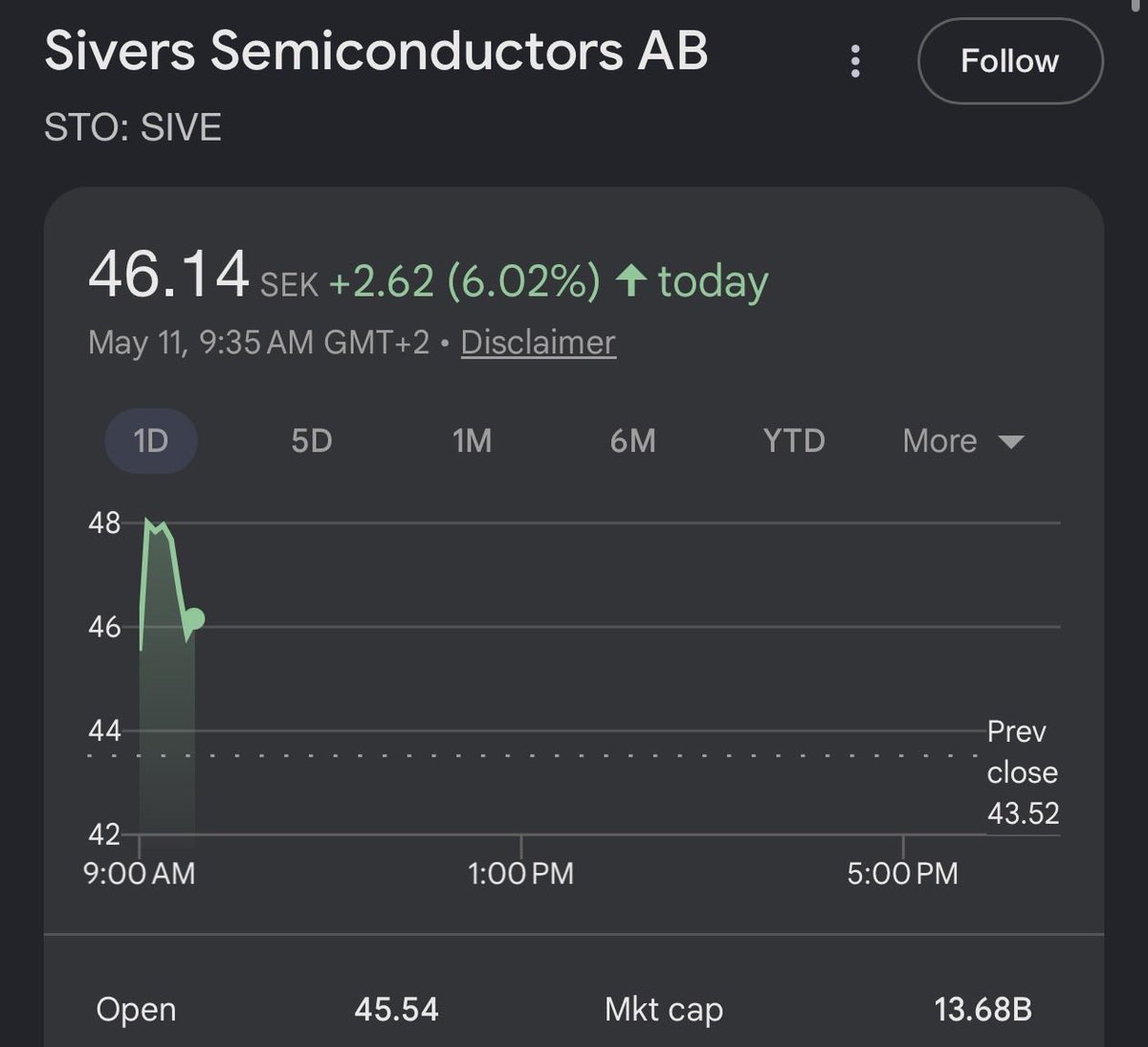

@aleabitoreddit Now it’s also being listed to the MSCI Small Cap Index. Swedish article: di.se/live/kursraket…

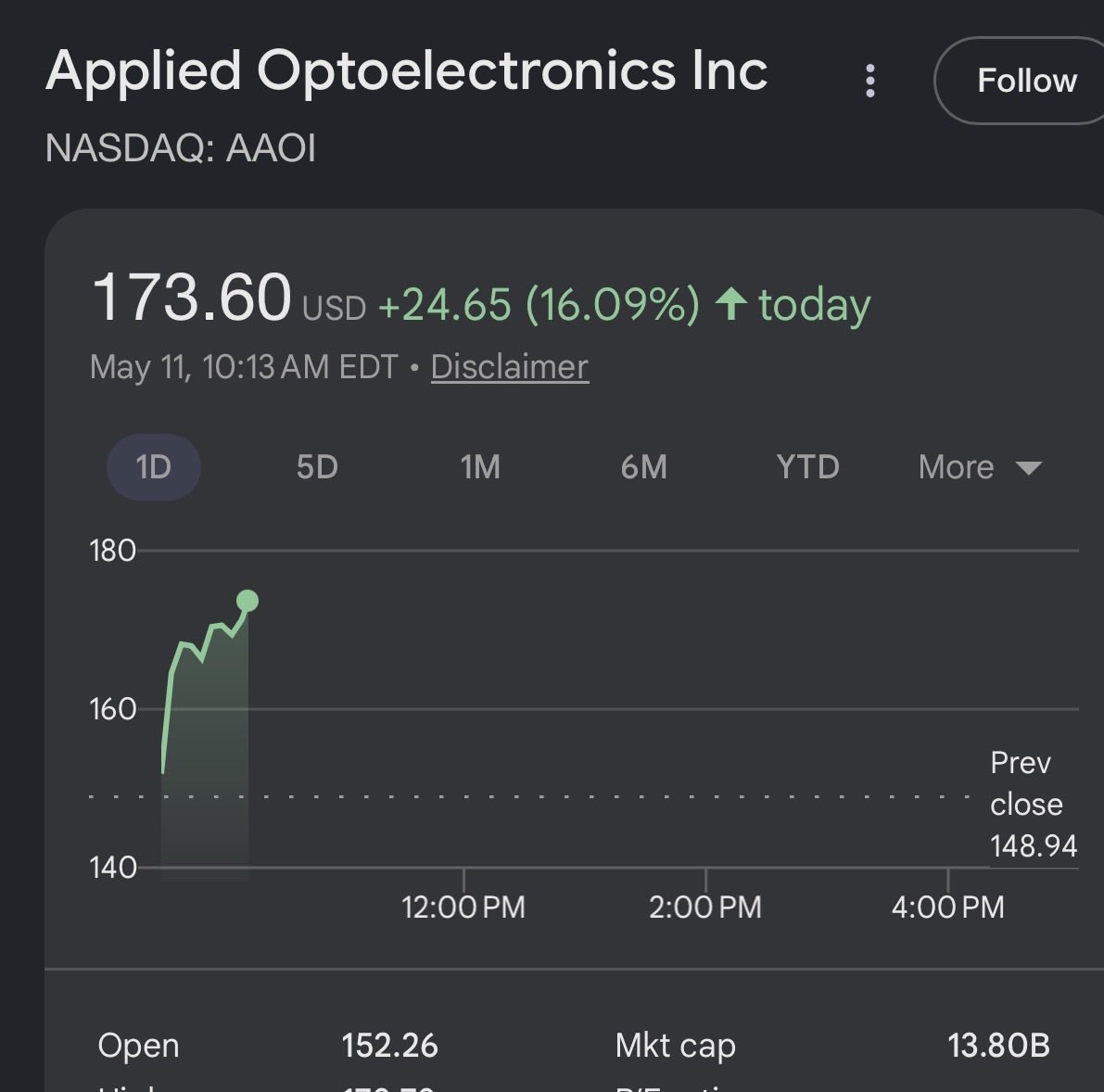

$AAOI reported earnings, it's actually extremely positive so far contrary to market reactions. Like all 2027 hyperbolic forward growth companies: Nobody should care about current financials. Key things market missed was: AOI: hit They hit 100K units/month capacity for 800G transceivers. And: -> "Significant larger growth expected starting in Q3 as capacity comes online" If you do look at financials: It's ~29.2% non GAAP gross margin on ~$151.1M revenue, guiding $180-$198m Q2. We already know from Lumentum earnings that it's more of capacity bottleneck, not a demand one. And anything they make they sell out. It's a forward growth story, so important thing aside from these notes is the earnings call on hyperscaler demand implications and capacity ramp.

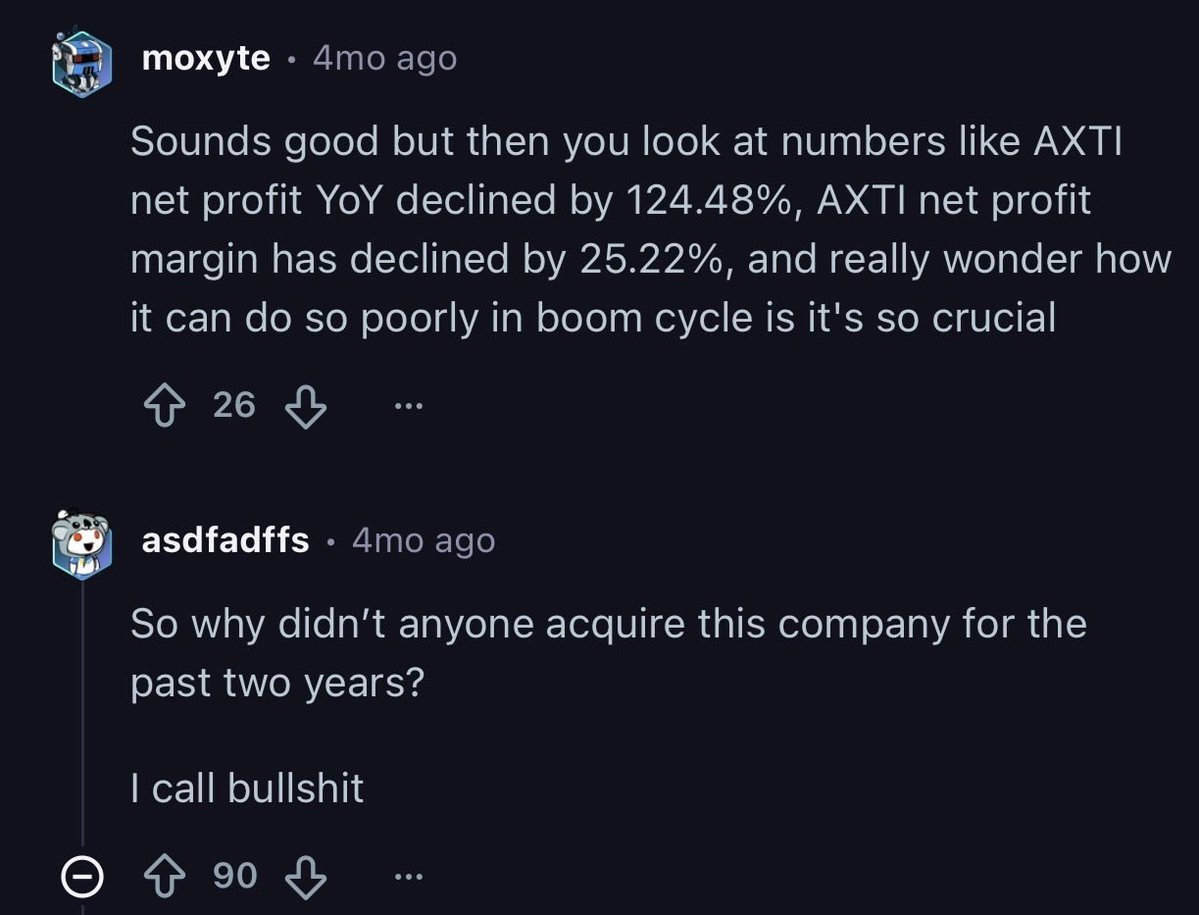

Not exactly! I'm just a tad more familiar with photonic supply chains than I am with energy so I like picking potential winners. Just wanted to introduce $IQE into the equation like i did with $AXTI, so I could do a "Did you Listen Anon?" post 3 months later if it turns out well.

I guess, post earnings when $ARM touched $268... $ARM is now #18 on the individual stock list that I went long on that hit 100%-1000%+ YTD? I've lost count TBH. Some others like $LPK and $SIMO and $HPS.A are getting really close now. But feels like I'm one of the few ones out there on X with actual receipts of all the returns + original thesis post.

$MU Bargain of the Century PE Ratio: 15.5 Sales Ratio: 2.33 50% Increase in HBM (AI Memory) Sequentially. DRAM/NAND prices are surging.